ake1150sb

Introduction

I’ve given a Trusted Purchase advice for Energy Switch (NYSE:ET) in April. I’m very happy as a result of ET gave buyers virtually 5% revenue after my advice.

My basic and valuation updates present what’s there isn’t any purpose to change into much less optimistic about ET. Accelerated information middle funding is a big tailwind for all mid-sized firms, particularly giant ones like ET. Profitability is continually growing, which additionally helps to scale back the stability sheet. Current acquisitions point out that administration needs to strengthen ET’s place as some of the necessary firms for the US power sector. Valuation continues to be compelling and the excessive ahead dividend yield of seven.8% is secure.

Basic evaluation

The newest information on ET means that Mizuho shares are among the many finest power picks for July. I agree with Mizuho’s opinion as a result of ET’s fundamentals are bettering and the inventory nonetheless gives a compelling ahead distribution (dividend) yield of seven.8%.

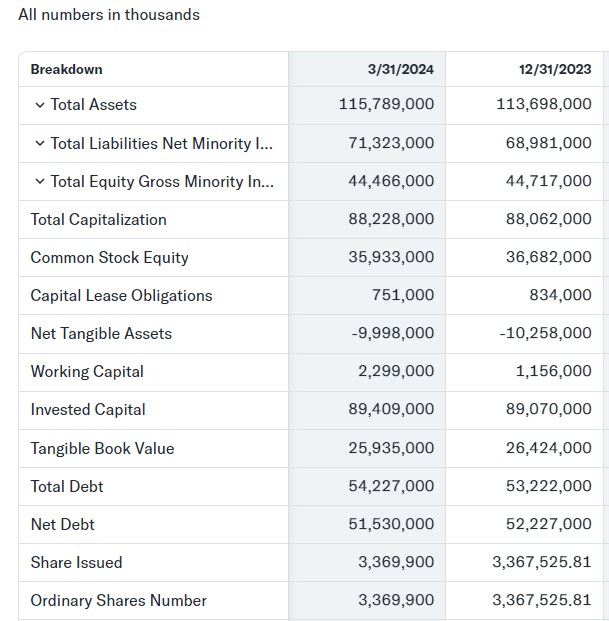

First, I will consider the security of dividend yields for shares. The newest quarterly report accessible is the one ending March 31, 2024. ET’s income was up 13.9% year-over-year within the first quarter, which is robust. When it comes to profitability metrics, buyers must be glad as properly. Gross margin elevated year-over-year from 17.7% to 18%, and working margin elevated from 10.86% to 11%. In consequence, ET’s money circulate from operations (‘CFO’) elevated year-over-year from $3.35 billion to $3.78 billion. A robust CFO allowed spending extra on investments, in addition to directing funds to scale back debt. Web debt fell from $52.3 billion to $51.5 billion. The enlargement of the CFO together with the deleveraging of the stability sheet bodes properly for the security of ET’s dividend.

Yahoo Finance

From a longer-term perspective, I need to emphasize ET’s efforts to consolidate its place within the Permian base. ET introduced on Could 28 that it’s buying WTG Midstream in a $3.25 billion deal. WTG Midstream owns and operates the most important privately held Permian fuel gathering and processing firm with property positioned within the coronary heart of the Midland Basin. To finance the deal, ET is proposing a $3.5 billion providing by means of a senior bond subject. In line with the corporate’s co-CEO Tom Lengthy, the consolidation “is sensible within the interim house.” Which means the corporate could think about extra acquisitions.

The transfer is probably going to assist solidify ET’s place as one of many important mid-cap firms for the US. As information middle prices skyrocket, demand for pure fuel is prone to be excessive. In line with TC Power’s govt vp and chief working officer of pipelines, the demand for pure fuel to energy information facilities will improve by 8 billion cubic toes per day by 2030. the most important reminiscent of Power Switch.

Lastly, ET’s property are fairly diversified and it has stable LNG exports. So the latest information {that a} federal decide has blocked the Biden administration’s ban on LNG exports is constructive for ET. US LNG exports are anticipated to indicate regular progress in 2024 and 2025.

Evaluative evaluation

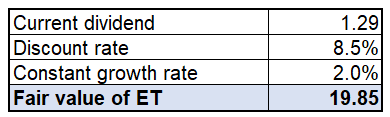

For a dividend machine like Power Switch, essentially the most applicable valuation strategy is the Dividend Low cost Mannequin (DDM). The present dividend is $1.29. The price of fairness is the low cost price for the DDM strategy, which is 8.5% for ET. A relentless progress price and equal to the long-term common inflation within the USA, ie. 2%.

Calculated by the writer

ET’s honest worth is $19.85, up almost 22% from its final shut. I discover this progress potential compelling, particularly if you add in ET’s excessive dividend yield.

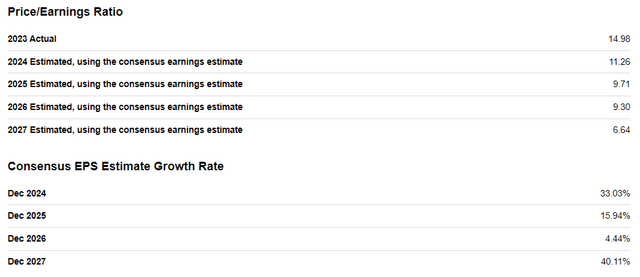

ET’s undervaluation can be highlighted by its P/E ratio, which is anticipated to fall to six.6 by FY2027. Wall Road analysts count on regular earnings-per-share progress over the following 4 fiscal years, resulting in a big discount in earnings per share.

on

With ET’s acquisitions accelerating, that are anticipated to drive income progress, and administration’s dedication to protecting prices underneath management, earnings per share enlargement will be anticipated. Due to this fact, ET could be very attractively valued additionally primarily based on ahead P/E ratio evaluation.

Mitigating elements

ET’s efficiency when it comes to share worth appreciation has been spectacular because the pandemic disaster. Over the previous three years, the inventory has returned 53% general, considerably higher than the S&P 500. Nonetheless, ET has misplaced 43% of its worth over the previous decade. Whereas the efficiency of the S&P 500 has been sturdy over the previous three years, I believe buyers must be conscious that it has been in decline over the previous decade.

on

The environmental controversy surrounding considered one of ET’s largest property, the Dakota Entry Pipeline (‘DAPL’), started to escalate in 2016 when the primary building permits had been issued. ET is affected by intense stress from environmental stakeholders who need the pipeline stopped. It’s troublesome to quantify the monetary influence of a possible DAPL termination; nevertheless, this can undoubtedly trigger disruptions to ET’s operations and adversely have an effect on income. DAPL’s environmental assessment has been delayed till 2025.

The geopolitical uncertainty of latest years makes it troublesome to foretell tendencies within the international power market. Whereas mid-cap firms are much less uncovered to adjustments in hydrocarbon costs, they’re affected by the worldwide stability of power provide and demand. Such uncertainty provides a layer of uncertainty about ET’s short-term return prospects.

Conclusion

ET’s stellar dividend yield of seven.8% stays secure as the basics are stable, and the latest administration transfer will assist solidify ET’s place as some of the necessary firms for US power. Accelerated information middle funding from tech giants is a robust secular tailwind for ET. Valuation stays engaging, which means ET is a “sturdy purchase”.