les01

Whereas Halliburton (NYSE: HAL) Over the previous 12 months, the North American enterprise has confronted difficulties, which at the moment are being offset by elevated exercise internationally. The corporate’s earnings proceed to develop, however that does not matter for the inventory worth, which has been fairly risky. certain over the previous two years.

The final time I wrote about Halliburton, I instructed that it was weak as a result of unsure macro circumstances and its reliance on OPEC to prop up oil costs. It seems that tender financial information and deliberate OPEC provide cuts at the moment are placing strain on the inventory worth.

Market circumstances

Regardless of the rising indicators of financial weak point over the previous 1-2 years, Halliburton stays bullish on vitality demand. The corporate expects crude oil demand to extend by 1.2-2.3 million barrels per day in 2024, pushed by non-OECD international locations.

I are likely to suppose so going ahead, demand will disappoint as financial circumstances proceed to weaken. With the danger of a recession largely forgotten, fairness markets are transferring larger amid robust earnings from a number of firms. A collection of financial information counsel that the US financial system continues to melt regardless of the huge fiscal stimulus. For instance, manufacturing information stays weak and pressures on shopper spending proceed to rise regardless of robust employment. Nevertheless, the labor market is weakening, and there’s a threat that it’ll finish sometime.

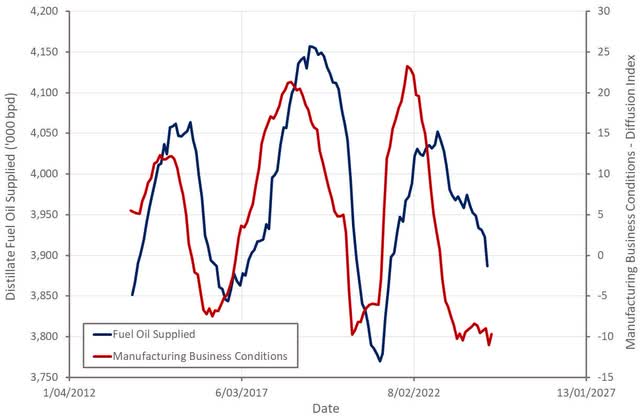

Determine 1: Gas oil manufacturing and enterprise circumstances in america (supply: created by the writer utilizing Federal Reserve information)

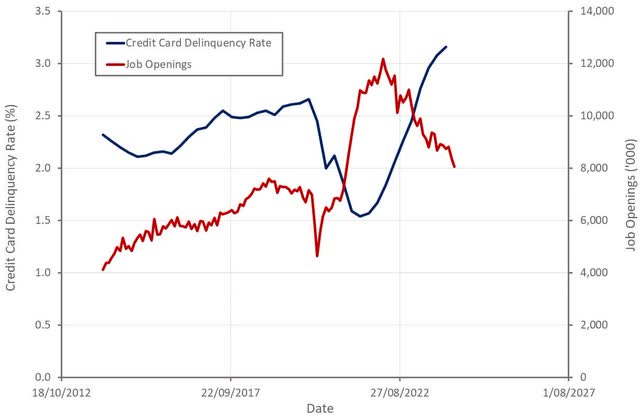

Determine 2: US bank card delinquency charges and job vacancies (supply: created by the writer utilizing Federal Reserve information)

Regardless of a reasonably robust improve in demand lately, oil provides have been greater than capable of sustain. The one motive there hasn’t been an even bigger provide glut is OPEC’s willingness to chop manufacturing to assist costs. That now seems to be coming to an finish, as voluntary provide cuts totaling 2.2 million barrels per day have been halted since October.

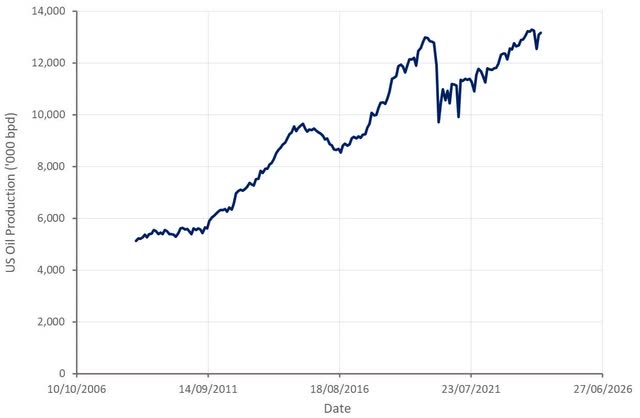

Determine 3: US oil manufacturing (supply: created by writer utilizing EIA information)

As for the providers market, Halliburton believes that curiosity in unconventional reservoirs is rising worldwide, most notably Argentina. Saudi Arabia can be channeling funding from offshore to non-traditional (Jaffura). Firms like Nabors ( NBR ) proceed to deploy rigs in these areas, pointing to progress alternatives for Halliburton.

The U.S. frac market ought to be supported by service firms’ capability self-discipline. This may increasingly create a decent market when demand picks up, however it will not save service firms in a downturn. Halliburton additionally believes that West Africa and the North Sea may develop into areas of power in 2025 and past.

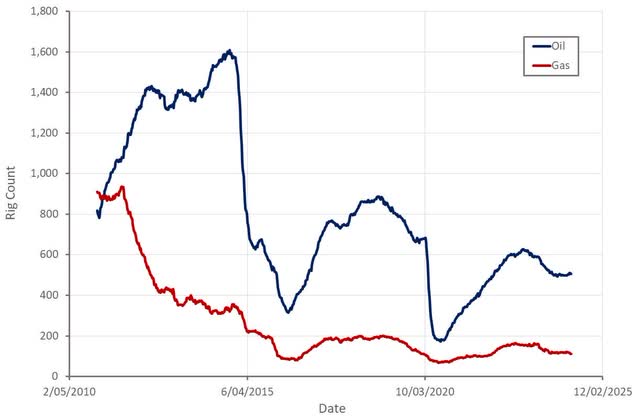

Determine 4: US rig depend (supply: created by writer utilizing information from Baker Hughes)

Halliburton Enterprise Updates

Whereas I’m fairly destructive on Halliburton’s near-term outlook, that is because of the nature of oilfield providers and deteriorating demand. Lately, Halliburton has carried out an excellent job of strengthening its enterprise, growing its publicity to offshore areas, synthetic carry and manufacturing chemical compounds. This was supported by small mergers and acquisitions so as to add sure technical capabilities. Halliburton has additionally invested in differentiating its core providers, reminiscent of hydraulic fracturing.

This consists of the corporate’s ZEUS platform, which gives electrification, automation and subsurface diagnostics. ZEUS is reported to cut back prices and enhance operational effectivity. Halliburton’s SmartFleet Fracture Monitoring System is an automatic system for real-time subsurface measurement. Understanding fracture progress turns into more and more essential as core acres lower and parent-child interventions improve. Halliburton automation will increase the effectivity of simultaneous fracturing and optimizes gear operation to increase life and enhance reliability.

Halliburton additionally launched a brand new directional drilling system focusing on unconventional species in North America. The iCruise CX system is designed for advanced curves and lateral functions. This helps cut back effectively time via quick drilling, quick descent occasions and quicker casing drilling. It additionally helps operators precisely place wells within the reservoir because of its exact management capabilities.

Regardless of these efforts, Halliburton continues to be held again by the truth that it operates in pretty commodity markets which might be comparatively capital-intensive and supply low progress charges. In the meanwhile, providers like ZEUS are a bonus, however within the occasion of a downturn, operators will develop into extra cost-conscious. Moreover, electrical fleets will develop into the norm over the following few years as service firms improve their fleets.

Monetary evaluation

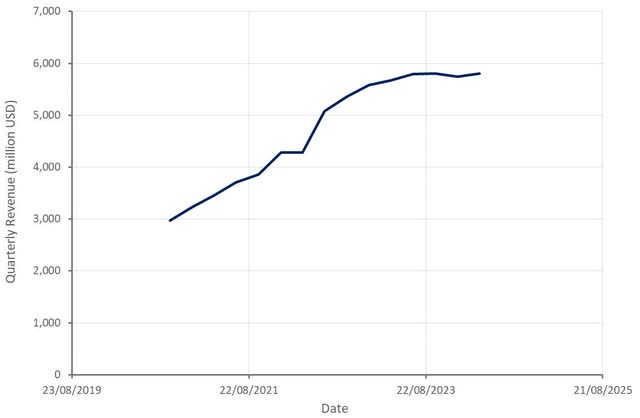

Halliburton’s first-quarter income was $5.8 billion, up 2.2% year-over-year. Worldwide income elevated 12% to $3.3 billion, whereas North American income was $2.5 billion, down about 8% year-over-year. Progress was pushed by Latin America, which introduced in $1.1 billion, up 21% YoY. Excluding Latin America, Halliburton’s income was down about 1%. Though Halliburton’s North American enterprise is struggling, it’s considerably insulated from present circumstances by the truth that 40% of its gear is below long-term contracts.

Completion and manufacturing earnings had been $3.4 billion within the first quarter, down barely from the identical interval final yr primarily as a result of decrease strain pumping exercise. Halliburton’s drilling and analysis division generated $2.4 billion in income within the first quarter, up 7% year-over-year, pushed by drilling providers within the Center East and North America and total capability in Latin America.

Halliburton expects its worldwide income to develop by double digits in 2024. Worldwide markets are additionally anticipated to stay tight, resulting in margin enlargement. Onshore exercise in North America has reportedly stabilized, and Halliburton expects a gradual degree of exercise in 2024. Halliburton expects that LNG will ultimately result in a restoration in pure fuel exercise, however this isn’t anticipated till 2024.

Halliburton expects completion and manufacturing revenues to extend 2-4% sequentially within the second quarter, and drilling and appraisal revenues to extend 1-3% sequentially. That will result in roughly 3% year-over-year income progress, a slight acceleration after 4 straight quarters of declines.

Determine 5: Halliburton’s earnings (supply: created by writer utilizing information from Halliburton)

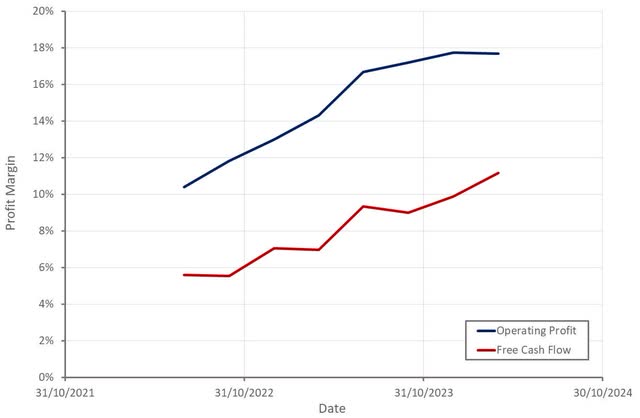

Within the first quarter, Halliburton generated $987 million in working revenue, with an working margin of 17%. The Completion and Manufacturing division’s working revenue margin was 20%, in comparison with a 16% margin for the Drilling and Analysis division. Halliburton expects each divisions’ profitability to develop within the second quarter.

Halliburton had $205 million in free money circulate within the first quarter. Working capital has been a drag on money circulate, however that is turning into much less of a difficulty as progress slows. Nevertheless, Halliburton’s capital expenditures are growing, offsetting a number of the enhancements in working capital. Free money circulate in 2024 is anticipated to be not less than 10% larger than in 2023.

Determine 6: Halliburton’s revenue margin (supply: created by writer utilizing information from Halliburton)

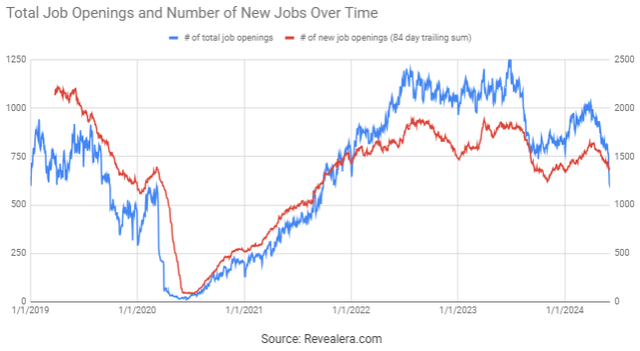

The latest sharp drop in job vacancies suggests additional deterioration in demand, which is more likely to weigh on Halliburton’s ends in the second half of the yr.

Determine 7: Jobs at Halliburton (supply: Revealera.com)

Conclusion

Whereas Halliburton seems low-cost based mostly on latest earnings, it is truly fairly totally valued when you think about the truth that its margins are most likely unsustainably excessive in the intervening time. That is determined by the extent to which service firms can show larger capability self-discipline than up to now, and the extent to which Halliburton has constructed actual pricing energy via service differentiation.

Whereas the corporate’s earnings are anticipated to proceed to develop, I imagine that financial weak point and the expectation of OPEC provide cuts will undermine Halliburton’s profitability because the yr progresses. Given the late stage of the present cycle, I imagine $20-25 could be a extra engaging entry level.

Determine 8: Halliburton EV/S ratio (supply: Looking for Alpha)