DenisTangneyJr/E+ through Getty Photographs

Introduction

On Might 28, I wrote an article entitled “My Favorites! 3 Very Enticing Shares for the Pure Gasoline Powered AI Increase.”

On this article, I’ve targeted on what I imagine can be a really lengthy one the sturdy optimization of pure fuel costs attributable to the massive improve in power demand as a consequence of new functions of synthetic intelligence.

The report added that an extra 8.5 billion cubic toes of pure fuel per day may very well be wanted to satisfy the expansion in demand.

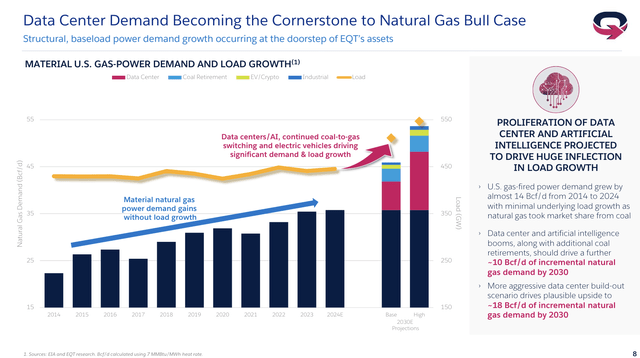

[…] Within the analysis report present knowledge middle energy demand at 11 gigawatts (GW)which within the base case is Capability is anticipated to develop to 42 GW by 2030.

The report provides that within the base case, approx By 2030, 2.7 billion cubic toes of fuel per day can be wanted. – Reuters (emphasis added)

In response to EQT Company (EQT), one of many world’s largest producers of pure fuel, we might see demand improve by 10 billion cubic toes per day by 2030 because of AI alone!

Much more optimistic estimates present a gradual improve of 18 Bcf/d.

EQT Corp.

Once more, that is simply from AI!

This excludes:

- World inhabitants development.

- The expansion of the center class in rising markets.

- The transition from coal to pure fuel continues.

On the whole, export demand may be very optimistic.

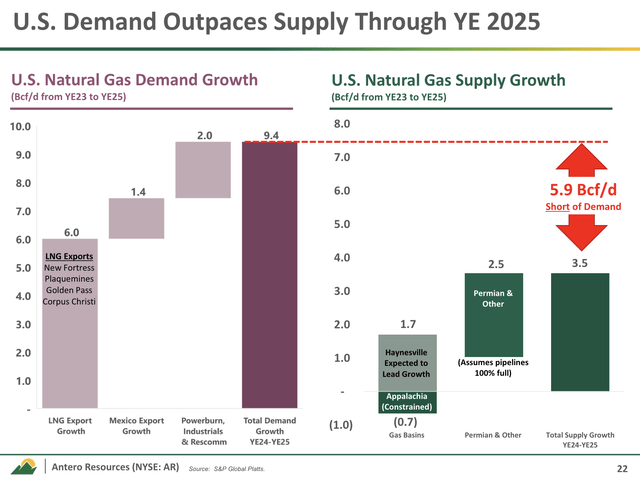

Earlier assets (NYSE: AR)star of this text, estimates that LNG (liquefied pure fuel) export development will add 6 billion cubic toes per day of recent demand by 2025. Add in stronger home demand and elevated exports to Mexico, and the corporate estimates there can be a provide shortfall of about 6 Bcf/d.

Earlier assets

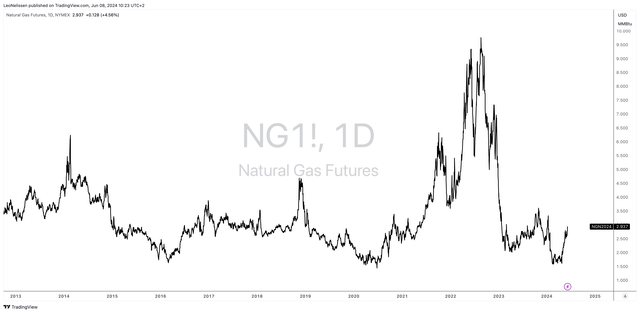

That is very optimistic and one of many the reason why pure fuel costs have began to get better.

Though costs have solely simply returned to regular, the momentum we’re seeing is actually exceptional.

TradingView (NYMEX Henry Hub)

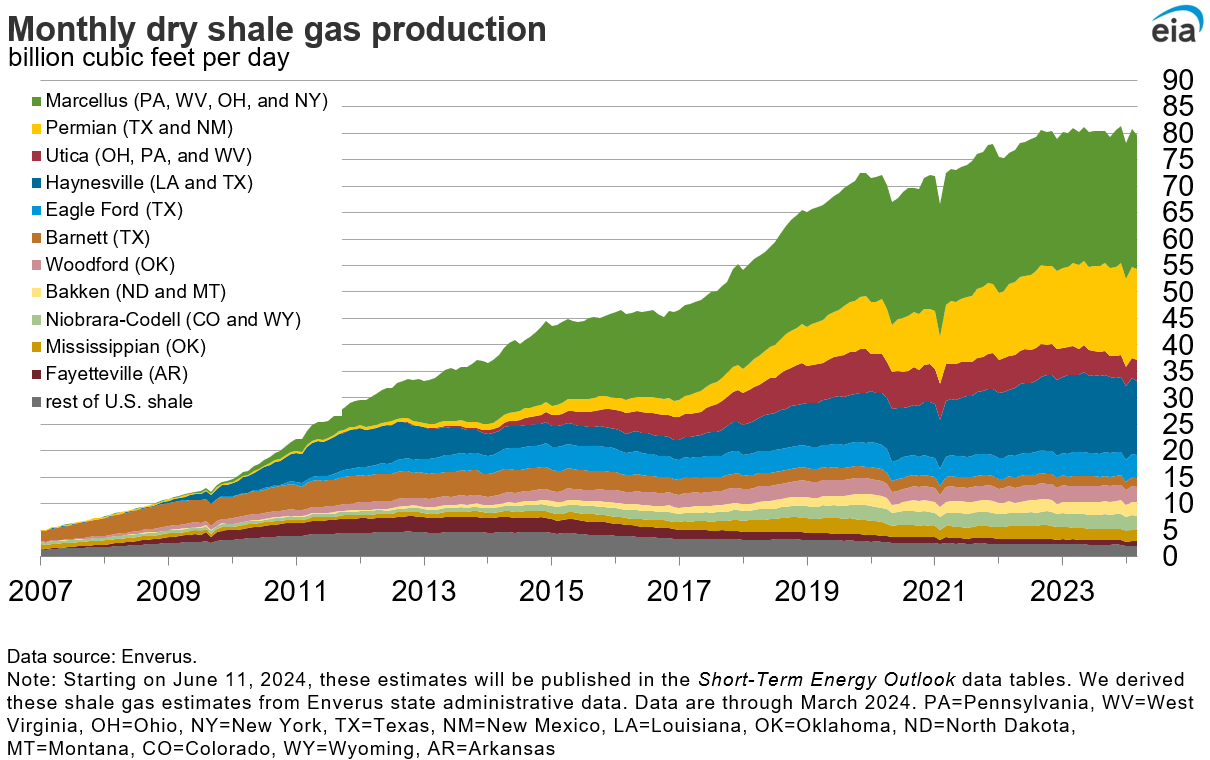

That being stated, provide as an entire has modified because the shale revolution has supplied the US with unprecedented development in pure fuel manufacturing.

Now it is over.

Though pure fuel continues to be very considerable (particularly in comparison with oil), manufacturing development has slowed dramatically.

Vitality Info Administration

In gentle of those adjustments, Goehring & Rozencwajg argue that we’ll quickly see vital adjustments in stock, permitting North American costs to converge with a lot larger worldwide costs.

The US is about to transition from a chronic interval of acute oversupply to a structural deficit of historic proportions. Whereas shares stay excessive, our fashions predict they’ll attain harmful ranges a lot before anybody thinks attainable. Given this backdrop, it isn’t clear to us that US pure fuel must be buying and selling at a report low cost to its energy-equivalent value, even after two gentle winters in a row. Traders ought to take notice.

In essence, the tip of the shale revolution is the satisfaction of the quickest rising demand for pure fuel in historical past.

Returning to Goehring & Rozencwajg:

Though we have been very early, we imagine that North American pure fuel with much less liquefaction and transportation will converge to the worldwide value, which is at present $10 per thousand toes. Traders are very bearish after two gentle winters in a row, however are neglecting the bullish provide and demand shifts at present happening. That is essentially the most uneven funding we will consider.

That is the place Antero Sources is available in.

Why I am so bullish on Antero Sources

I’ve been bullish on Antero Sources since I began protection in 2023.

My final article was written on February 19, after I left with Fr Robust purchase score.

The inventory has soared 43% since then, eclipsing the S&P 500’s 7% return.

I imagine that is only the start, as AR brings a number of qualities that make it a really perfect inventory to capitalize on pure fuel.

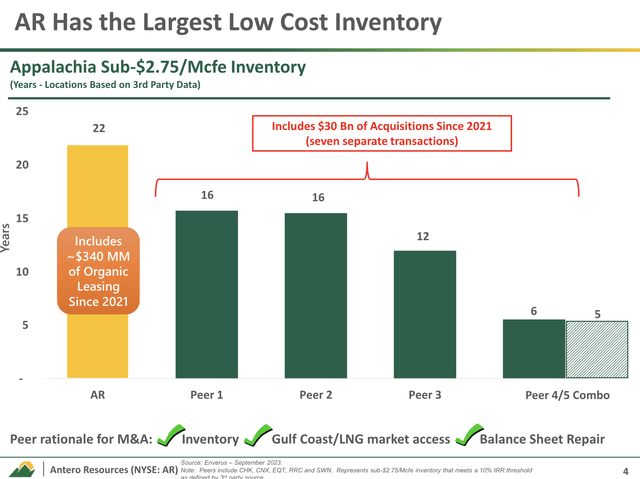

For starters, the corporate has greater than 20 years of premium inventory within the Marcello Basin (Appalachia), the place it has turn out to be probably the most environment friendly producers.

Extra exactly, excluding new developments, the corporate’s 22-year breakeven reserves are beneath $2.75/Mcfe ($2.85 MMBtu – Henry Hub unit).

Earlier assets

The corporate is very environment friendly in its pool.

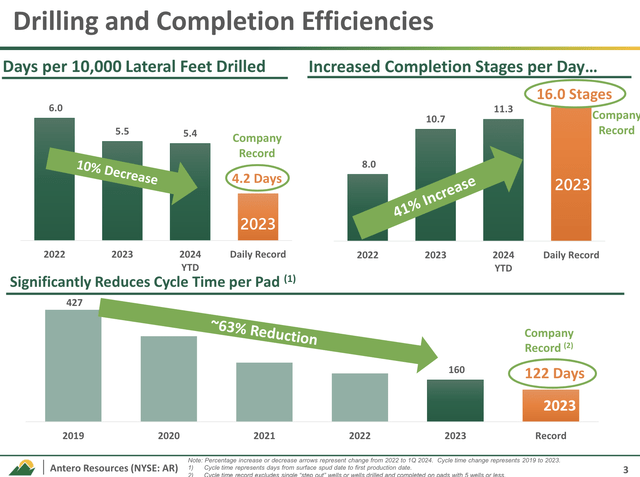

For instance, within the first quarter of this 12 months, the corporate decreased the time it took to drill 10,000 lateral toes to five.4 days. That is down from 5.5 days in 2023.

As well as, Antero set a report for the variety of levels accomplished, averaging 11.3 levels per day. This compares to only underneath 11 levels per day final 12 months.

Earlier assets

The corporate has additionally developed new completion expertise to save lots of greater than an hour of pumping time every day, and it’s benefiting from Antero Midstream’s superior water infrastructure (AM) to cut back congestion.

This infrastructure additionally eliminates the necessity for water vans.

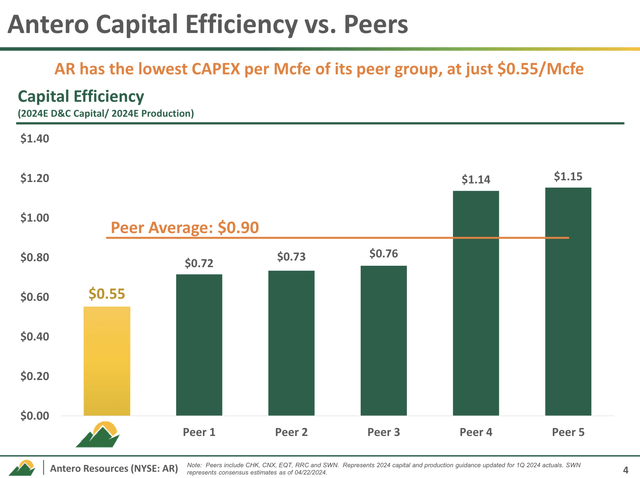

General, the corporate leads friends in capital effectivity because it solely requires $0.55 per Mcfe to take care of manufacturing. The common price amongst friends is nearly twice as excessive!

Earlier assets

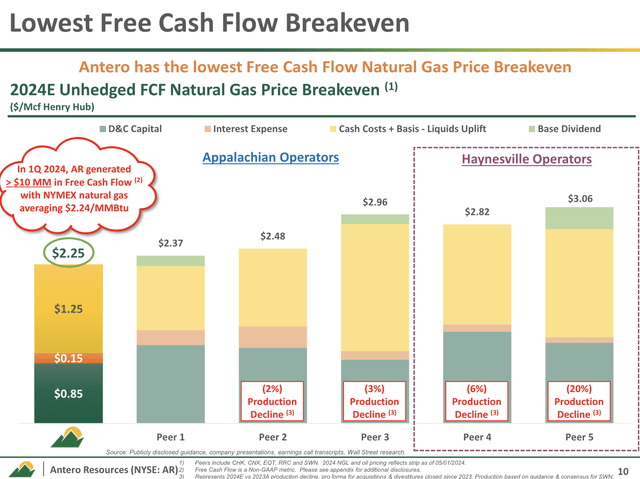

On an unhedged foundation, the corporate’s break-even is $2.24 per thousand toes, which beats main friends — particularly these in higher-cost basins just like the Haynesville.

Earlier assets

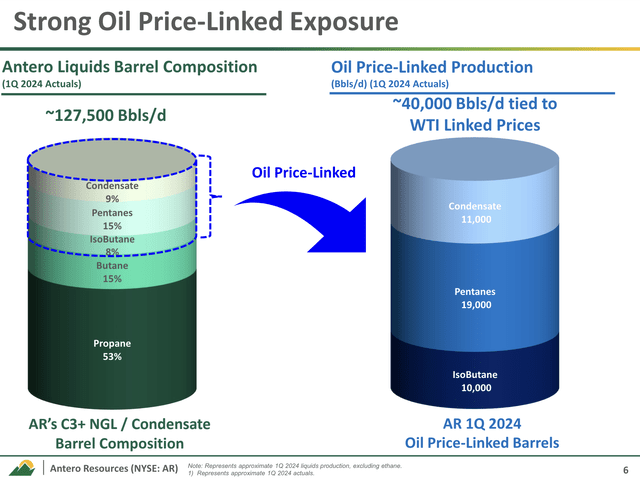

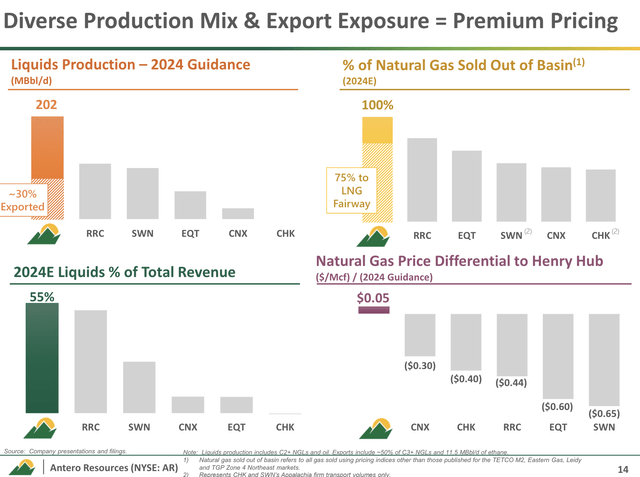

As well as, AR has one other massive benefit: product vary.

Whereas AR is a producer of pure fuel, not all of its manufacturing is low-cost pure fuel.

The corporate has a big footprint within the liquids and LPG (pure fuel) markets.

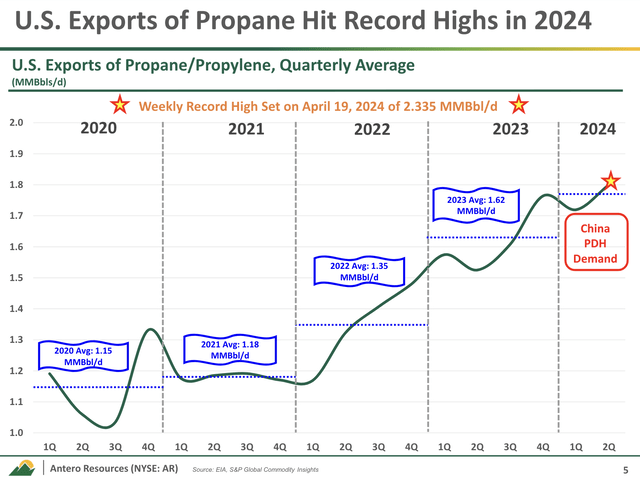

U.S. propane exports rose to an all-time excessive of greater than 2.3 million barrels per day within the first quarter. That is 14% greater than the 2023 common.

Earlier assets

This development in exports, mixed with strategic pricing selections, has enabled Antero to command premium costs for its merchandise.

For instance, propane costs as a share of WTI averaged 44% in early 2024. This was up from 36% within the fourth quarter of 2023.

As well as, Antero’s resolution to promote a better proportion of its water barrels on worldwide indices as an alternative of long-term home offers permits it to profit from higher worldwide pricing.

Earlier assets

My level is that AR is just not a pure fuel producer that’s principally depending on Henry Hub costs in its personal basin.

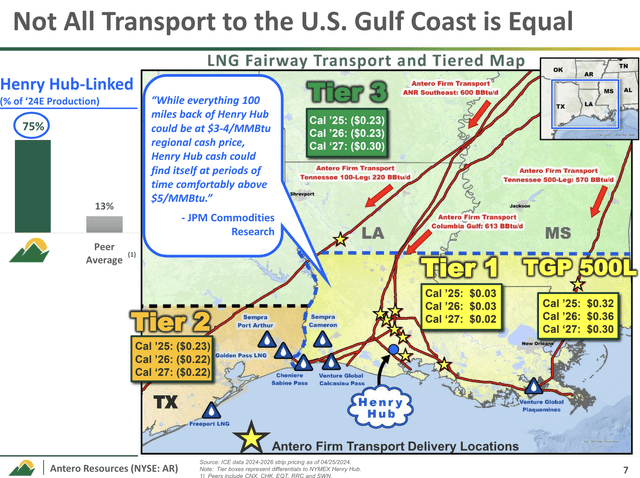

Even higher, the corporate is a serious LNG participant, because it sells roughly 75% of its pure fuel from its basin — principally to the LNG hall alongside the Gulf Coast.

As you’ll be able to think about, this places the corporate in an amazing place to entry larger costs and profit from the speedy development in international demand for LNG.

Utilizing the corporate’s personal knowledge, its friends solely promote 13% of the LNG hall.

Earlier assets

As well as, there are three different most important benefits.

- Greater than half of the corporate’s merchandise are liquids.

- It’s the solely main U.S. pure fuel producer anticipated to promote its fuel at a value larger than Henry Hub.

- It sells 100% pure fuel from its basin.

Earlier assets

I imagine these qualities set the corporate aside as probably the greatest pure fuel shares available on the market.

Advantages to shareholders

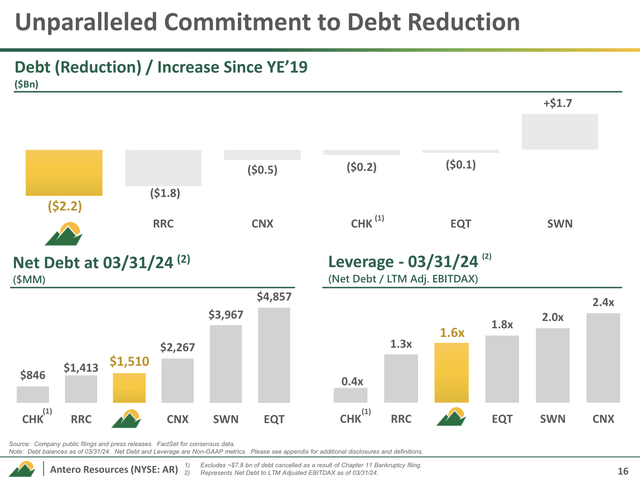

Along with a superb enterprise mannequin, the corporate has spent the previous couple of years aggressively decreasing debt.

It at present has $1.5 billion in internet debt. That is lower than half of the 2020 debt load. It additionally has no debt maturing till 2026 and a leverage ratio of lower than 2x EBITDA.

Earlier assets

Going ahead, the corporate’s technique contains decreasing gross debt and allocating future free money move to buyback shares to additional improve shareholder worth.

It doesn’t pay dividends.

Whereas augmented actuality is probably not nice for income-oriented buyers, it has enormous free money move potential.

This 12 months and primarily based on the present market surroundings, analysts anticipate the corporate to generate $290 million in free money move. That is a giant quantity contemplating how low pure fuel costs are.

That represents 3% of its $10.6 billion market cap.

That quantity is anticipated to develop to $1.1 billion subsequent 12 months, or greater than 10% of the market capitalization.

If pure fuel costs rise to >$5 Henry Hub over time, the corporate has the chance to repurchase shares at an unprecedented price, considerably growing the corporate’s worth per share.

Given Henry Hub’s $3 free money move alternative, I imagine we might anticipate a free money move return of 12-16% in a steadily elevated pure fuel value vary of $4-5 – relying on development plans .

This additionally implies that I anticipate AR to outperform the power benchmark ETF (XLE) as I imagine the upward development in pure fuel is very undervalued.

So I comply with a Robust purchase score as a result of I anticipate the market to find the enchantment of AR and analogues – particularly as soon as international financial development improves.

Personally, I’ve held AR shares since final 12 months – with good returns. Nevertheless, I offered as a result of I closed my total buying and selling portfolio. I made a decision to maneuver my cash into my long-term funding portfolio – for quite a lot of causes.

Now I am taking a look at how greatest to include non-dividend shares into this technique.

Evidently, given how a lot I like AR, I’ll make it a “everlasting” spot in my long-term portfolio within the coming weeks and months.

So please do not be confused that I’m not disclosing a protracted place in AR right now.

I invested in Antero Midstream, not Antero Sources.

Take it away

The way forward for pure fuel appears extremely promising, pushed by rising AI-related demand and broader market tendencies equivalent to LNG exports and the continuing transition from pure fuel to coal.

Right here, Antero Sources stands out as your best option as a consequence of its spectacular efficiency, strategic positioning and robust monetary place.

With deep reserves within the Marcellus Basin, low manufacturing prices and vital publicity to engaging LNG markets, AR can capitalize on rising international demand for pure fuel.

Furthermore, the corporate’s concentrate on decreasing debt and the potential for vital free money move sooner or later enhance its funding enchantment.

Execs and cons

Execs:

- Robust inventory and effectivity: AR has greater than 20 years of premium stock within the Marcellus Basin and leads friends in capital effectivity.

- Strategic positioning: By promoting 100% of its pure fuel from its pool, AR improves its pricing.

- A various set of merchandise: Vital publicity to high-margin liquids and LNG additionally improves pricing.

- Monetary well being: Aggressive deleveraging and robust free money move potential present subdued monetary threat.

- The rise of Tailwinds: Unprecedented demand development pushed by AI, coal-to-gas transition and speedy development in LNG exports.

Cons:

- No dividends: AR doesn’t provide revenue via dividends.

- Market volatility: Pure fuel costs might be risky, making AR far more risky than the “common” shares you could have invested in.

- Business dangers: Regulatory adjustments and environmental points might have an effect on its operations and finish markets.