Rawpixel/iStock through Getty Photos

Funding thesis

On January 14, 2024, I suggested readers to keep away from the Invesco Dynamic Meals & Beverage ETF (NYSEARCA: PBJ) as a result of extreme estimation issues. Though his selection supplied extra potential for development than y Client Staples Choose Sector ETF (XLP), they’ve been extra unstable and of much less high quality, and this thesis has performed out properly over the previous 5 months. Since this text was revealed, PBJ has lagged XLP, the Vanguard Client Staples ETF (VDC), and the Constancy MSCI Client Staples ETF (FSTA) by 7-8%.

Looking for Alpha

Immediately’s article re-evaluates PBJ’s outlook in gentle of those comparatively weak earnings and the latest quarterly overhaul. I’m ready for a greater revenue alternative, however I’ll use completely different elementary indicators to find out whether or not it’s well worth the danger in comparison with the low-cost easy ETFs within the client staples sector. I hope you benefit from the evaluation.

Assessment of PBJ

Technique dialogue and efficiency

PBJ tracks the Dynamic Meals & Beverage Intellidex Index, choosing 30 US meals and beverage shares primarily based on elementary and technical elements comparable to value momentum, earnings momentum, high quality, administration actions and worth. Inside these classes are sub-factors comparable to return on belongings, valuation ratios and analyst estimate modifications, so PBJ is predicted to look moderately good on paper. I usually see this being the case, however traders needs to be conscious that the mannequin doesn’t emphasize the standard issue. For instance, the weighted common return on belongings of PBJ’s elements is 7.60%, in comparison with 9.75% for XLP. I’d count on this metric to be higher on condition that it is without doubt one of the metrics listed within the choice course of.

In accordance with methodological doc, The index is up to date quarterly on the finish of February, Might, August and November. Every safety receives a proprietary “mannequin rating,” and the Index consists of these with the very best scores in every sector and market capitalization group. Primarily based on my overview of holdings, bigger corporations obtain extra weighting than smaller corporations. That is why the common market capitalization of the ten largest holdings is $65 billion, in comparison with $6.5 billion for the ten lowest holdings.

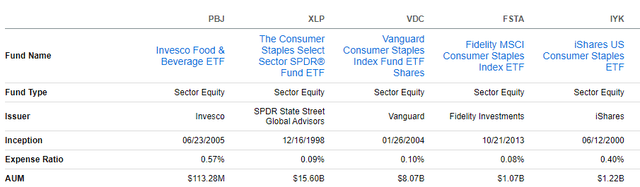

Lastly, I believe PBJ’s expense ratio of 0.57% is extreme. XLP, VDC and FSTA have expense ratios between 0.08% and 0.10%, and even the multi-sector iShares US Client Staples ETF (IYK) fares barely higher in charges with an expense ratio of 0.40%.

Looking for Alpha

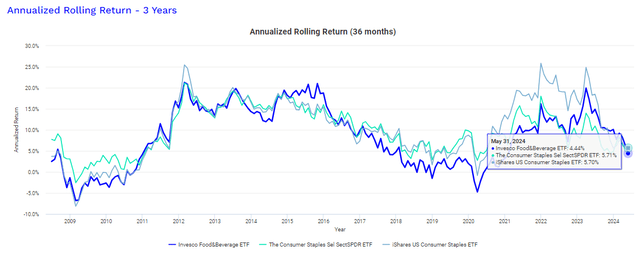

PBJ expense ratio and inconsistent efficiency monitor report in all probability helped by its low $113.28 million in belongings below administration. Its three-year trailing line of returns hardly ever beats XLP’s, and whereas previous efficiency is not any predictor of future efficiency, there’s little justification for charging such a big quantity for a fund that is extra suited to merchants than traders.

Portfolio visualizer

PBJ evaluation

Composition of PBJ vs. XLP, VDC, FSTA, IYK

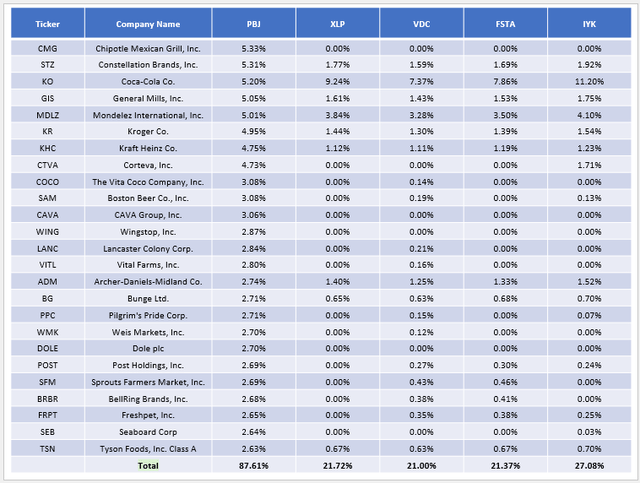

The next desk reveals the cash-adjusted allocations for PBJ’s prime 25 holdings, which make up 87.61% of the portfolio. One purpose to contemplate PBJ is that its composition is sort of completely different from XLP, VDC, FSTA and IYK. Except Coca-Cola ( KO ) and Mondelez Worldwide ( MDLZ ), most have little to no illustration in plain vanilla funds. As an alternative, they’re dominated by megacaps like Procter & Gamble ( PG ), Costco ( COST ), and Walmart ( WMT ), three shares excluded from the PBJ.

The Sunday Investor

PBJ elementary evaluation

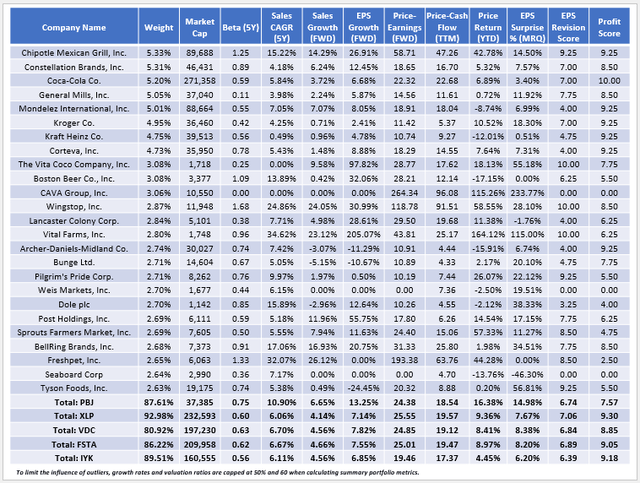

The next desk presents chosen fundamentals for these prime 25 holdings. I’ve additionally included abstract metrics for the 4 friends under.

The Sunday Investor

Listed here are 4 observations to contemplate:

1. PBJ has a five-year beta of 0.75, which is considerably greater than XLP, VDC, FSTA and IYK. Which means that some defect safety is waived, and traditionally it has been. PBJ fell 34.22% in the course of the subprime disaster between November 2007 and February 2009, in comparison with 28.12% for XLP, and it hasn’t carried out as properly in Q1 2020 both.

Portfolio visualizer

The benefit of a better beta portfolio is that it will possibly seize extra potential. Nonetheless, this isn’t a typical objective for traders on this sector. The elemental evaluation desk identifies a number of small- and mid-cap shares with betas near or higher than unity, so the distinction in dimension is the first supply of this added danger.

2. Smaller corporations usually supply higher development potential, and that is proven by shares like The Vita Coco Firm (COCA) and Important Farms (INT), which have projected revenue development charges of 97.82% and 205.07%, respectively. I’ve capped them at 50% to calculate PBJ’s projected earnings development fee of 13.25%, however even then it is virtually double its friends.

There are solely about 100 U.S. Client Staples shares with a market cap over $1 billion and a median ahead earnings development fee of simply 7.31%. Subsequently, I’m assured that the company mannequin is the dominant development issue. I discovered the identical with different Invesco Defensive Sector ETFs primarily based on the Intellidex Defensive Sector Indexes, with projected earnings development charges in comparison with these benchmarks of the sector as follows:

- Invesco Dynamic Biotechnology & Genome ETF (PBE): 11.79% vs. 8.62%

- Invesco Dynamic Leisure & Leisure ETF (PEJ): 16.64% vs. 7.09%

- Invesco Dynamic Prescription drugs ETF ( XLV ): 9.90% vs. 8.62%

3. As I discussed earlier, the mannequin doesn’t emphasize high quality. PBJ’s sector-adjusted earnings efficiency, primarily based on In search of Alpha Issue Grades estimates, is decrease than XLP’s (7.57/10 vs. 9.30/10), which I consider is the more than likely supply of its long-term underperformance. As an alternative, the mannequin emphasizes momentum. Contemplate how its elements are up 16.38% year-to-date, however the ETF’s value is down 2.03%. The discrepancy pertains to turnover calculated at 95% for the latest monetary 12 months. Particularly, 13/30 of the present holdings are new to the fund, together with CAVA Group (COFFEE) and Important Farms, up 115.26% and 164.12% YTD. Sadly, they weren’t picked to begin the 12 months, and now traders should take care of their lofty valuations.

4. Final time I advisable PBJ was August 5, 2023, and the ETF had a small complete return achieve of 0.49% after that, in comparison with XLP’s lack of 1.49% earlier than my downgrade in January 2024. I felt assured in my score on the time , as a result of PBJ was buying and selling at a five-point low cost to ahead earnings relative to XLP utilizing the easy weighted common methodology (18.88x vs. 23.80x). This low cost is critical to make PBJ a profitable commerce given the added danger, decrease high quality and better charges.

Sadly, regardless of its weak latest efficiency, PBJ solely gives a one-point low cost to ahead earnings (24.38x vs. 25.55x) and trailing money stream (18.54x vs. 19.57x). IYK’s valuation appears probably the most enticing (19.46x future earnings, 17.37x trailing money stream). Whereas it does not supply the identical upside potential as PBJ, its fundamentals are aggressive with XLP, VDC and FSTA.

Funding advice

PBJ is a high-fee meals and beverage fund primarily based on a proprietary mannequin that emphasizes development and momentum. Sadly, the standard is persistently poor, a characteristic that I believe has led to poor long-term profitability. To offset this, I counsel readers search for steep valuation reductions within the 4-5 level vary to future earnings, and since that is not the case right now, I do not suggest shopping for. Thanks for studying and I look ahead to your feedback under.