monkeybusinessimages/iStock by way of Getty Photos

Abstract

I am constructive about Brilliant Horizons Household (NYSE: BFAM). My total thesis is that BFAM will profit from elevated demand for childcare providers as extra girls enter the labor drive (leading to extra two-parent working households). BFAM is nicely positioned to capitalize on its scale and reputational benefit, which is troublesome to copy. Issues about near-term upside strain from macro headwinds ought to fade as soon as BFAM exhibits the market that it could proceed to develop at 10%.

Firm overview

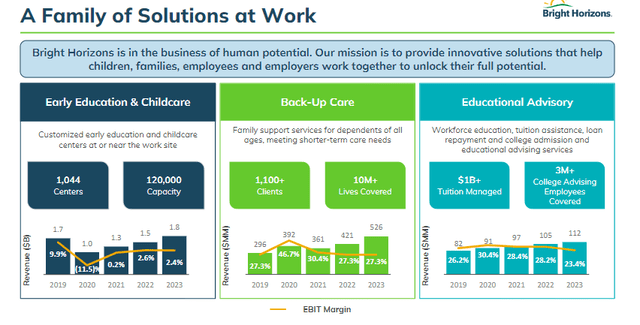

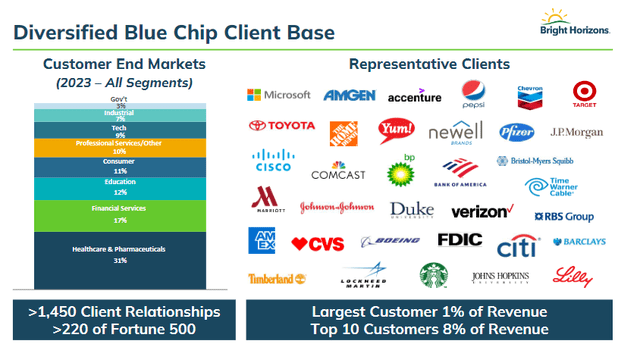

BFAM is a supplier of childcare providers to oldsters on behalf of sponsoring employers and has a protracted historical past of over 25 years. Up to now, BFAM has served greater than 1,400 shoppers, greater than 200 of which had been Fortune 500 firms. As of 1Q24, BFAM has 1,044 facilities that may serve as much as 120,000 kids. BFAM works in US (~73% of income), Europe (together with UK and Netherlands) and Australia, which accounted for 27% of whole income in FY23.

BFAM

There’s a rising want for childcare providers

There are numerous secular threats that improve the demand for childcare providers. Particularly, the variety of girls pursuing full-time careers is on the rise. That is in keeping with a report from the Bureau of Labor Statistics, the place extra working-age girls are working than ever earlier than (this report, whereas old-fashioned, offers a great perspective on this pattern). Accordingly, this elevated the proportion of households by which each mother and father work to 67%. To make issues worse, based on a research by The Pew, a major proportion of those mother and father have dwelling mother and father (age 65+) to take care of. After we put all these totally different dynamics collectively, it naturally signifies that mother and father have much less time to handle their kids, they usually want an answer to resolve this downside.

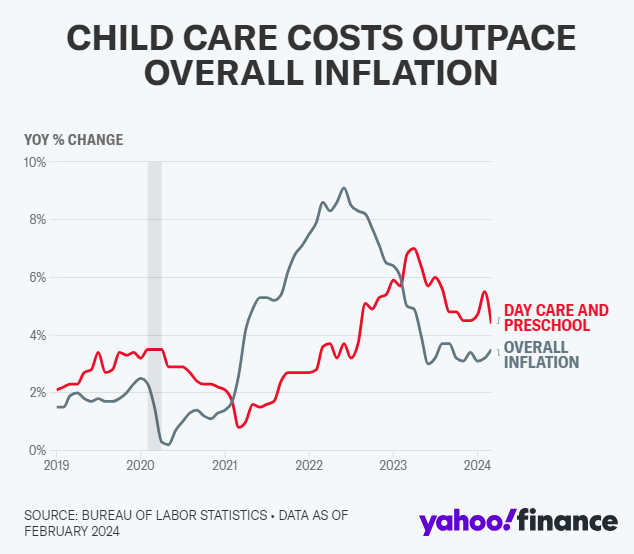

The tailwinds have additionally allowed childcare suppliers to repeatedly increase costs in keeping with inflation, and I anticipate this pricing energy to proceed, particularly for giant gamers like BFAM.

Yahoo

Scale and fame are key aggressive benefits

There are two essential aggressive benefits I see in BFAM: scale and fame.

Scale is a bonus for a wide range of causes. To begin with, the presence of scale (extensive regional protection) permits BFAM to fulfill the demand of huge companies that require little one care options in all their areas, provided that it’s simpler to take care of one participant than with a number of smaller gamers. Second, it means extra monetary alternatives to handle the trade’s greatest constraint to development: labor. You want sufficient manpower to run a middle, and provided that employment within the trade has but to return to pre-existing ranges, whoever can afford to pay extra will have the ability to retain or appeal to workers. As well as, larger monetary capability permits BFAM to higher climate financial cycles (covid has pressured the closure of many childcare amenities).

BFAM

Fame is maybe as necessary as scale benefit (I feel they go hand in hand). Fame is essential as a result of BFAM offers with kids and fogeys are very cautious about who takes care of their kids whereas they’re away. Due to this fact, I consider that folks will choose respected suppliers. This dynamic pushes employers to work with respected gamers as a result of they do not need to threat a backlash from abused kids. BFAM wins on this trade due to the blue chip buyer base it has constructed up over time. This creates a virtuous cycle for BFAM as employers in search of an answer supplier will worth BFAM’s buyer base. I consider the pure thought course of could be “Since these massive gamers belief BFAM, BFAM should be reliable”, and as BFAM works with extra shoppers, it turns into “extra respected”. The factor about fame is that it can’t be replicated in a brief time frame.

Total, with these two aggressive benefits, I consider that new entrants or subscale gamers won’t be able to simply disrupt BFAM’s market place.

Engaging working mannequin

BFAM BFAM BFAM

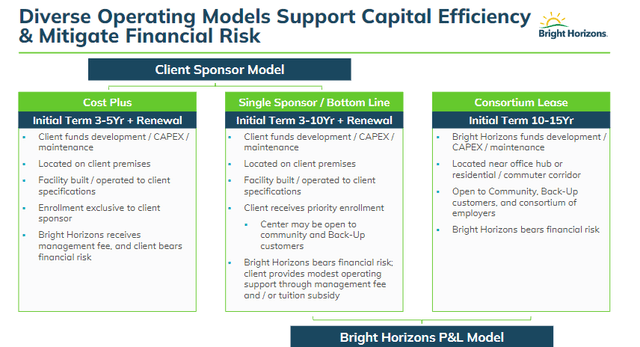

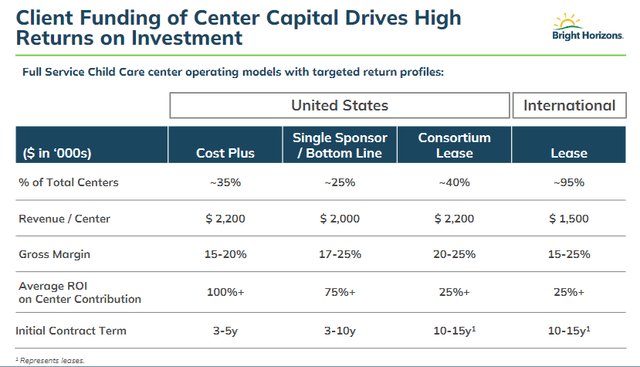

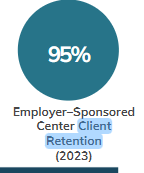

BFAM additionally has an asset-reduced working mannequin that frees up money to fund its M&A technique. Within the US (the vast majority of income), BFAM operates on a client-sponsor mannequin the place the mandatory capital prices of latest facilities are funded by employers. In flip, BFAM will handle the facilities and obtain a corresponding revenue from the service providing. As a result of nature of this partnership, the connection has traditionally been very robust (95% retention fee), which is smart as the middle is constructed with the intention of being managed by BFAM.

BFAM

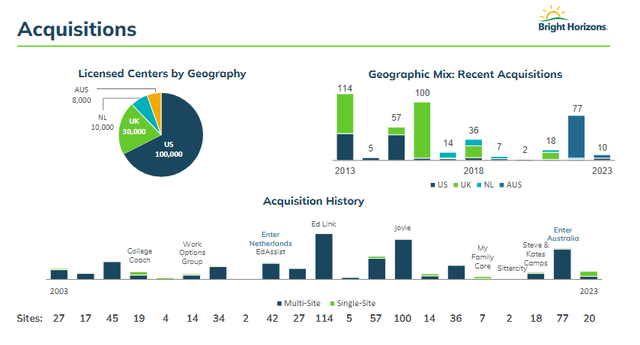

The fantastic thing about this mannequin is that BFAM has low money prices and might convert a good portion of every revenue into free money movement (FCF) that’s used to fund its M&A technique. Since 2009, BFAM has routinely transformed greater than 100% of adjusted internet earnings into FCF, BFAM has been aggressive in its M&A technique, buying a number of hundred facilities over the previous 20 years, and BFAM’s total enterprise mannequin has benefited from the inherent cycle. Asset-light working mannequin: Frees up money to finance M&A; > offers scale > will increase fame > attracts extra prospects > will increase scale > and the cycle repeats.

Evaluation

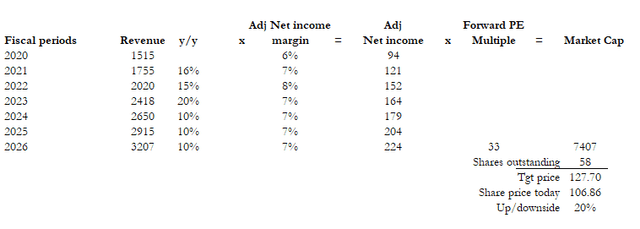

Supply: writer’s calculation Supply: writer’s calculation

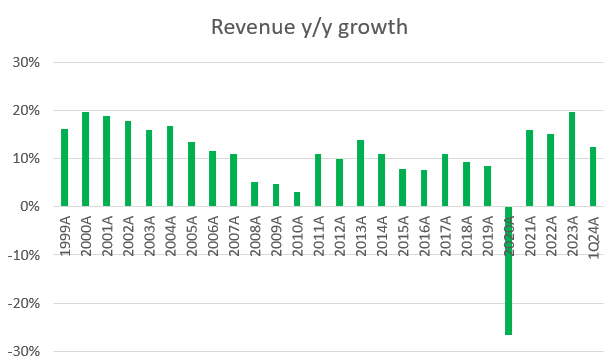

I consider BFAM is price 20% greater than the present share worth. My worth goal relies on FY26 adjusted internet earnings of $224 million and a ahead PE a number of of 33x. Within the post-subprime interval, BFAM has traditionally grown at excessive single-digit to low-teen development charges, and I predict related development over the subsequent 3 years. I consider 10% is well achievable given the secular tailwind and BFAM’s aggressive benefit. Administration additionally plans to extend income by 10% in FY24. In a normalized (pre-COVID) atmosphere, BFAM is working at ~7% adjusted internet earnings margin, and I anticipate that margin degree to proceed going ahead.

One among my essential takeaways from as we speak’s market is that I anticipate BFAM to commerce at 33x ahead PE (BFAM’s historic common) versus the 30x it trades as we speak. In my opinion, the latest strain on multiples is probably going resulting from market issues a couple of macro atmosphere the place many employers are shedding workers and this can imply much less demand for childcare providers within the close to time period. I disagree that it is a short-term macro headwind, however 1Q24 outcomes are already exhibiting indicators of restoration. Full-service middle occupancy averaged >60% in 1Q24, up from 55-60% in 1Q23, with wholesome reserving traits within the US, Netherlands and Australia. Moreover, 44% of full-service facilities are above 70% occupancy, a 900bps enchancment from 35% in 1Q23. Within the US, regardless of the macro headlines, registrations grew by excessive single digits year-on-year, with good efficiency throughout all age teams and central fashions and notable double-digit development amongst infants and toddlers. When it comes to manpower, BFAM has made important progress in growing the staffing degree of the middle by improved recruitment and retention.

As BFAM exhibits the market that it’s able to rising because it has traditionally, the market ought to revalue BFAM again to its normalized (common) a number of of 33x.

Funding threat

BFAM UK’s full-service enterprise, which accounts for round 13% of gross sales, continues to battle resulting from low occupancy attributable to a mixture of an unfavorable macro atmosphere and workers shortages. Moreover, BFAM’s training consulting enterprise continued to overlook expectations, with full-year steerage minimize to low single-digit development from mid-single-digit development. This was primarily attributable to low buyer uptake and worker engagement. Whereas these segments are small individually, they nonetheless make up a major quantity on a collective foundation. If the macro headwinds in these areas worsen, this might scale back development to under 10%.

Conclusion

My constructive angle in direction of BFAM is because of its robust place within the rising childcare providers market. I anticipate BFAM to profit from macro tailwinds and have the ability to seize share given its robust aggressive benefit (scale and fame). BFAM’s asset-light mannequin additionally allows it to transform earnings to FCF extremely, offering capital to fund its M&A technique, additional strengthening its aggressive benefit.