Monty Rakuzen

Funding thesis

Axcelis Applied sciences (NASDAQ: ACLS) was one of many first corporations I coated on Searching for Alpha. On the time it appeared costly and expectations had been very excessive. Since then, the share value has dropped considerably, and I believed it might be a great time to make sure follow-up.

As you will learn on this evaluation, whereas the corporate’s merchandise stay very important to semiconductor producers, Axcelis has failed to keep up its development momentum. This is because of a number of elements, together with weak demand for shopper electronics and electrical autos, in addition to the corporate’s restricted publicity to AI. There are nonetheless long-term alternatives for greater earnings, however they’ll come later.

This misplaced development momentum, mixed with a restricted margin of security, has prompted me to keep up a Maintain score on the corporate. On this article I’ll briefly evaluate the enterprise description, current developments, prospects close to future and evaluation.

Enterprise description

Whereas I’ve mentioned how the corporate makes cash earlier than in my earlier articles about Axcelis, I’ll briefly talk about it once more. Please discuss with my older articles for a extra detailed description.

Axcelis Applied sciences performs a essential position within the semiconductor business. Semiconductor chips are utilized in quite a lot of digital merchandise from private computer systems and cell telephones to vehicles and sensors. The demand for these merchandise might have numerous elements: some have gotten extra open to shoppers, whereas others are driving the synthetic intelligence growth we’re presently experiencing.

Whereas corporations like Nvidia (NVDA) can design and develop these chips, the precise manufacturing course of is advanced and requires important funding. Because of this pure play semiconductor producers exist. They’re known as foundry. Axcelis provides these producers with ion implantation tools and different processing tools. I will not go into the technical particulars, however this tools helps to alter {the electrical} properties of the semiconductor, which is a essential course of.

It’s a very advanced know-how that requires years of analysis and know-how. That is why there are just a few massive gamers within the discipline, together with Axcelis and Utilized Supplies (AMAT).

Latest developments and inventory efficiency

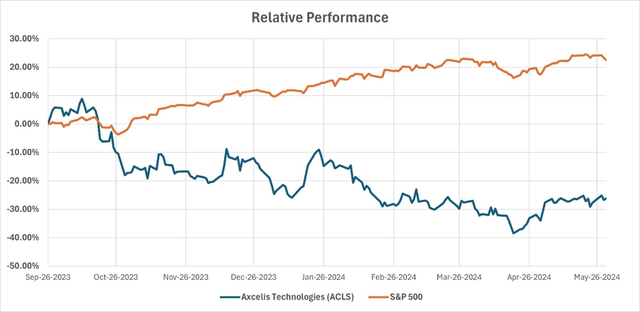

Since my preliminary evaluation right here at Searching for Alpha, the inventory has gone down. It lags the S&P 500 by a major margin, as proven beneath.

S&P Capital IQ

There are a number of causes for this, which we’ll talk about within the outlook part. In abstract, the expansion alternatives didn’t materialize and the corporate remained exterior the AI ecosystem.

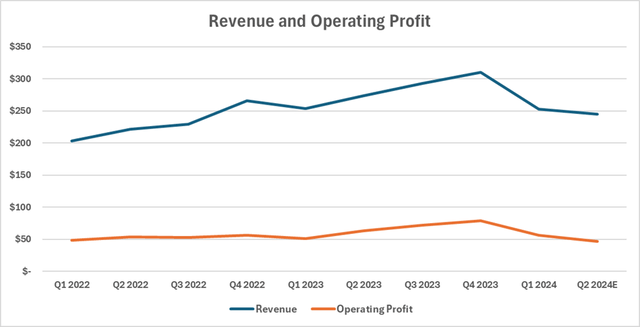

In the newest quarter (Q1), the corporate beat EPS and income estimates. Income was barely down in comparison with the identical interval final yr. Administration plans to decrease income and working revenue within the second quarter in comparison with the identical quarter final yr. Beneath is a chart exhibiting Axcelis’ quarterly precise and anticipated income and working revenue.

S&P Capital IQ

Clearly, the expansion shouldn’t be in step with the market’s expectations from the inventory chart. Income and working revenue had been flat year-over-year within the first quarter and are anticipated to say no within the subsequent quarter. This is likely one of the the reason why shares are falling. Within the subsequent part, we’ll talk about why the corporate is experiencing stagnation.

Forecast for the close to future

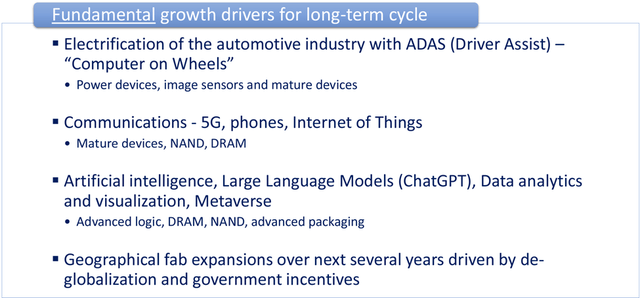

The earnings presentation for Could 2024 reveals the principle basic drivers of development, which you could find beneath.

Presentation for buyers, Could 2024

I consider they are often large revenue drivers for companies. Nevertheless, the important thing phrase right here is long-term. Keep in mind, the additional out the forecasted return, the upper the low cost price utilized (or must be utilized) out there. Whereas I’m assured within the agency’s potential to translate these development drivers into actual earnings, I’m skeptical in regards to the timing.

Let’s break down every of the factors above one after the other.

Electrification is altering all the pieces from home goods to the best way we drive. I perceive the enterprise alternatives with electrical vehicles and different technological advances in vehicles, akin to driver help programs. Nevertheless, I consider that the present state of innovation within the automotive business should even be acknowledged. Know-how pioneer Tesla is shedding market share to its Chinese language rivals, whereas extra conventional gamers are returning to inside combustion engines or hybrids, delaying or canceling their EV initiatives. As well as, auto gross sales stay beneath pre-pandemic ranges and are forecast to say no as shoppers weaken attributable to persistently excessive rates of interest and inflation. Coupled with the regulatory hurdles, it appears to be like like Axcelis has an extended strategy to go earlier than seeing important enhancements on this space.

Communications is an intriguing discipline for funding. The potential of a totally realized Web of Issues is staggering. We’re upgrading our telephones and 5G is turning into increasingly more inexpensive. The US authorities is making an attempt to encourage communications corporations to take a position extra and enhance the nation’s infrastructure. Nevertheless, to this point this has not materialized. Excessive rates of interest deterred these investments. There’s a probability that funding will decide up as soon as the Fed begins slicing charges, but it surely does not appear like it would occur anytime quickly. In accordance with the FedWatch Device, 46.5% of market members consider that in November 2024, charges will lower solely to 500-525 bps.

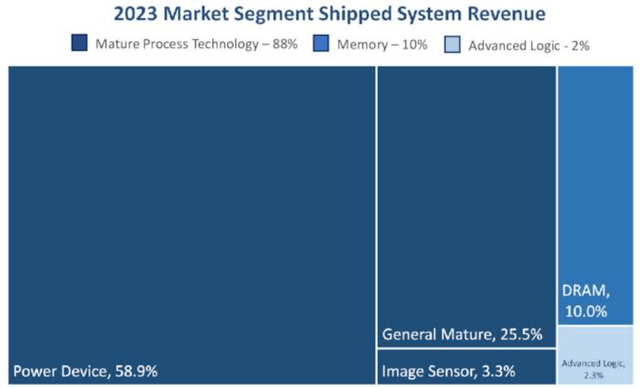

Synthetic intelligence that is undoubtedly the story of 2024. Now we have seen enhancements that we thought had been unattainable. They’re primarily language fashions educated on large information, and so they hold amassing increasingly more information. This implies we’d like extra semiconductor chips to retailer information. My concern is twofold. First, I fear that many of the infrastructure funding for AI has already been made. As soon as enough infrastructure is in place, AI know-how and machine studying fashions will likely be related as a result of the infrastructure will already be in place. Decreased funding in AI infrastructure will imply lowered funding in semiconductor manufacturing capability and thus in Axcelis merchandise. My second concern is that even when this continues to be a high-growth space, Axcelis shouldn’t be very a lot concerned in it. The chart beneath reveals the market segmentation of the corporate’s shipped system income. Reminiscence chips and superior logic account for less than 12% of gross sales. The corporate primarily offers with energy gadgets and common mature merchandise utilized in shopper electronics and autos.

Presentation for buyers, Could 2024

Lastly, it’s true that there are plans to increase the manufacturing facility within the coming years. One such instance is Intel (INTC), which is making an attempt to turn into in foundry of the Western Hemisphere. As they’ll want semiconductor {hardware}, it will imply a rise in demand for Axcelis merchandise. Nevertheless, I stay skeptical in regards to the timing of those extra earnings. It is going to take a very long time for Intel and others to construct working factories and place orders. Intel’s purpose is to turn into the #2 foundry by 2030 alone.

General, I feel the long-term drivers are sturdy. Because of this (mixed with the analysis I will be overlaying) this isn’t a brief thesis. Nevertheless, I consider they’re too long-term and must be lowered accordingly.

Evaluation

Let’s transfer on to the valuation half and see what a good worth appears to be like like for this firm.

My goal value in my authentic quick thesis was $107. Within the following article, I maintained this goal, however closed the quick place, holding the thesis, because the macro atmosphere appeared to enhance. The inventory really fell beneath the value goal and has now recovered barely to $113 as of this writing. The goal value has solely modified barely because the final evaluation.

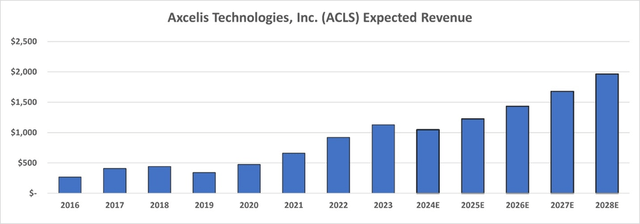

It is a constructive situation the place I predict the corporate will handle to keep up income development post-pandemic, aside from 2024 as administration plans to scale back income. Consequently, income is simply over $1 billion in 2024 and almost $2 billion in 2028. See beneath:

S&P Capital IQ and writer

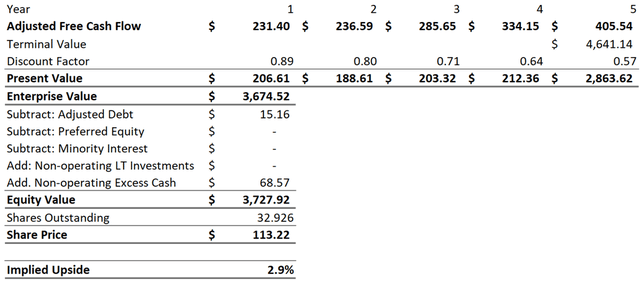

Adjusted for anticipated modifications in margins, capital expenditures and web working capital, this income interprets into adjusted free money movement of $231 million in 2024 and $405 million in 2028.

I remind you that in my calculations I divide money and short-term investments into operational and extra. I take advantage of a sure share of income, often between 5-10%, to calculate working money. That is an approximate calculation of the quantity that will likely be spent on the day-to-day operations of the corporate throughout the yr. The remainder is extra cash. These money surpluses will be claimed by shareholders, however not working money, because the enterprise wants it.

Utilizing these numbers and strategies, we discover an fairness worth of $3.72 billion, implying a $113.22 value goal for the inventory. That is up 2.9% from the present share value on the time of writing and does not present sufficient margin to make it a purchase.

The writer

Conclusion

Axcelis Applied sciences performs a major position in all the semiconductor provide chain. I consider he has strong long-term tailwinds to assist him enhance his topline and bottomline. Nevertheless, the timing of those anticipated positive factors is unsure.

All 4 key long-term development areas highlighted by administration are going through challenges. These issues come up both from excessive rates of interest, which create an unattractive funding atmosphere, or from demand issues for shopper electronics and electrical autos. Additionally, the corporate doesn’t profit considerably from the necessity for extra information attributable to AI developments, because it has little impression on the business.

Whereas the corporate is now less expensive than once I first analyzed it, and the potential upside is constructive, there may be neither a great margin of security nor a compelling short-term catalyst to drive the inventory to the next valuation.

That is why I preserve my Maintain score on Axcelis. I’ll proceed to watch this marketing campaign and can publish one other evaluation if the thesis not holds.