anilbolukbas

VF Company (NYSE: VFC) sells branded clothes, footwear and equipment below a portfolio of manufacturers. Manufacturers embrace massive world names comparable to North Face, Vans, Timberland and Dickies, in addition to smaller manufacturers together with Icebreaker, Napapijri, JanSport and Supreme, which was acquired. in 2020 for $2.1 billion.

The inventory has misplaced most of its worth since 2021 resulting from VFC’s poor model administration and costly M&A method, which has led to heavy debt and underperforming manufacturers. An intensive reform plan is within the works, however no results have been seen in This fall as revenues fell by -13.4%.

Ten-year inventory chart (In Search of Alpha)

The sluggish efficiency of the VFC model has but to see an finish

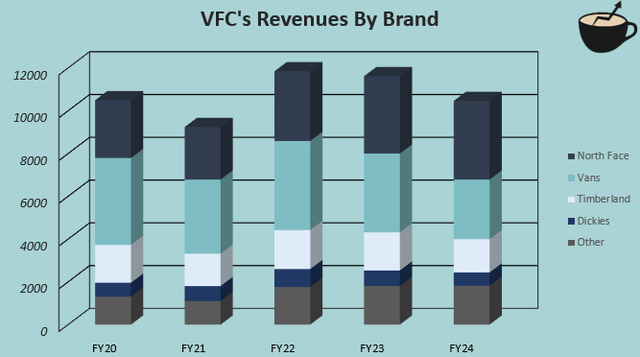

VFC has a latest historical past of progress in lots of the firm’s key manufacturers. Income for Vans, VFC’s largest model by fiscal 2024, is down from $4,063.4 million in fiscal 2020to the large issues with the Covid pandemic to only $2,785.7 million in fiscal 12 months 2024 at a CAGR of -9.0%. Timberland, VFC’s third largest model, had a -3.1% CAGR over the identical interval, whereas Dickies -1.1% CAGR – the corporate appears unable to adapt to altering buyer demand with many manufacturers stagnating.

The acquisition of Supreme in 2020 additionally exemplifies VFC’s historical past of poorly managed manufacturers. The model boosted VFC’s gross sales by $500 million in fiscal 2022, with formidable plans to extend progress to $1 billion by new shops, model collaborations and world enlargement by VFC’s in depth world distribution community. As Google Traits exhibits steady world search time period quantity for Supreme, the corporate recorded goodwill and intangible asset impairment prices totaling $735 million in fiscal 2023, with an extra $313.1 million in fiscal 2024 resulting from weak model metrics. VFC is now reportedly contemplating promoting the enterprise.

Creator’s calculation utilizing VFC 10-Ok knowledge

The North Face model is outstanding for VFC because the model’s stagnant picture from FY14 to FY17 has was a powerful CAGR of 8.0% from FY2020 to FY2024, with the corporate rising as VFC’s largest model. Quick progress from the top-performing model has additionally begun to stagnate, with -5.3% YoY income in This fall and 1.7% progress for the total 2024 fiscal 12 months. Whole income progress in This fall was -13.4%, marking one of many deepest declines in VFC’s income in latest historical past.

The poor gross sales efficiency finally led to a margin squeeze, because the working margin was simply 6.0% in fiscal 2024, following a long-term double-digit degree with a median of 11.4% from fiscal 2016 to 2020. Additional declines additionally pose the same menace as SG&A scales with inflation and failed progress initiatives towards declining gross margins.

Do not take the success of the reversion plan at face worth

To fight the poor efficiency, VFC unveiled a resuscitation plan in its Q2/FY2024 report press launch. The plan was unveiled by Bracken Durrell, VFC’s new CEO, who was appointed months earlier than the plan was introduced.

Within the plan, VFC goals to enhance ends in North America by altering its working mannequin, reshaping the Vans model with the appointment of a brand new model president, slicing $300 million in fastened prices and decreasing debt – the modifications mirror a key shift in VFC’s technique and a transparent concentrate on turnaround Vans.

A $300 million discount in fastened prices seems to be a superb driver of profitability if it may be efficiently applied with out compromising organizational efficiency. Nevertheless, the corporate wants a rebrand to keep up earnings as profitability continues to endure from declining gross sales, because of VFC’s almost $6 billion in interest-bearing debt.

I do not assume the Reinvent plan’s turnaround targets must be taken at face worth earlier than the manufacturers’ efficiency is best demonstrated – the turnaround plan for Vans was already unveiled at Vans’ 2022 Investor Day, because it was beforehand for North Face. Nevertheless, the Vans model has but to expertise any stabilization after a number of quarters. Introduced progress targets for Timberland and Dickies have been additionally missed, with income persistently declining.

The plan is now extra thorough than the one offered at Investor Day in 2022, particularly since Bracken Darrell has been appointed as the brand new CEO to drive change on the firm. Bracken Durrell has a powerful resume, having beforehand served as CEO of Logitech Worldwide ( LOGI ) and held government positions at Procter & Gamble ( PG ), Whirlpool ( WHR ), and Basic Electrical ( GE ). Nevertheless, main style manufacturers might be tough, as sustaining and creating demand requires deep, ongoing data of consumers and developments – whereas the brand new CEO is being praised for reworking the Previous Spice model, the same turnaround at Vans may very well be tougher and sure , requires a special kind of branding technique.

Efficiency exhibits no indicators of enchancment but. Vans gross sales fell -26.3% in This fall, North Face -5.3%, Timberland -13.7% and Dickies -15.2%. The remainder of the manufacturers have been nearly steady with a slight lower. The search time period Vans continues to point out weak point in Google Traits.

Most just lately, in February, VFC introduced that the corporate is present process a strategic portfolio evaluate and is now seeking to doubtlessly promote lots of its smaller manufacturers. The evaluate might create upside, however no gross sales have been introduced but.

Inventory valuation costs in too many enhancements

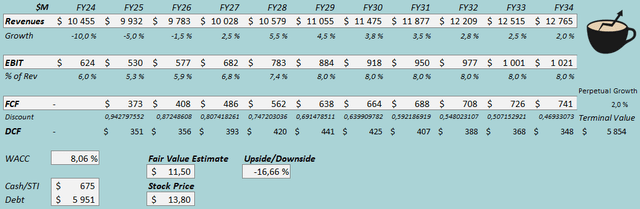

I constructed a reduced money stream [DCF] a mannequin for estimating the approximate truthful worth of shares. Within the mannequin, I think about a semi-successful reversal, leaving margins larger than they’re now, however not fairly at long-term ranges.

On the earnings facet, I estimate a -5% decline in FY2025, a -1.5% decline in FY2026, however a return to higher efficiency from FY2027. From FY2026 to FY2034, I estimate a income CAGR of three.4%, after which progress ends at 2%.

As VFC plans to save lots of $300 million in prices and I estimate higher earnings in a couple of years, I anticipate the EBIT margin to extend from 5.3% in FY2025 to a remaining 8.0%. The corporate has pretty low capex and dealing capital wants, making the money stream conversion fairly good.

The DCF mannequin (Creator’s calculation)

VFC is estimated to have a good worth estimate of $11.50, which is 17% under the inventory worth on the time of writing – even when Reinvent’s restoration plan exhibits a big variety of enhancements, the inventory seems to be reasonably overvalued. Good progress appears to require an nearly full rebrand, which I do not assume buyers ought to anticipate.

The DCF mannequin makes use of a weighted common value of capital of 8.06%. The WACC used is derived from the capital asset pricing mannequin:

SARM (Creator’s calculation)

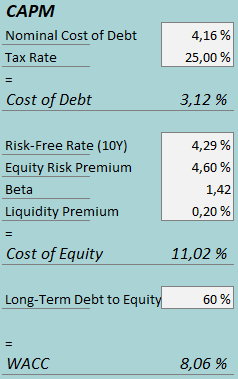

In This fall, VFC spent $61.8 million on curiosity, making the corporate’s rate of interest 4.16% on present interest-bearing debt. I estimate a long-term debt-to-equity ratio of 60% resulting from the truth that VFC’s steadiness sheet continues to leverage debt however plans to deleverage. I consider that debt refinancing now’s more likely to lead to the next rate of interest, creating average danger to the price of capital.

To estimate the price of fairness capital, I exploit the 10-year United States Treasury yield of 4.29% because the risk-free fee. The fairness danger premium of 4.60% is Professor Aswath Damodaran’s newest estimate for the USA, up to date 5thousand January. Searching for Alpha places VFC’s beta at 1.42. Lastly, I add a liquidity premium of 0.2%, creating a price of fairness of 11.02% and a WACC of 8.06%.

Considerable upside danger

The bearish thesis nonetheless has quite a lot of upside danger — if Vans’ turnaround proves to be very profitable, a return to long-term margins and higher progress may make the inventory undervalued on the present worth. With a median FY2016-2020 working margin of 11.4% from FY2027, the DCF mannequin would estimate a progress potential of 65%. Nevertheless, there are not any indicators of such a turnaround but, and such a state of affairs shouldn’t be thought of doubtless but.

As well as, the strategic different evaluate may nonetheless be within the upside if VFC can promote well-known manufacturers at a great worth – Timberland, Dickies and Supreme manufacturers may get VFC a great valuation if a possible purchaser is extra assured within the manufacturers’ management. . Hypothesis surrounding potential gross sales is rising, and a sale of a number of of VFC’s manufacturers is more likely to occur sooner or later in my view. Nevertheless, estimating potential gross sales might be irritating; gross sales are usually not a sure strategy to generate revenue.

I encourage buyers to maintain a detailed eye on the model’s efficiency within the coming quarters, as an entire turnaround may nonetheless be very helpful for shareholders.

Take it away

VFC’s new CEO has launched a serious reform plan to repair underperforming manufacturers. Dramatic cost-cutting is deliberate, and Vans is slated to ship higher efficiency by management modifications and operational modifications. Nevertheless, buyers should not purchase into an nearly full turnaround simply but – a Vans turnaround has been tried for a while, and Bracken Darrell does not have a lot expertise with high style manufacturers, which may nonetheless show to be an issue. This fall efficiency additionally continues to point out weak point throughout manufacturers, with even North Face now displaying weak point after a earlier turnaround. The rating appears to take good enhancements as a base state of affairs, which I doubt for now. Whereas promoting the model or altering the company may very well be a giant plus, the chance/reward ratio doesn’t appear good and I provoke VF Company with a Promote.