simonkr/E+ by way of Getty Photographs

Stratasys’ (NASDAQ: SSYS) monetary efficiency in latest quarters has been cheap given the difficult demand setting. Nevertheless, traders proceed to keep away from the inventory, and the share value has fallen greater than 30% for the reason that begin of the 12 months.

I beforehand assumed that Stratasys was persevering with losses will put downward stress on the inventory value. This continues to be the case because the gentle demand setting makes it tough for the corporate to generate enough revenues to interrupt even. Regardless of this, Stratasys nonetheless has a fairly wholesome stability sheet and has managed to considerably cut back its money burn in latest quarters, positioning the corporate towards the present downturn.

Stratasys additionally nonetheless has a takeover provide, which ought to seemingly present extra leverage to the inventory value. Nano Dimension (NNDM) has provided to amass all excellent shares of Stratasys 2023 for US$16.5 per share in money. Whereas Stratasys has been fairly antagonistic to Nano Dimension’s advances previously, the proposal nonetheless exists and the businesses seem like in discussions.

Market circumstances

Buyer capital spending stays constrained on account of the tight monetary setting, an ongoing problem for Stratasys’ capital gross sales. Difficult circumstances are anticipated to persist by way of 2024, resulting in ongoing buy delays and longer gross sales cycles. Exterior of the buyback, Stratasys’ income has remained pretty flat, and the corporate believes it is gaining market share. Stratasys’ first-quarter gross sales cycle reportedly improved barely, and the corporate’s buyer engagement was additionally good.

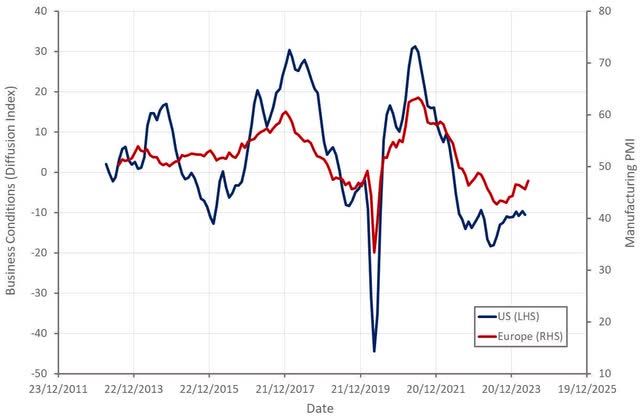

Determine 1: Manufacturing survey information (supply: created by the writer utilizing Federal Reserve information)

Stratasys is not the one complement firm going through losses and declining income, suggesting that its present struggles are primarily the results of macro discuss moderately than any particular firm problem.

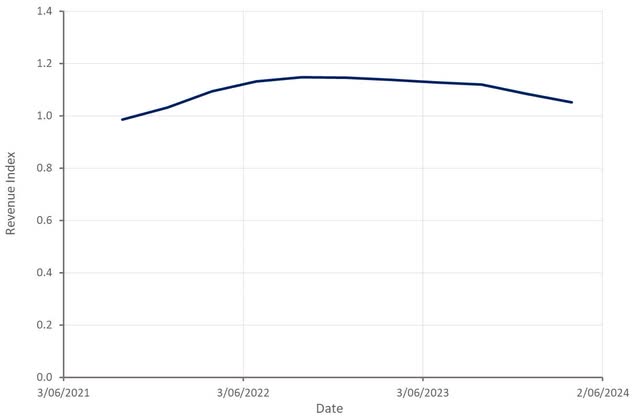

Determine 2: Revenue index of listed manufacturing firms (supply: created by writer utilizing information from firm experiences)

Stratasys Enterprise Updates

Stratasys continues to increase its materials and printer choices with a concentrate on mass manufacturing use circumstances. The F3300 was launched in late 2023 and offers twice the throughput of ordinary FDM methods at considerably decrease manufacturing prices. It targets the high-end FDM market. The F3300 is reportedly serving to to increase Stratasys’ gross sales funnel, with preliminary orders exceeding the corporate’s expectations. Nevertheless, a extra important revenue of three,300 F3 is anticipated solely within the second half of the 12 months. Early clients embody Toyota, BAE Programs, Sikorsky and Nissan.

Stratasys additionally lately launched the H350 model 1.5, which has improved sensors and distant service capabilities. Together with this, Stratasys launched SAF HighDef printing capabilities, permitting clients to create extra complicated components. This will probably be delivered as a part of a firmware replace and will probably be backwards suitable with earlier H350 fashions.

Stratasys additionally launched new supplies for FDM that may open up functions in fields corresponding to aerospace and medical. VICTREX AM 200 is a PEEK-based polymer that’s immune to temperatures, corrosion and chemical compounds and has robust mechanical properties.

Stratasys additionally launched GrabCAD’s Elements on Demand, which integrates the corporate’s software program platform with Stratasys Direct, permitting clients to entry Stratasys Direct 3D printers. Stratasys is making an attempt to create a related software program ecosystem and believes that integrating {hardware} and software program provides it a bonus as a result of it has entry to logs that present perception into buyer wants. Success on this space will go a good distance in creating differentiation and enhancing Stratasys’ potential to generate worthwhile development.

Monetary evaluation

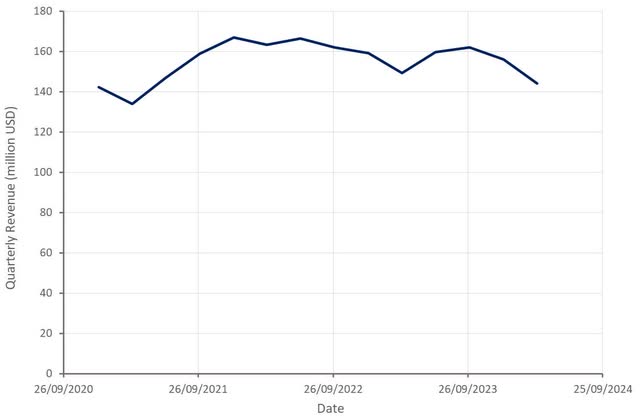

Stratasys’ first-quarter income was $144 million, down 3.5% 12 months over 12 months. Excluding the sale of non-core firms, revenues remained comparatively flat. Product income was $99 million within the first quarter, down roughly 2% year-over-year. Given the heavy use of beforehand acquired methods, Stratasys expects that these methods will ultimately get replaced by increased performing methods, leading to a restoration in product revenues. Inside product income, system income decreased roughly 19% YoY, whereas consumables income elevated roughly 10%. It must be famous that Covestro was acquired in April 2023 and contributes US$ 4-5 million per quarter. With out that, revenue from consumables was fairly flat. Providers income was $45 million within the first quarter, down about 7% year-over-year. Excluding gross sales, revenues from providers grew by 1.8%.

Stratasys expects $630 million to $645 million in income in 2024, with constant quarterly income development and stronger development within the second half of the 12 months. This could imply a rise of about 1.6% within the center. Given Stratasys’ weak Q1 outcomes and continued macro weak point, I am skeptical that this will probably be achieved.

Determine 3: Stratasys Income (supply: created by writer utilizing Stratasys information)

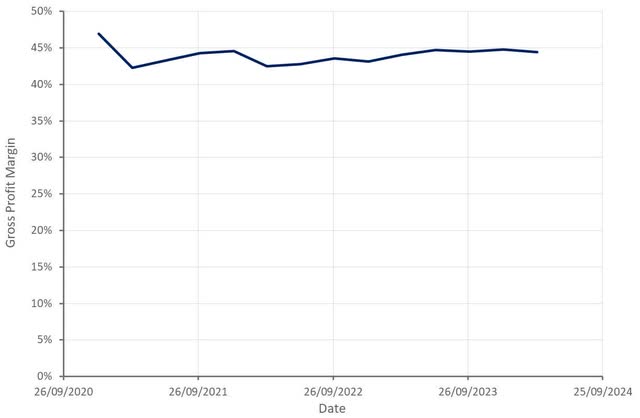

Stratasys’ gross margin has been pretty regular in latest quarters, supported by increased consumables income and better Stratasys Direct profitability. Inflationary pressures related to the pandemic are additionally now not a problem.

Determine 4: Stratasys Gross Revenue Margin (supply: created by writer utilizing Stratasys information)

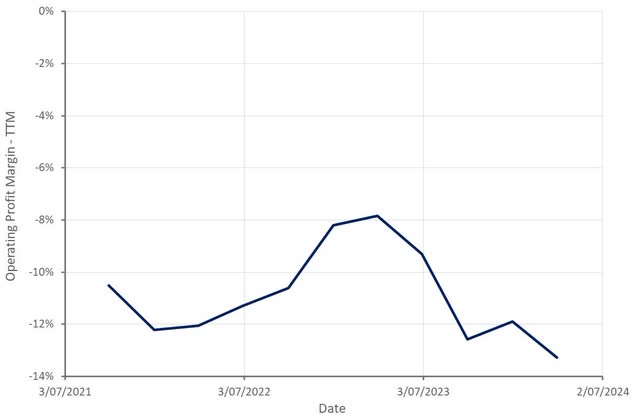

Stratasys’ working bills had been $88.4 million within the first quarter, a rise of roughly 7% year-over-year. The rise was because of latest acquisitions and bills associated to the corporate’s strategic evaluation course of. In consequence, the corporate’s profitability continues to say no. Whereas that is clearly a destructive, Stratasys’ losses are beneath management and its money circulate is enhancing. Stratasys generated $7 million from operations and posted constructive money circulate within the first quarter. The corporate expects constructive money circulate for the complete 12 months.

Determine 5: Stratasys Working Revenue Margin (supply: created by writer utilizing Stratasys information)

Conclusion

Stratasys’ declining income and ongoing losses proceed to place stress on the inventory. Whereas destructive, that is largely the results of a gentle demand setting. Exterior of the buyback, Stratasys’ earnings are nonetheless fairly stable, and the corporate is lowering its money burn. Stratasys additionally nonetheless has about $160 million in money and money equivalents on its stability sheet, which offers flexibility.

I am not very bullish on the outlook for many additive firms, however the market might be too pessimistic at this level. The present downturn ought to set off consolidation and pressure sellers to grow to be extra environment friendly, resulting in increased profitability when demand recovers.

As well as, there’s an acquisition provide as a backup ought to Stratasys’ enterprise proceed to wrestle. Stratasys has offered little info on the progress of its strategic evaluation, besides to say that it’s fascinating and making progress. Nevertheless, Nano Dimension’s provide stays on the desk and is price considerably greater than Stratasys’ present share value.

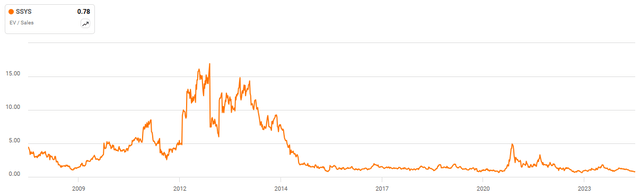

Determine 6: Stratasys EV/S ratio (supply: In search of Alpha)