zemography

Welcome to a different installment of our weekly Choice Share Evaluate, the place we talk about exercise within the Choice Shares and Child Bonds market, each from the underside up, highlighting particular person information and developments, and from the highest down, offering an outline of the broader market. We strive too so as to add historic context in addition to related themes that seem like driving the markets or that traders ought to concentrate on. This replace covers the interval as much as the third week of Could.

Be sure you try our different weekly updates protecting the enterprise growth firm (“BDC”) markets in addition to the closed-end fund (“CEF”) markets for insights into the broader revenue house.

Market motion

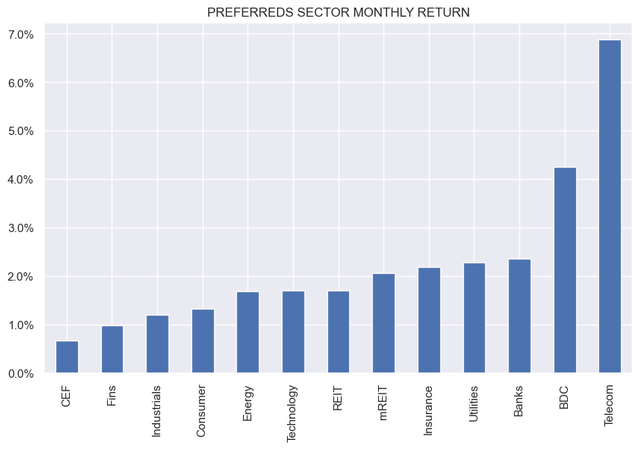

Most popular shares had week as long-term Treasury yields continued to fall. Because the starting of the month, all sectors are within the pink, with larger beta sectors main the way in which.

Systematic revenue

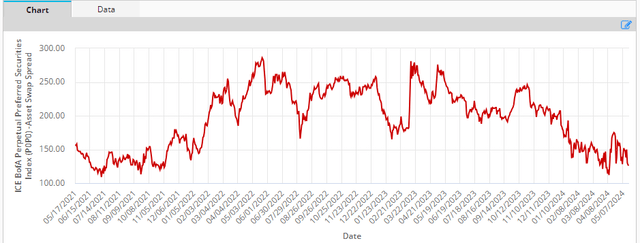

Prime credit score spreads have narrowed once more after a current sharp fall, providing much less worth to traders, notably as Treasury yields are actually additionally decrease.

ice

Matters of the market

Assumptions concerning the redemption of most well-liked shares have been renewed. It’s believed that since short-term charges should not going to fall as a lot this 12 months as beforehand anticipated, this can inspire corporations to purchase floating fee devices. The same old suspects right here that folks usually suppose shall be purchased out are AGNCN, NLY.PR.F, RITM.PR.A and RITM.PR.B, and plenty of others.

The truth that steady short-term charges can encourage issuers to exchange their floating debt with longer-term debt could appear intuitive; nonetheless, the market is assumed to be stationary. When the consensus originally of the 12 months was for 6-7 cuts, the 5-year Treasury yield was round 3.85%. Now, if folks count on 1-2 slopes, the yield is 4.45%.

In different phrases, it is much more costly to exchange floating fee loans with long-term debt right this moment than it was originally of the 12 months, when folks thought short-term charges had been coming down quick. There isn’t a such factor as a free lunch. Many corporations should be resentful that they did not publish engaging lengthy returns initially of the 12 months as a result of they thought falling quick charges would make their float less expensive to service. Now that short-term charges are anticipated to remain larger for longer, long-term charges have additionally risen, as anticipated.

One other factor to bear in mind is that these issuers can already refinance their bonds at decrease ranges – via repos or different secured amenities. AGNC will pay round 5.25% on repo as a substitute of paying nearly twice as a lot as AGNCN. Nevertheless, he has (but) chosen not to take action, which all begs the query of whether or not refinancing is a secure factor to do.

There are lots of causes corporations difficulty bonds, so simply because we see new bonds does not imply they exist to refinance seniors. On the one hand, credit score spreads are very slim. B-rated company spreads — about the place lots of the traditional suspects like BDCs and mortgage REITs difficulty bonds — are at their lowest stage in additional than a decade. Briefly, issuing bonds is affordable and corporations are profiting from them.

FRED

Another excuse BDCs and REITs difficulty bonds is that their portfolio property have elevated in worth, as has just about all the things else within the markets over the previous 12 months. This decreased their portfolios organically. In the event that they need to increase their leverage to the goal stage, they should difficulty extra debt.

One other indication that bond issuance would not essentially exist to redeem most well-liked inventory is that we’ve not seen a lot of it to this point. REITs resembling MFA and MITT have just lately issued bonds however have executed nothing with their most well-liked shares.

To be clear, we count on some quantity of leveraged buyouts, and certainly we have seen that in some sectors, particularly banks. Nevertheless, in our view, widespread redemption of floating property is unlikely. Furthermore, debt issuance can also be not a robust sign of upcoming senior repurchases.

Total, we proceed to favor many fixed-f-float trades with near-term name dates, particularly the place the yield low cost is excessive and the worth is beneath $25. This consists of the 2 RITM preferences talked about above, in addition to shares resembling SNV.PR.E. Both the inventory will increase to a really engaging yield, otherwise you get a small capital achieve (and a excessive annual return over a shorter interval).

Market commentary

Mortgage REIT PennyMac (PMT) preferences have appeared within the service. As a reminder, final 12 months the administration acknowledged that PMT.PR.A and PMT.PR.B should not going to maneuver to a floating fee as initially deliberate and can stay mounted. There was a Preferreds Weekly that mentioned a few of the mechanics. When the information broke, there was plenty of heated hypothesis about how the corporate could be buried in lawsuits, compelled to surrender and return to a floating fee.

Our view was that this was unlikely for various causes, each authorized and sensible, and right here we’re with PMT.PR.A declaring the identical mounted dividend for our first floating fee interval. We do not hear a lot concerning the avalanche of lawsuits, and the commentary appears to have shifted.

PMT.PR.A appears the very best within the trio with a yield of 8.8%. PMT Privileges is an efficient diversifier within the mREIT sector, given PMT’s origination platform, which offers some stability in ebook worth, as we noticed specifically through the COVID catastrophe.