Michael We

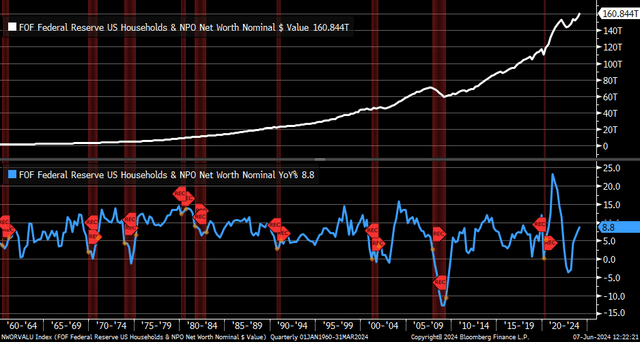

U.S. family fairness soared to an all-time excessive. Shares are up 15% in 2024, as measured by the S&P 500, whereas the bond market has recovered amid falling yields in current weeks. Worldwide shares have US mega-cap shares have underperformed, however have additionally rallied effectively because the begin of the 12 months, though home small-caps have flatlined.

General, the rise in monetary asset costs and the restoration within the property market are constructive components for households, and so they proceed to hunt – and pay for – monetary recommendation. One of many beneficiaries of this actuality Monetary LPL (NASDAQ: LPLA).

i repeat a purchase ranking on the $22 billion market cap funding advisory agency. EPS development is predicted to be stellar subsequent 12 months by means of 2026, whereas its valuation, at my variety, at a worth for such a stable earnings trajectory. The LPL chart can also be the most effective that may be discovered available on the market at this time.

Again in January, after I upgraded the inventory to Purchase from Maintain, I anticipated buyers to start to see LPL’s modest valuation given the bettering monetary market traits (rising fairness costs are a tailwind for asset managers) could be a boon. This typically continued with asset development beneath administration traits. The inventory is up about 20% from the earlier evaluation.

The household’s web price reached new highs

Kevin Gordon

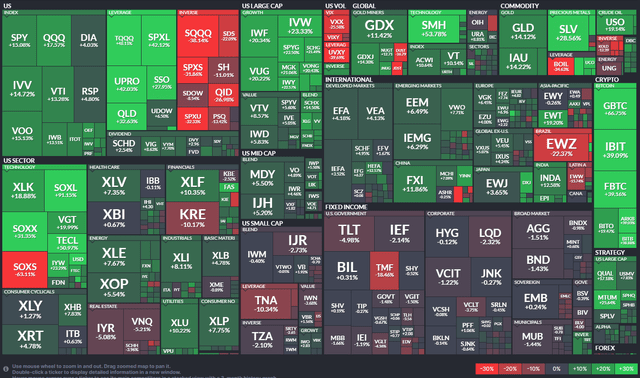

Yr-to-date ETF efficiency heatmap: Robust positive aspects

Finviz

LPLA is the biggest impartial broker-dealer within the U.S. with $1.2 trillion in consumer belongings, in response to Financial institution of America International Analysis. The agency helps greater than 22,000 monetary advisors nationwide by means of a spread of providers together with brokerage and advisory providers, funding options, cybersecurity know-how and platforms, operational assist and compliance.

Again in April, the LPL reported a stable set of quarterly outcomes. Q1 non-GAAP EPS of $4.21 beat the Wall Avenue consensus estimate of $3.82, and income of $2.8 billion, up 17% year-over-year, topped $110 million {dollars}. Robust advisory charges, increased commissions and prices beneath management all helped LPL obtain its first revenue since FQ1 2023. Nonetheless, web new asset development for the quarter fell to simply 4.9% year-on-year.

Nonetheless, its administration expressed confidence in earnings acceleration within the coming quarters, and a smaller Fed charge minimize ought to assist the earnings trajectory. Its working leverage and usually steady enterprise mannequin are robust factors. The agency operates a small-cap enterprise with wholesome natural development within the RIA section. LPL has additionally traditionally used M&A for development. Then, simply final week, the corporate reported a stable 3.6% soar in whole advisory and brokerage belongings on the finish of Could in comparison with April. Web purchases totaled a document $15 billion in Could, representing a 15.3% year-over-year enhance in whole web new advisory belongings.

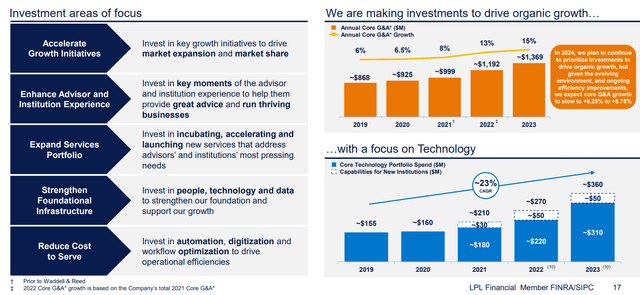

LPL is concentrated on development

LPL IR

The primary dangers embody a downturn within the macro economic system and the inventory market, which is able to result in a decline in payment earnings. A Fed charge minimize would truly be a headwind for LPL, whereas decrease demand from smaller banks may dampen earnings prospects.

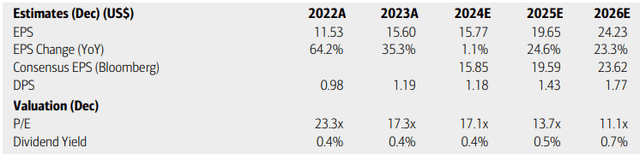

incl wageBofA analysts see the working room EPS is rising modestly this 12 months after two years of speedy revenue development. Earnings per share are anticipated to extend once more subsequent 12 months to 2026 and will exceed $26. Consensus Search Alpha’s earnings numbers aren’t as bullish in comparison with what BofA is forecasting, but it surely sees earnings development of seven% this 12 months with earnings development within the low-teens in 2025, adopted by 27% development by means of 2026. High the LPL line is projected to leap within the low to mid-double digits over the subsequent two years.

Dividends, in the meantime, are additionally rising at a brisk tempo, however yields on shares within the rising funding banking and brokerage trade ought to stay very low. With a P/E nonetheless under 20, the valuation stays intriguing.

LPL: Earnings, Valuation, Dividend Forecasts

BofA International Analysis

Given excessive sustained EPS development over the subsequent two years after a lull this 12 months, if we apply a 5-year common of 16.4 multiples to $21 in FY2026 earnings, the valuation could possibly be round $344. A PEG ratio strategy utilizing trailing 12-month earnings per share of $15.50 justifies a 30x a number of, assuming a 20% common earnings development charge. That valuation places the inventory a lot increased.

For now, I will be conservative with my elementary goal rising to $344 based mostly on a sustained excessive earnings forecast, making the inventory nonetheless a purchase. This can be a important enhance from my earlier estimate in mild of long-term sustainable income development. In January, I targeted on EPS traits for this 12 months and subsequent, however with 2026 extra in sight, the bullish case has develop into even stronger.

I believe at this time’s Wall Avenue valuations are affordable given what LPL has achieved over the previous few years, in addition to the rising demand for monetary advisory providers. The agency’s deal with know-how options may additionally assist its backside line with out inflicting extreme value will increase, so alternatives for prime working leverage would assist Wall Avenue analysts’ upbeat earnings forecasts.

LPL: Robust EPS development warrants a excessive valuation

Searching for Alpha

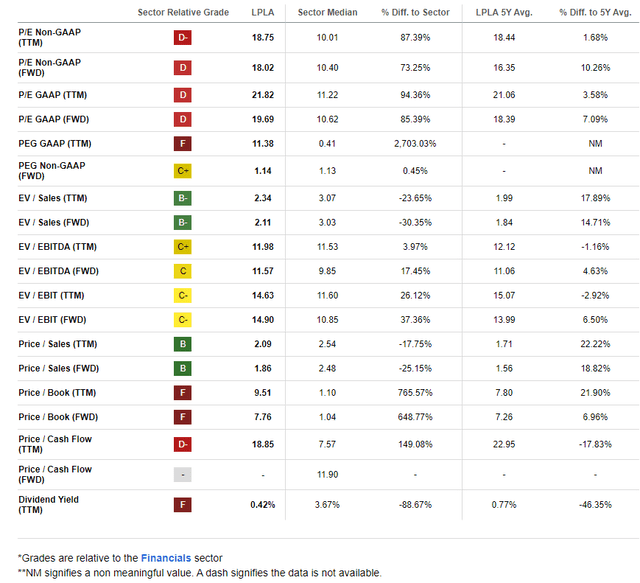

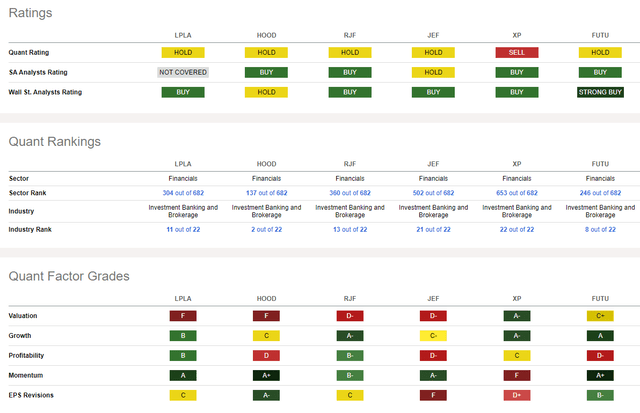

In comparison with their friendsLPL is characterised by excessive evaluation, however very excessive development charges subsequent 12 months and past are convincing. Furthermore, there’s a firm extremely worthwhile whereas his inventory worth momentum the ranking is dependable in a tape that didn’t favor shares of the monetary sector. Lastly, there was a combined set after Q1 earnings per share sellside forecast adjustments.

Evaluation of rivals

Searching for Alpha

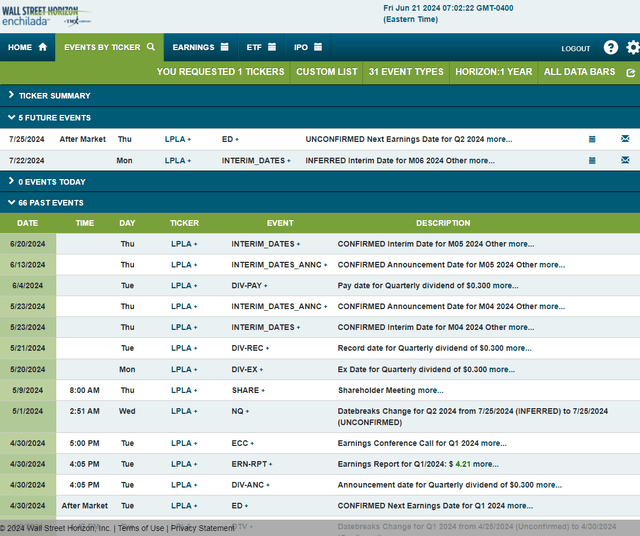

Trying forward, company occasion information offered by Wall Avenue Horizon exhibits an unconfirmed Q2 2024 earnings date on Thursday, July twenty fifth for AMC. Earlier than that, LPL will launch its June interim AUM figures on July 22.

Danger calendar of company occasions

Wall Avenue Horizon

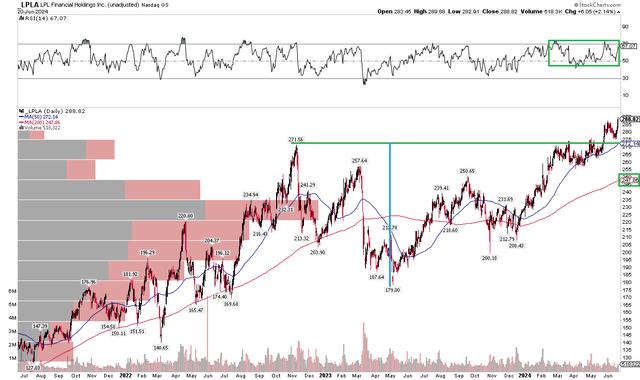

Technical reception

With massive earnings development on the horizon, a positive trade setting and earnings a month forward, LPL’s schedule is spectacular. Notice within the chart under that the inventory has just lately hit new all-time highs following a key bullish breakout final month. The RSI momentum oscillator on the prime of the chart can also be in bullish territory, with the indicator line not dipping under 40 this 12 months. With the long-term 200-day transferring common rising and the inventory additionally above the short-term 50 dma, the underlying pattern is clearly headed development

I see assist on the late 2022 excessive round $272, whereas a possible upside technical goal is $365 based mostly on the $93 top of the late 2022-Q2 2024 consolidation vary, which appears like a bullish cup and deal with sample.

General, the LPL chart is stable after the breakout to the upside. Each its RSI oscillator and its transferring common auger for increased costs forward.

LPLA: Bullish breakout to new highs, robust momentum

Stockcharts.com

Backside line

I reiterate my purchase ranking on LPL. I see the inventory as undervalued at this time, given its robust earnings per share development over the subsequent 12 months to 2026, whereas its technical state of affairs can also be encouraging.