Thomas Barwick

Funding thesis: I’m bullish on Despegar.com.

In a earlier article in March, I argued that Despegar.com (NYSE: DESP) has the potential for additional development sooner or later because of robust development the gross quantity of bookings and revenue – the Brazilian market confirmed significantly excessive indicators.

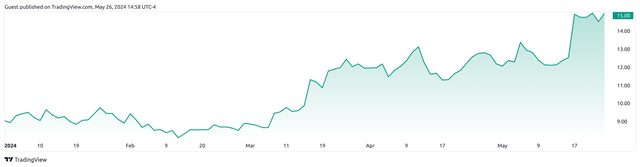

Since then, we have seen the inventory rise considerably – up greater than 37% since my final article.

TradingView.com

The aim of this text is to evaluate whether or not Despegar.com is able to seeing additional development sooner or later – based mostly on latest efficiency.

Productiveness

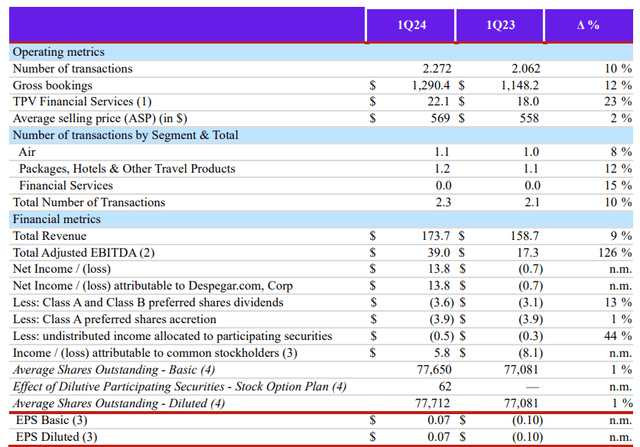

Trying on the monetary outcomes of Despegar.com for the first quarter of 2024, we will see that the gross variety of bookings elevated by 12% in comparison with the earlier quarter.

Monetary outcomes of Despegar.com for the first quarter of 2024

The corporate clarifies that on a impartial foreign money foundation, gross Bookings had been up 42% year-on-year, with robust demand in main markets similar to Brazil and Mexico a key driver of this development.

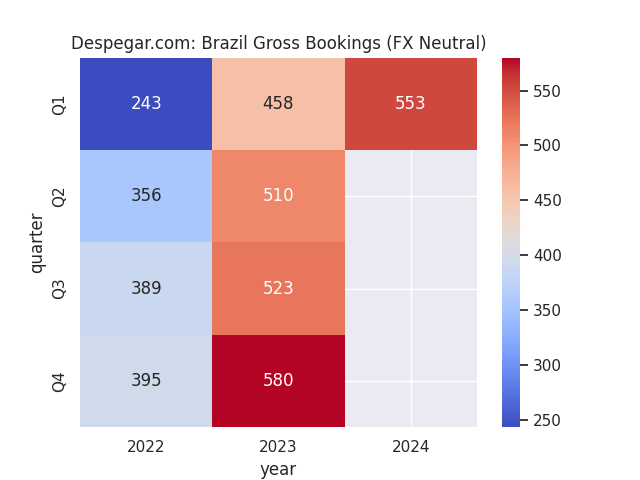

Trying on the Brazilian market, which is greater than twice the scale of Mexico, we see gross bookings on a foreign money impartial foundation up 21% year-over-year to $553 million.

The figures are derived from Despegar.com’s historic monetary outcomes. Warmth map created by the writer utilizing the Seaborn Python visualization library.

These development charges had been considerably greater than in Mexico, the place we noticed a 15% improve from $218 million to $250 million over the identical interval.

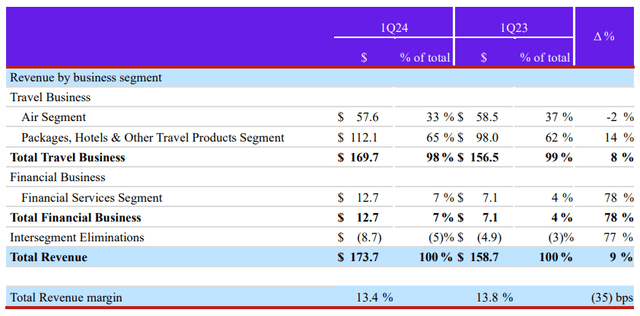

income by enterprise section, we see that the Excursions, Inns and Different Journey Merchandise section elevated by 14% in comparison with the prior 12 months quarter. Furthermore, this section now accounts for 65% of whole income, up from 62% within the year-ago quarter.

Despegar.com: monetary outcomes for the first quarter of 2014

With that stated, I feel the expansion in income and gross bookings over the past quarter has been spectacular.

From a stability sheet perspective, Despegar.com continued to cut back its long-term debt to $1.944 million in the newest quarter with a long-term debt to whole property ratio of 0.22%.

| December 22 | December 23 | March 24 | |

| Lengthy-term debt | 5119 | 2262 | 1944 12 months |

| Mixture property | 804172 | 898334 | 886062 |

| The ratio of long-term debt to whole property | 0.64% | 0.25% | 0.22% |

Supply: Figures (US$ 1000’s) obtained from Despegar.com quarterly reviews for 4Q22, 4Q23 and 1Q24 Lengthy-term debt to whole property (%) calculated by writer.

short-term liquidity, we see that the short ratio stays on the similar degree as final quarter, however money and money equivalents are down greater than 15% in comparison with final quarter.

| December 22 | December 23 | March 24 | |

| Money and money equivalents | 219167 | 214576 | 181495 |

| Accounts Receivable | 147806 | 183393 | 204494 |

| Whole present liabilities | 564466 | 671080 | 657754 |

| Fast ratio | 0.65 | 0.59 | 0.59 |

Supply: Figures derived from Despegar.com’s monetary outcomes for 4Q22 and 4Q23 (in 1000’s of US {dollars}, excluding fast ratio). Fast fee issue calculated by the writer.

Trying forward and taking dangers

We see that the Brazilian market continued to indicate robust development in gross bookings, whereas revenues within the excursions, lodges and different journey merchandise section confirmed double-digit development. When it comes to my view of the above outcomes and future outlook for the inventory, it’s clear that future development will probably be closely depending on the efficiency of all the Brazilian market.

Though the corporate’s stability sheet reveals a present debt ratio under 1 (indicating that the corporate doesn’t have sufficient liquid property to service its present liabilities), I imagine that the corporate’s low degree of long-term debt relative to its whole property signifies that traders will probably be keen to miss short-term money holdings so long as we proceed to see robust development in gross bookings and income – which we’re.

On condition that we have solely just lately seen earnings per share transfer again into constructive territory, it is possible that the expansion we’re seeing within the inventory has been fueled by income somewhat than earnings development per se.

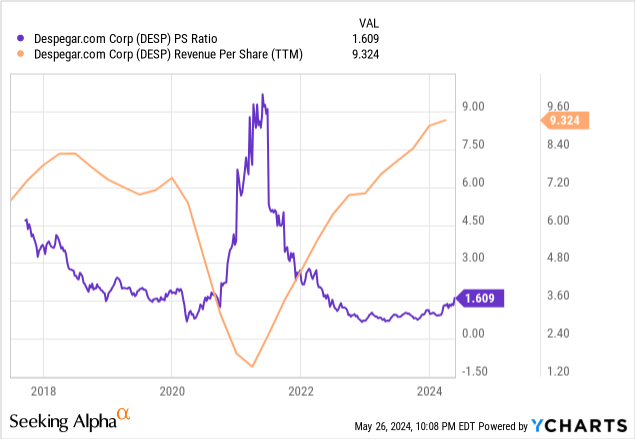

We see that the corporate’s price-to-sales ratio stays comparatively low in comparison with the general five-year development, whereas earnings per share are at a five-year excessive:

ycharts.com

From this attitude, I imagine the inventory has the potential for additional upside, supplied earnings development stays on a powerful trajectory.

When it comes to the corporate’s future technique, Despegar.com follows an “online-offline” technique in Brazil and Argentina, whereby the corporate opens bodily shops to enter the offline market in these nations. The aim of opening offline shops is to draw prospects who should not initially on-line, and on the similar time encourage future on-line exercise by constructing the belief of such prospects. Half of the market in Latin America as a complete stays offline, with offline shops and name facilities accounting for 13% of the corporate’s bookings.

I imagine that with ten shops open within the Brazilian market, this will present a big alternative to extend model consciousness and seize a good portion of the offline market within the nation.

One potential threat for Despegar.com at the moment is the potential for a slowdown in income between June and August, which represents the winter season for Brazil. With the anticipated seasonal slowdown in home journey at the moment, gross bookings could also be affected. Nonetheless, as detailed within the Efficiency part of this text, we have already seen gross bookings in Q2 and Q3 of final 12 months really improve in comparison with Q1. As such, the corporate nonetheless has potential for development on this market.

Conclusion

In conclusion, Despegar.com has recorded encouraging development within the Brazilian market and the corporate’s stability sheet continues to look wholesome. For these causes, I proceed to keep up a constructive view of Despegar.com.