YOKE

Earlier this yr, I wrote an article about Brookfield Infrastructure Companions (NYSE: BIP)(TSX:BIP.UN:CA)(BIPC), which is a world infrastructure participant with a market capitalization of over $14 billion.

My thesis was then based mostly on the next three traits of BIP:

- Sturdy present earnings supported by defensive cash-generating belongings (eg utility infrastructure, public-private partnership agreements, regulated midstream, and many others.)

- The lion’s share of money flows are linked to inflation dynamics or based mostly on built-in recurring income escalators that add a pretty natural development element.

- A stage of AFFO funds that leaves an honest chunk of inside fairness for BIP to reinvest and generate more money movement development along with the aforementioned escalators.

- An funding grade stability that de-risks the general funding thesis and likewise permits BIP to additional help the inorganic development side.

Basically, my determination investing in BIP has resulted in a comparatively respectable (and guarded) dividend yield of ~5%, coupled with a near-double-digit dividend development fee going ahead.

Two issues have occurred since my article was printed. First, BIP is underperforming the market, registering flat complete returns. Second, BIP launched its Q1 2024 earnings deck, bringing some attention-grabbing information for us to digest and contextualize with my thesis.

Let’s check out the Q1 2024 earnings deck and resolve if the upside stays.

Overview of thesis

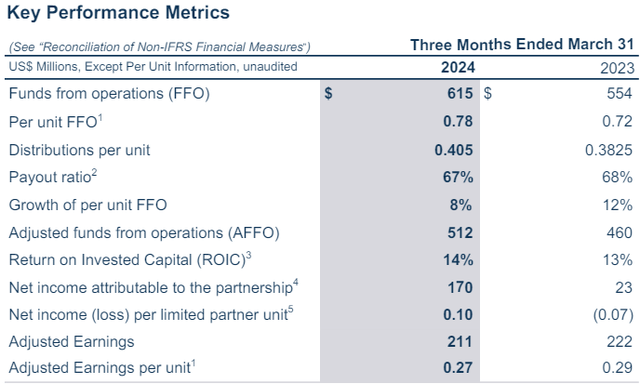

Q1 2024 earnings outcomes marked a big enchancment over final yr’s Q1. Enhancements will be noticed in all instructions. For instance, crucial metric – FFO per unit – elevated by 8%, which instantly affected the dividend development of ~6%. From the desk beneath, we will additionally see that the FFO payout ratio has remained unchanged (and even decreased by 1%), which signifies that BIP has certainly succeeded in executing its technique to accommodate dividend development on the expense of regular underlying money movement development. .

Extra BIP data for Q1 2024

A part of that is attainable attributable to built-in income shocks and indexing to inflation, however many of the development truly comes from elevated working capital and natural development paths supported by preserved FFO technology (ie, a conservative FFO payout ratio). For instance, notable drivers of FFO development this quarter had been the acquisition of German telecom towers, two information heart platforms and the acquisition of 40 retail information facilities.

Nevertheless, the capital recycling or asset rotation technique performed an much more vital function in driving FFO enlargement. Right here we should perceive that for BIP to realize its natural development goal of 6-9% each year, it should enterprise into large-scale M&A or natural growth tasks. Neither income escalators nor incremental capex by means of retained FFO technology is adequate to realize this purpose. So to maneuver the needle by way of FFO development, BIP wants to seek out recent capital to accommodate its development technique.

On this regard, the sale of elements of present tasks (equivalent to JVs) and even all the undertaking or asset is an optimum technique to entry liquidity in a shareholder-friendly method. Firstly, it avoids issuing further capital (diluting the present shareholder base) and secondly, it permits for the seize of embedded worth in tasks that had been initially BIP funded however now operational have the potential for larger realization IRR.

Here is a associated remark from a current earnings name by Sam Pollack, chief govt officer, about how BIP managed to get recent liquidity by divesting a few of its present portfolio to later use these proceeds to fund new acquisitions at larger ratios.

In April, we signed binding documentation for the sale of a fiber-to-fiber platform inside our French telecommunications infrastructure enterprise. The transaction is valued at greater than €1 billion and is anticipated to generate an IRR of 17% and a capital a number of of roughly 1.9x. We established this new fiber growth section in 2017 and rapidly scaled the enterprise to change into the main wholesale fiber to the house community within the area.

This yr (as of Q1 2024), BIP has made vital progress on the capital recycling entrance, producing roughly $1.2 billion in income, greater than half of its 2024 goal of $2 billion. Given this momentum, it appears like BIP will finish the yr with considerably extra unlocked worth in its portfolio than $2 billion, which in flip ought to additional enhance the expansion outlook. A very powerful factor on this context is to supply enticing tasks in order that administration can put recycled capital again to work to draw IRR.

Once more, studying Sam Pollock’s solutions to one of many analysts’ questions concerning the funding panorama, we will simply conclude that BIP is not going to have a lot issue find the place to deploy its capital:

sure. Look, I feel we — the whole lot needs to be risk-adjusted. However during the last yr or so, we have undoubtedly focused alternatives within the 15% to twenty% vary, with the potential to even obtain larger returns if sure elements of our marketing strategy come collectively. So we’re undoubtedly just a little bit grasping in the intervening time, to take considered one of Buffett’s phrases, I suppose, however we — I feel it is simply the atmosphere that we’re in proper now.

Lastly, BIP additionally managed to strengthen its capital construction this quarter with a number of notable refinancings. On account of sure debt relavers, greater than 90% of BIP’s debt was based mostly on fixed-rate debt with a median time period of greater than seven years. This offers the mandatory money movement stability and predictability for BIP to be energetic throughout the inorganic development part.

Backside line

BIP delivered one other quarter of stable FFO per unit development with out hurting the stability sheet. Income development got here from built-in rental escalators, however most significantly from a profitable capital recycling program that enabled BIP to shut new offers and improve exercise.

Present capital recycling dynamics coupled with a pretty funding house ought to present a powerful tailwind for BIP to proceed to develop FFO technology considerably whereas sustaining a powerful stability sheet.

In consequence, Brookfield Infrastructure Companions continues to be a pretty purchase with a ~5% dividend yield that can clearly develop over time.