audio promoting

Plug Energy Inc. (NASDAQ: PLOW) continues to fail abysmally, regardless of the a. The corporate’s monetary prospects weren’t helped by a big authorities mortgage, and the preliminary pleasure shortly pale. My funding thesis stays bearish on the inventory regardless of the potential for robust help on the present worth.

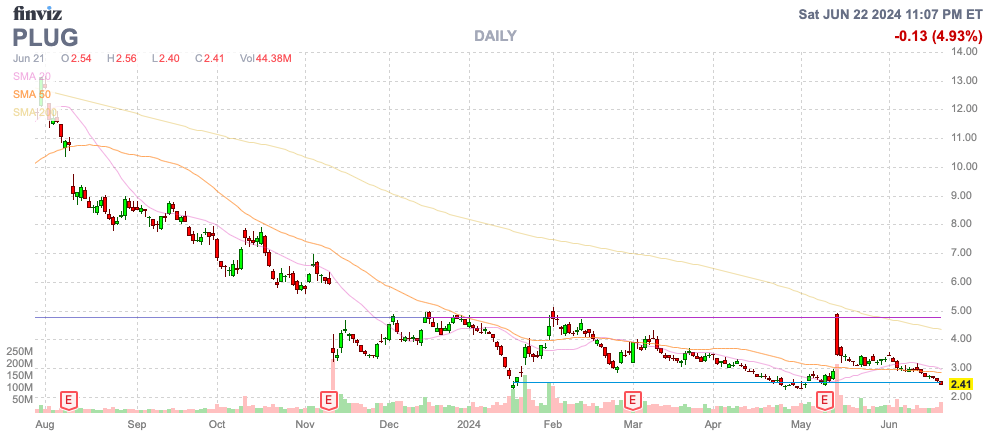

Supply: Finviz

Uncared for mortgage

Plug Energy rose to $5 on the again of a $1.66 billion conditional mortgage assure from the U.S. Division of Power. Whereas a inexperienced hydrogen firm can actually use low-cost authorities financing, the monetary efficiency will not change with further borrowing.

The mortgage assure has already been questioned by a US senator, and the mortgage is conditional. The deal apparently covers the development of as much as six inexperienced hydrogen crops.

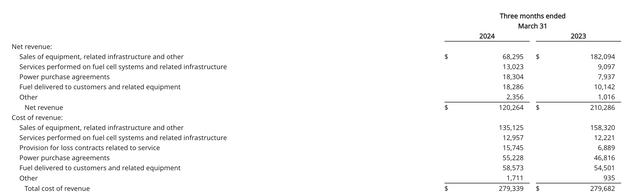

Latest outcomes for the primary quarter of 2024 present why a US senator might have some issues about lending $1.7 billion to a giant loser. Plug Energy took a very long time to lastly get a hydrogen plant up and operating on a business scale in Georgia, and gross sales fell to only $120 million within the quarter.

Plug Energy reported that income fell almost 43% from the earlier quarter and fell under analysts’ estimates by greater than $37 million. The corporate lately ramped up commercial-scale manufacturing of inexperienced hydrogen crops in Georgia and Tennessee to 25 tons per day (TPD), however gross sales have fallen.

Regardless of all the joy about reaching capability at these crops, gasoline income was solely $18 million towards $59 million in bills. These quarterly outcomes have been comparatively according to the 2023 quarter.

Supply: Plug Energy Q1 2024 earnings

In whole, revenues of $120 million have been offset by bills of $279 million. Regardless of the drop in income in comparison with the identical interval final yr, the full worth of income remained the identical.

Plug Energy efficiently decreased working bills to only $100 million within the quarter from $140 million final yr. Adjusted working bills of $103 million have been down from $131 million, a slight constructive as the corporate applied plans to chop prices by $75 million.

Once more, the issue is that Plug Energy does not even generate a constructive gross margin to cowl its decreased working prices. The corporate is engaged on a inexperienced hydrogen plant in Louisiana to extend capability to 40 TPD, however Plug Energy has but to point out an enchancment in monetary efficiency regardless of the Georgia plant beginning manufacturing of liquid inexperienced hydrogen in late January.

A standard frustration with the financials is the continued willingness to subsidize companies when clients ought to be keen to overpay to modify to scrub vitality. The corporate predicts it’s going to finish the yr with 65 TPD of unpolluted hydrogen gasoline, up from 50 TPD now. The issue is that Plug Energy is just producing 25 TPD now, and the Louisiana mission brings the full to 40 TPD. The corporate will provide solely 60% to 65% of demand, leaving Plug Energy ready to lose cash on 35% or extra of manufacturing. A enterprise should not have a detrimental margin

Massive Texas mission provides huge 45 TPD inexperienced hydrogen manufacturing. The most recent forecast is for a begin date of late 2025, which suggests Plug Energy will provide a major quantity of gasoline by means of a lot greater offtake from third events, the place prices are between $12 and $14 per kg, in comparison with gross sales of simply 6 as much as $7 per kg.

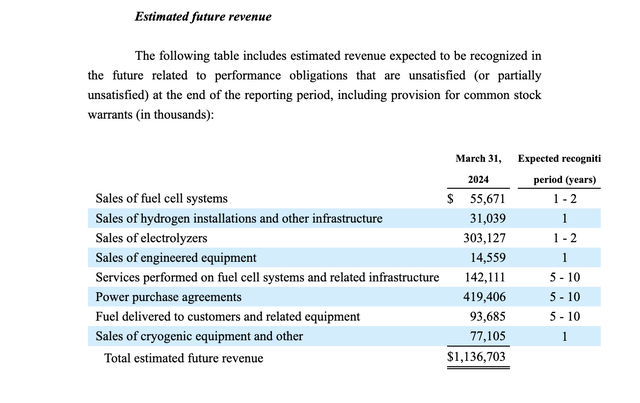

Even future income figures name into query Plug Energy’s potential to ever meet its monetary targets. The backlog is simply $1.1 billion, with important sums earmarked for electrolyzers and energy buy agreements. The inexperienced hydrogen gasoline enterprise is a minor a part of the story.

Supply: Plug Energy Q1’24 10-Q

Issues with cash

Plug Energy ended the quarter with a money stability of almost $400 million, with a cap of $220 million. The corporate has $210 million in convertible debt and several other different financing and lease obligations.

The issue is money stream: Plug Energy burned by means of $168 million within the quarter from operations. CapEx was one other $93 million, bringing the full quarterly burn to $261 million.

The corporate all the time sees low gross sales within the March quarter and loads of tools/electrolyzer tasks are within the validation stage, which is able to result in further gross sales within the close to time period. Plug Energy contributed simply 10% of gross sales within the first quarter, however the quantity was a lot nearer to 25% final yr, with quarterly income comparatively flat all year long.

Plug Energy didn’t forecast quarterly or annual gross sales, whereas prices are all the time excessive, even for an organization that’s projected to succeed in greater than a billion {dollars} in annual gross sales. The financials turn out to be dire after the corporate dramatically misses targets, and these losses from shopping for gasoline and electrical energy add up.

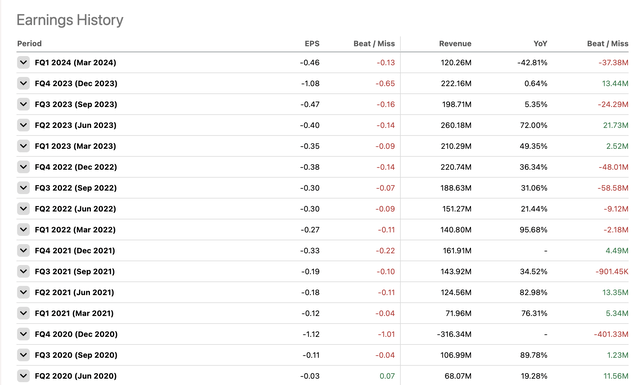

Analysts count on smaller losses going ahead, however forecasts are nonetheless for losses for the remainder of the yr to almost double from Q1 losses. The stability sheet doesn’t help this degree of losses and money burn.

To make issues worse, analysts didn’t present a transparent estimate of Plug Energy’s losses from Q2 2020.

Supply: In search of Alpha

The DOE mortgage is solely serving to the corporate cowl capital expenditures to construct new amenities totaling $1.7 billion. The mortgage will incur further curiosity prices and the administration crew has proven no self-discipline to show the inexperienced hydrogen crops right into a worthwhile enterprise with the necessity to terminate new provide contracts that aren’t financial.

Take it away

The important thing takeaway for buyers is that Plug Energy buyers proceed to face much more dilution whereas the inventory trades at lows under $2.50. The inexperienced hydrogen firm nonetheless has very risky gross sales, whereas prices are all the time elevated.

Plug Energy is about to report greater gross sales on the again of upper tools gross sales for the yr, however its key inexperienced hydrogen gasoline enterprise is underperforming. Buyers ought to keep away from the inventory due to its excessive money burn charge and certain want to lift further capital.