jxfzsy

US 10-year Treasuries at 4.5% are neutrally rated even when inflation falls (as actual yields needs to be greater)

We see the 10-year Treasury yield (US10Y) prone to rising to five% for whereas CPI and PCE figures are printed at 0.3% month-to-month (or greater). However the newest Core PCE deflator was 0.2% for the month. A sequence of those may finally immediate the Fed to taper. So the place are we now with the ten yr yield?

First, notice our principle that the Zeros supplied a reasoned imaginative and prescient of an “common impartial surroundings.” U.S. inflation averaged about 2.5 p.c that decade, matching a mean Fed funds charge of three p.c and a mean 10-year Treasury yield of about 4.5 p.c. See extra right here.

Primarily based on this, if we for a delicate touchdown and curbing inflation, the funds charge mustn’t fall beneath 3%. This determines the ultimate flooring. This restrict might be pushed greater, say within the area of 4%, if some vulnerability to inflation persists. All that is related for situations the place 10-year yields will be achieved.

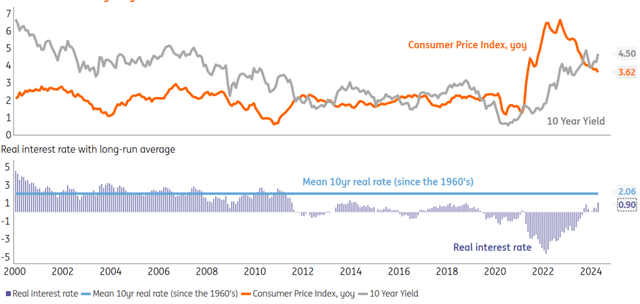

Our evaluation of zero durations reveals that the equilibrium 10-year yield is round 4.5%, which truly impacts the fund’s flooring charge of three%. A better funds flooring may simply push the 10-year above 4.5%. Mainly, the present 10-year yield would not essentially signify outrageous worth, even when inflation is falling.

The actual US 10-year charge remains to be only one%. Impartial degree – 2%. Decrease CPI doesn’t essentially imply decrease productiveness…

Supply: ING estimates, Macrobond

A charge reduce may result in overdrafts falling by as much as 4% over 10 years

Moreover, we notice that the typical 10-year actual return because the Nineteen Sixties has been round 2%. Now it is about 1% (based mostly on printed inflation charges). If we assume that we return to “regular charges” (and we are going to), then we needs to be a 2% actual charge over a 10-year time period. See the graph above.

If inflation falls by 1%, the actual charge will likely be 2%. Nonetheless, this leaves the 10-year Treasury yield unchanged. That is necessary as a result of it highlights the truth that the 10-year Treasury yield would not essentially have a very good cause to fall just because inflation is falling.

However this is why the 10-year Treasury yield may fall:

A charge reduce often coincides with a fall in longer-term yields. See right here for extra particulars; this reveals that vital drops are typical earlier than and after the primary reduce. On that foundation, if the Fed begins tapering within the coming months, a transfer to 4% (or decrease) for the 10-year Treasury yield wouldn’t be out of the strange.

In reality, we name for such progress. This could deliver with it a rationale for asset managers to go tactically lengthy early (earlier than the primary drawdown) and for legal responsibility managers to both problem or lock charges later (after the primary few cuts). Nonetheless, we consider this window will likely be quick (no various months) and can finish nicely earlier than the Fed completes its rate-cutting cycle.

In any case, 5% stay the extent for 10 years, which remains to be within the dialog

Nonetheless, a 10-year Treasury yield of 4% (or beneath) shouldn’t be an equilibrium consequence, as a charge reduce would coincide with the formation of a constructive yield curve. A standard (common) zero fashion curve would cowl a time period premium of 150 bp. within the 10-year yield.

That shortly returns 10 years again at 4.5%. And if the funds charge cannot get again to three% and, say, the 4% low, then we might quickly see the case for a 5% 10-year yield. Think about fiscal / issuance pressures and we are able to additionally attain 5%, even with a 3% funding flooring.

Backside line: The 4.5% 10-year yield we see immediately is neither excessive nor low. It’s a blow to what we contemplate to be impartial. Stability is a giant phrase, however we predict it is spot on right here. Even when inflation falls, the 10-year actual yield is so low that it has no proper to fall merely on that foundation.

The important thing ingredient is the discount in charges, as this often ends in decrease charges for longer durations. We’ll decline to 4% over 10 years as discounting tightens as Fed charge cuts and tapering start.

However this extra is destructive. So, barring a system crash, do not count on to remain there. Throw in further fiscal elements and the 5% deal with seems fairer (greater than regular), publish the early phases of a charge reduce.

So the extra pure medium-term result’s that the 10-year yield will are likely to settle a lot nearer to five% than 4%.

Content material disclaimer

This publication has been ready by ING for informational functions solely, whatever the wealth, monetary state of affairs or funding targets of the actual consumer. The knowledge doesn’t represent an funding suggestion, nor does it represent funding, authorized or tax recommendation or a suggestion or solicitation to purchase or promote any monetary instrument. Learn extra

Authentic publish

Editor’s notice: The bullet factors for this text had been chosen by the editors of Searching for Alpha.