demaerre/iStock through Getty Photos

Funding thesis

It looks like in a single well-known cartoon, the whole lot Nvidia ( NVDA ) touches turns to gold. Typically this notion goes too far, as in SoundHound (NASDAQ: SOUN) huge rally in 2024. Shares soared in February when Nvidia reveled in its funding in it. Really Nvidia virtually nothing was invested in SOUN in comparison with its $3 trillion market cap. I believe Nvidia makes a whole lot of those sorts of investments yearly, however the buzz round SOUN was notably robust.

There are definitely causes to be optimistic about SOUN. The corporate is delivering enormous income progress and the present momentum is actually robust. However, the corporate generates lower than $20 million in income per quarter in an business value $3.8 billion. Because of this the corporate’s footprint is sort of invisible. The business is anticipated to flourish over the following decade, however SOUN may be very skinny CAPEX prices recommend that entry limitations are extraordinarily low.

General, I believe the professionals and cons make up for one another. On this context of extraordinarily excessive uncertainty, I consider that the mass premium revealed by my valuation evaluation is unjustified. Nonetheless, I give SOUN a Robust Promote score.

Firm info

Based on its newest 10-Okay submitting, SoundHound’s mission is to make the world voice-intelligent by way of an impartial AI platform that allows folks to work together with services and products the way in which they work together with one another—by talking naturally.

SOUN provides varied AI-based options that may assist companies create voice assistants for his or her choices. The corporate’s fiscal 12 months ends on December 31, and it operates in a single enterprise phase.

Funds

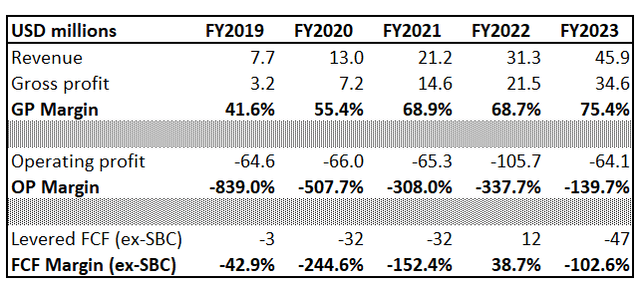

SOUN went public not too way back, which is why its P&L is just out there from FY2019. However, 5 years is a very long time horizon to attract conclusions about the principle monetary traits of an organization. The corporate has achieved a 56% income CAGR, however the scale is comparatively small, with TTM income nonetheless effectively under $100 million. The enterprise mannequin seems sturdy as gross margins present robust growth because the enterprise expands.

Writer’s calculations

Working margin can also be exhibiting a stable optimistic pattern as revenue is compounded at a robust tempo. SOUN remains to be burning money as a result of the corporate wants to take a position closely to gasoline progress. That does not seem to be a lot of an issue as a result of SOUN is in a stable monetary place with greater than $200 million in money and far much less excellent debt. I believe SOUN’s monetary place is stable and permits the corporate to proceed to reinvest in innovation.

Searching for Alpha

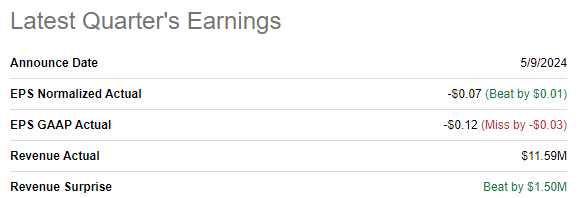

The most recent quarterly earnings had been launched on Might 9, when the corporate posted optimistic earnings and adjusted EPS. The income momentum is large as the corporate elevated profitability by 73% year-over-year. However, the numbers are fairly low with 1Q11 income of $11.6 million, and share progress could be deceptive. Additionally, on a sequential foundation, income fell from $17.2 million to $11.6 million.

Searching for Alpha

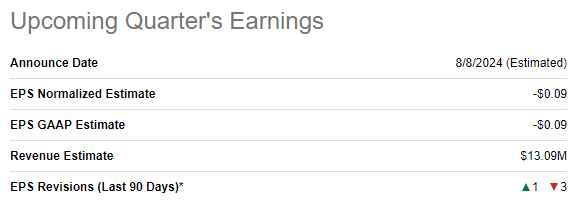

The publication of the revenue for the following quarter is scheduled for August 8. Based on consensus estimates, income for Q2 shall be $13.1 million, which might be about 50% greater than the identical quarter final 12 months. Whereas the 50% enhance in income is spectacular, the slowdown in progress can also be important. Furthermore, adjusted earnings per share are anticipated to say no from -0.07 to -0.09 {dollars}, regardless of the rise in revenues.

Searching for Alpha

To summarize, SOUN’s monetary efficiency seems to be typical for a younger and comparatively small firm. The corporate is exhibiting enormous income progress with a slightly erratic price of growth, and its backside line can also be nonetheless risky. For a rising firm, it is usually necessary to grasp the potential for future income progress.

So let me zoom out from a purely monetary perspective and take a look at different necessary facets. The bullish signal is that the business is rising and is anticipated to point out huge progress over the following decade. Based on varied sources, the business is anticipated to point out a double-digit CAGR over the following decade. For instance, Spherical Insights expects the worldwide voice assistant market to develop at a CAGR of 30.5% over the following decade. I additionally wish to level out that the identical supply estimated that the entire business in 2023 shall be $3.8 billion. If this estimate is right, it signifies that SOUN has a market share of about 1.5%.

Though the business is anticipated to be scorching for longer, I have to additionally emphasize that the competitors is prone to be fierce. SOUN’s money move assertion exhibits that the corporate spends lower than a million US {dollars} in capital expenditure per 12 months, which signifies that the limitations to entry are very low and there are lots of gifted engineers who can grow to be potential rivals for SOUN. Furthermore, it is laborious to say that SOUN is a pioneer in an business the place Apple’s ( AAPL ) Siri is already 12 years outdated and Amazon’s ( AMZN ) Alexa will have a good time its first anniversary this 12 months.

In conclusion, SOUN is exhibiting stable progress in income and working leverage. Because of this the corporate is efficiently navigating the booming business, absorbing its tailwinds. However, the dimensions of the corporate is just too small and the relative progress numbers could be deceptive. The business is anticipated to keep up a 30% CAGR over the following decade, however limitations to entry are extraordinarily low, which means it will likely be extraordinarily tough for SOUN to defend and develop its market share. Furthermore, giants comparable to Apple and Amazon have been on this discipline for a couple of decade, and there’s little proof that these firms have been in a position to earn a living from it.

Evaluation

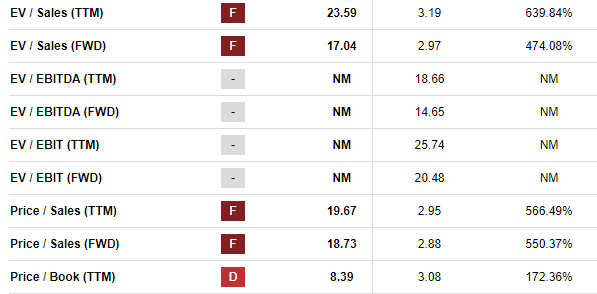

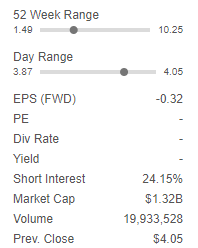

The inventory is up 6% over the previous twelve months, effectively underperforming the broader US inventory market. However, the efficiency of shares for the reason that starting of the 12 months is large – the rally was 89%. As a result of lack of profitability, most valuation ratios will not be out there. Nonetheless, those which might be unlocked look extraordinarily excessive.

Searching for Alpha

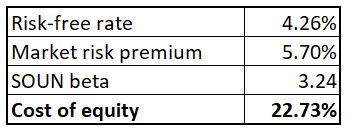

However, the ratios could be deceptive once we discuss concerning the valuation of younger, creating firms. So I ought to positively proceed with the discounted money move [DCF] modeling. I start by figuring out the low cost price that must be the price of fairness as a result of SOUN’s low stage of debt. The CAPM strategy is a method of calculating an organization’s value of fairness; all variables are available on-line.

Writer’s calculations

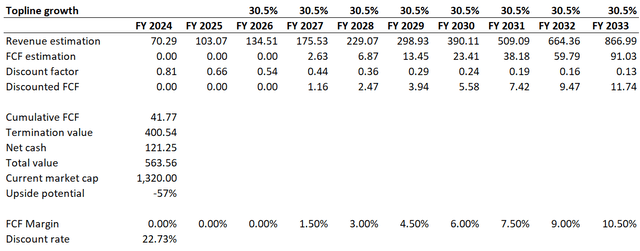

Two different necessary assumptions are far more sophisticated. Consensus income progress estimates can be found for fiscal years 2024 and 2025 solely. So by the tip of the following decade, I am hoping for an business CAGR predicted by Spherical Insights of 30.5%. As we noticed in my monetary evaluation, the corporate’s FCF margin may be very adverse. Over the following two years, consensus doesn’t count on adjusted EPS to be near zero. So I believe the earliest we will count on to see a optimistic FCF return is FY2027. With anticipated aggressive income progress, I’m bullish on FCF margin growth of 150 foundation factors yearly.

Writer’s calculations

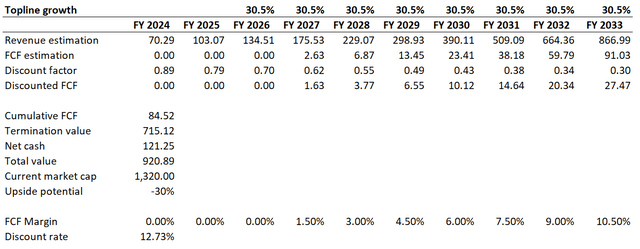

My DCF modeling exhibits that SOUN has a good worth of $564 million, roughly double its present market cap. My critics will possible argue {that a} low cost price of twenty-two.7% is just too excessive, however within the desk under we will see that even with a a lot softer low cost price, SOUN remains to be overvalued by 30%.

Writer’s calculations

Dangers to my bearish thesis

My DCF mannequin relies on assumptions. These assumptions are extremely unsure, and they’re extremely variable. Consensus earnings estimates might grow to be far more aggressive if the corporate delivers important earnings or considerably raises steering. If SOUN strikes to a optimistic FCF margin quicker than my DCF mannequin expects, that will additionally very possible have a optimistic impact on honest worth.

As I identified above, numerous the thrill across the inventory this 12 months was brought on by the information that Nvidia is an investor in SOUN. Maybe I am underestimating the synergistic impact of Nvidia’s presence amongst shareholders. Or the inventory might soar once more if new info emerges about Nvidia’s buy of further SOUN shares.

Searching for Alpha

Final however not least, there’s a enormous 24% brief curiosity in SOUN. Due to this fact, there’s the potential of a brief decline that would result in a big rally within the inventory as a result of shorts protecting their positions.

Backside line

In conclusion, SOUN is a “robust promote”. I believe all of the dangers and uncertainties outweigh the upsides, making the present premium to honest worth utterly inappropriate.