Walter Bibikov

James Knightley and Francesco Pezzole

Why we count on a lower subsequent week

Of the 26 banks surveyed by Bloomberg, 16 have been in favor of a 25 bp fee lower by the Financial institution of Canada. June 5 towards 10 for BoC retains in a single day lending fee at 5%. The same steadiness of possibilities is noticed within the markets, and the likelihood of a fee lower of 25 bp. The proof seems to argue in favor of this transfer, and we consider that given the BoC’s historical past of willingness to make daring calls, we consider it is going to go for a 25bp lower with little quantity. The caveat is that BoC officers haven’t been notably vocal in regards to the prospect of tapering, and so they might as a substitute select this assembly to make a transfer in July. At present, the transfer at this assembly is totally appreciated by the monetary markets.

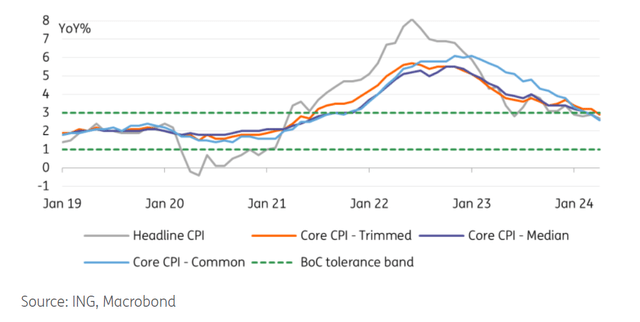

Key to the June fee lower view is that client worth inflation has slowed to 2.7% and core inflation is now additionally beneath 3% year-on-year, that means each inflation measures are inside the BoC’s consolation vary of 1% to three%. The unemployment fee has risen to six.1% from a low of 4.9% in mid-2022, whereas wage progress is within the vary of slightly below 5% y/y. First-quarter GDP is more likely to have risen simply above 2% year-on-year after a weak second half of 2023, however that was primarily resulting from a 0.5% leap in exercise from the earlier month in January, when February a extra subdued 0.2% progress was recorded, and output is anticipated to be flat in March.

Furthermore, the consequences of tight financial coverage have gotten more and more obvious, with the family debt service ratio hitting a file excessive of 15%, in comparison with 9.8% within the US. The danger of rising mortgage defaults could be very actual with rising unemployment, which is able to improve the probability of a possible recession. Notice that on this regard, three consecutive month-to-month declines in retail gross sales will not be an excellent have a look at a time when immigration progress has been so sturdy.

Inflation in Canada is again within the goal vary

The BoC mustn’t sound too dovish about future coverage

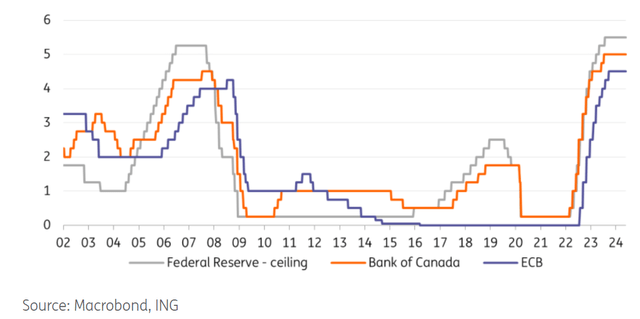

Given this backdrop, we consider the BoC will resolve to chop rates of interest by 25bps, however it’s more likely to be cautious about slicing too rapidly, as this might create the impression of a transparent divergence from the US. In spite of everything, if we’re proper and the BoC does lower 25 bps. on Wednesday, the unfold between the utmost federal funds fee and the BC base fee will widen to 75 bps.

This may be the widest studying since July 2019, and if the BoC cuts charges once more in July earlier than the Fed acts (we count on it to chop charges in September), we’ll see the widest unfold since 2009. This might doubtlessly have implications for the Canadian greenback, so we count on the BoC to return out with comparatively cautious messages on the outlook for additional fee cuts. Nonetheless, with the Fed anticipating to taper from September onwards, we see room for the BoC to chop charges to three.5% within the first half of 2025.

BoC charges versus Fed and ECB

The Canadian greenback is weakening in crosses

In our view, the markets are underestimating each the possibilities of a fee lower in June and additional easing by the tip of the 12 months. Regardless of a faster-than-expected decline in headline and core inflation in Canada, BoC market costs stay closely influenced by Fed expectations: As markets turn out to be much less averse to the Fed, the perceived probability of a BoC lower in June additionally didn’t exceed 70/75% throughout April and Might – now round 65% or 16 bp. The overall worth of BoC cuts on the finish of the 12 months will likely be 52 bps, about 20 bps. greater than for the Fed.

Our view on the BoC has been extra hawkish than the markets for a while and has positioned the Canadian greenback as a laggard within the coming months. Together with ample room for repricing (we count on three extra BoC cuts in 2024), the CAD additionally tends to underperform different commodity currencies when US information surprises to the draw back. If we do see softer US information, the CAD may find yourself nearer to the USD than the remainder of the G10.

By way of commodities, we count on the conjuncture to commerce extra closely towards the NZD, AUD and NOK as markets ought to want to reward these currencies that may depend on hawkish central banks. Relating to USD/CAD, the route of motion ought to nonetheless be primarily decided by the greenback fee, thus the US and Fed information. We count on the primary Fed tapering in September and suspect that the US greenback has already traded at its pre-US election peak. With this in thoughts, a transfer to 1.35 USD/CAD over the summer season stays our base case regardless of BoC easing.

Content material disclaimer

This publication has been ready by ING for informational functions solely, whatever the wealth, monetary scenario or funding goals of the actual person. The data doesn’t represent an funding suggestion, nor does it represent funding, authorized or tax recommendation or a suggestion or solicitation to purchase or promote any monetary instrument. Learn extra

Authentic publish