mariusFM77

Introduction

British American Tobacco (NYSE: BTI) (OTCPK:BTAFF) continues to be an investor favourite, primarily due to the core nature of the enterprise, the cheap inventory and the excessive dividend yield it presents. There’s a sturdy bullish consensus inventory.

I’ve a extra reverse view. Though BTI is a world-renowned provider of tobacco merchandise, the enterprise is going through difficulties, notably affecting its core enterprise, which at present generates greater than 80% of revenues.

I posted my preliminary protection again in February with a extra detailed description of the enterprise and extra clearly laid out the arguments in my thesis. This text will present a quick description of the enterprise, assess the mandatory metrics for the thesis, and clarify why the inventory is probably not as low cost because the market suggests, resulting in my Maintain ranking.

Enterprise Description

As I often do once I publish the next articles, I’ll first briefly overview the enterprise description.

British American Tobacco is among the largest tobacco firms. Even in case you are not a client, you’ll have heard of a few of its manufacturers comparable to Camel, Newport and Kent. Cigarettes, referred to as Combustibles, are by far the corporate’s largest section, accounting for 83% of complete income in December 2023. Nonetheless, it isn’t the one enterprise.

The second largest section is known as rising classes, which stands out as the way forward for enterprise. This section manufactures varied varieties of non-flammable merchandise comparable to battery-powered tobacco-free gadgets (vapers), digital gadgets that warmth consumables comparable to flavored nicotine merchandise (heated merchandise), and pouches containing high-purity nicotine, water and others. substances (fashionable oral). This section accounted for 13% of gross sales within the final monetary yr.

Lastly, the standard oral section sells snus and snuff, that are smokeless tobacco merchandise which can be snorted or taken orally. In FY2023, this section contributed solely 4%.

Among the firm’s manufacturers could be seen under.

Annual report of BTI for 2023

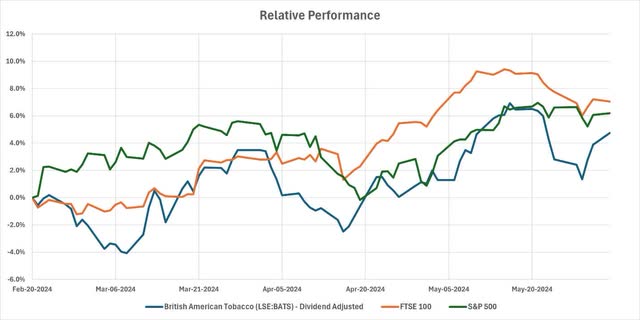

Inventory efficiency and Q2 earnings

Let’s check out how the inventory has carried out since late February once I printed my article. BTI’s inventory efficiency is dividend-adjusted as a result of dividend yield accounts for a big portion of this firm’s shareholder returns.

Throughout this era, the inventory barely underperformed the broader market. The adjusted return was 4.7%, whereas the Vanguard FTSE Europe ETF ( VGK ) and the S&P 500 ( SPY ) gained 7% and 6.2%, respectively.

S&P Capital IQ

BTI often publishes its half-year outcomes earlier than the June shut and a extra detailed half-year report, together with financials, a month later. On June 4 (the time this text was written), the corporate launched its preliminary closing outcomes for the primary half of the yr. It does not embody finance, but it surely provides us some attention-grabbing info.

Administration says the primary half was consistent with expectations and they’re on monitor to satisfy their FY2024 steering. The information highlights three primary areas.

First, the core gas enterprise continues to ship outcomes, though there are macroeconomic pressures. Administration notes that combustibles output is down 9% year-to-date as customers stay tight.

Second, funding in new classes continues. The corporate maintained international management by way of worth share with 41.1% in key markets. These positive factors have been primarily within the Americas (excluding the US) and Europe, offsetting declines within the US. The corporate continues to name for extra acceptable regulation of using a few of its merchandise. As well as, the corporate continues to introduce new merchandise on this section.

Final however not least, administration famous sturdy money technology and monetization of its ITC stake, which enabled the share buyback program.

These remarks point out that the corporate continues to be a powerful generator of money, which is used to return worth to shareholders and make investments extra within the new class section. Administration expects low single-digit income progress and a 3% decline in international tobacco quantity.

Preliminary thesis monitoring

My preliminary thesis for a Maintain ranking included three primary arguments. The sluggish transition to a smoke-free world, the deterioration of the core enterprise and the sustainability of the dividend. Let’s contemplate every individually.

Transformation with out smoke

This stays the primary bullish thesis. BTI is among the largest gamers within the manufacture of smokeless tobacco merchandise consisting of some merchandise in new classes and conventional oral merchandise.

The Higher Tomorrow initiative presents a imaginative and prescient of constructing a smoke-free world by shifting customers away from cigarettes to smoke-free options. This can be a clear purpose that the corporate units. With this initiative, the corporate plans to have 50% of its income come from non-combustible merchandise by 2035.

The corporate additionally focuses on hurt discount, which is a public well being technique that reduces the unfavorable well being results of smoking. This technique is consistent with the Higher Tomorrow initiative. Each of those methods emphasize that the corporate’s precedence is a smoke-free future and preparation for it.

In 2023, new class gross sales grew 12%, whereas conventional oral and combustibles fell 3.4% and 6.4%, underscoring the corporate’s strategic route.

Impairment of core enterprise

Whereas the non-flammable facet of the enterprise seems to be rising and receiving funding, the basics of the core enterprise are deteriorating. As talked about above, gross sales of flamable supplies have been down 3.4% in fiscal 2023. Outcomes for the 2024 semester haven’t but been launched, however should be watched.

There are two primary tendencies that we should always speak about. International recognition of cigarettes and adjustments in regulation.

Initially, in line with the Federal State Fee, there’s a long-term downward pattern within the variety of cigarettes bought in the US. There are various non-profit organizations, such because the WHO, which can be pushing for laws and placing stress on tobacco firms to promote fewer cigarettes and swap to more healthy choices. The corporate itself admits that cigarettes will change into a factor of the previous.

This thesis can also be supported by current regulatory developments world wide. The UK not too long ago handed a invoice banning anybody born after 2009 from shopping for cigarettes. On the opposite facet of the Atlantic, the ban on menthol cigarettes within the US appears set to proceed after the election. Nonetheless, the chance of a ban nonetheless exists.

Sustainability of dividends

On the time of writing, BTI shares present a dividend yield of 9.33%. This is essential to many traders. This excessive dividend yield ensures that BTI will seem on the funding screens of traders and funds which can be particularly eager about receiving dividends. Due to this fact, I contemplate it necessary to evaluate its sustainability.

In my earlier evaluation, I modeled the corporate’s anticipated money return over the following 5 years. I in contrast them to the monetary obligations that the corporate should pay. These monetary obligations embody dividends.

On this mannequin, we noticed that there’s a small buffer between money readily available and these monetary liabilities, which threatens dividends. Nonetheless, the corporate has began monetizing its share of ITC. BTI at present owns 21.6% of ITC, which is valued at $13.3 billion primarily based on ITC’s present market worth.

Due to this monetization, I consider the dividend threat is sort of nil and the stability sheet is nice. Dividend sustainability does not appear price monitoring anymore.

The market doesn’t count on operational enhancements

BTI is an attention-grabbing concept for a lot of traders because of its excessive dividend yield and cheapness of shares. When operating the standard DCF mannequin, I additionally count on a pleasant upside. A excessive dividend yield may also be thought of a sign of cheapness, as the corporate can return extra capital to its traders relative to its share worth.

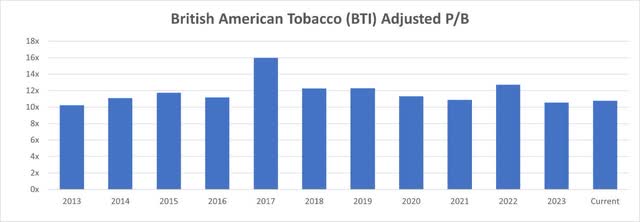

Nonetheless, the DCF mannequin alone is never enough to grasp the attractiveness of a worth. Utilizing historic price-to-book permits us to grasp how a inventory has been valued up to now and get an concept of how the market would possibly worth an organization sooner or later.

The adjusted price-to-book ratio exhibits that the inventory has at all times traded between the adjusted P/B vary of 10x-12x, with few exceptions. The inventory is at present buying and selling at 10.8x adjusted P/B.

S&P Capital IQ and writer

The market does not appear to consider that this firm will be capable to revolutionize its enterprise to generate increased returns on its property within the close to future. I agree with this evaluation, primarily due to the elemental developments we mentioned within the thesis monitoring part.

Conclusion

British American Tobacco is among the largest and main tobacco firms on this planet. Its manufacturers are well known and the corporate is properly positioned to spend money on non-combustible supplies. Nonetheless, on the similar time, the core enterprise is struggling.

Cigarette gross sales are nonetheless the most important section going through demand and regulatory challenges. Development in non-combustible supplies is clear, but it surely doesn’t appear to be sufficient to offset the decline within the core enterprise.

Shares look low cost; nonetheless, it at all times appears low cost. The historic adjusted price-to-book worth exhibits that the inventory has by no means priced within the working enhancements that will have led to the next return on property over the previous decade. At the moment, the multiplier is throughout the historic vary.

That is why I preserve my Maintain ranking on British American Tobacco. I consider traders ought to take one other have a look at various funding alternatives earlier than investing on this firm.

Editor’s be aware: This text discusses a number of securities that aren’t traded on a serious US alternate. Concentrate on the dangers related to these shares.