Studio Yaga

Applovin’s advert funding thesis stays strong

Applovin (NASDAQ:NASDAQ: APP) is a SaaS firm that provides promoting software program options for cell and internet app builders to enhance the advertising and marketing and monetization of their apps worldwide.

Dependable restoration within the world promoting market is undisputed, with two market leaders, Google (GOOG) and Meta (PURPOSE), that are already reporting robust progress of their prime and backside strains regardless of an unsure macroeconomic outlook.

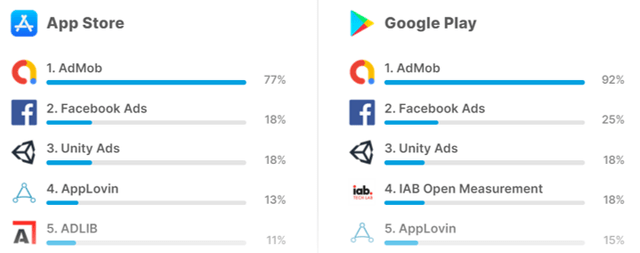

The most well-liked SDKs for promoting and monetization

Figures of purposes

Coupled with the main market share of the preferred promoting and monetization software program growth kits on each iOS and Android platforms, it is no shock that APP additionally reported a double-digit FQ1’24 income of $1.06 billion (+11% QoQ / +47.9% y/y) and GAAP earnings per share of $0.67 (+36.7% q/q/ +6800% y/y).

Many of the higher/decrease tradewind line pushed by acceleration in software program platform progress to US$2.71B in annual income (+17.6% QoQ/+91.2% YoY), with the high-margin SaaS phase persistently reporting progress in Adjusted EBITDA in 72.5% (-0.3 factors q/q/ +10.9 g/y). ).

APP’s AXON 2.0 expertise, launched in early 2023, has clearly benefited its core enterprise with “steady self-learning, incremental information and engineering enhancements” driving “greater return on advert spend (ROAS) for our advertisers, which results in elevated funding” and income progress.

This additionally explains its steady month-to-month energetic payers [MAP] 1.8 million (QoQ/YoY) and common income progress per card [ARPMAP] $48 (+2.1% QoQ/+4.3% YoY).

On the identical time, APP is already directing the gradual enhancements of AXON 2.0 AI fashions together with the excessive demand for promoting in on-line/cell gaming platforms in FQ1’24. integration and elevated spending on UA’.

Mixed with administration’s robust working bills of $329.16 million after discounting non-cash stock-based compensation (+2.1% qoq/+9.9% yoy), it is no shock that the SaaS firm is reporting accelerating progress whole adjusted EBITDA to $549. M (+15.1% q/q/+100% y/y) and an more and more wealthy whole adjusted EBITDA margin of 51.8% (+1.9 factors q/q/+13.6 y/y).

In consequence, it is no shock that APP has supplied a forward-looking Q2 2024 earnings forecast with whole income of $1.07 billion (+1% qoq/+41.3% yoy) and whole adjusted EBITDA of USD 560 million (+2% q/q/ +67.1% YoY), implying a equally wealthy whole adjusted EBITDA margin of 52.3% (+0.6pts QoQ/+7.9 y/y).

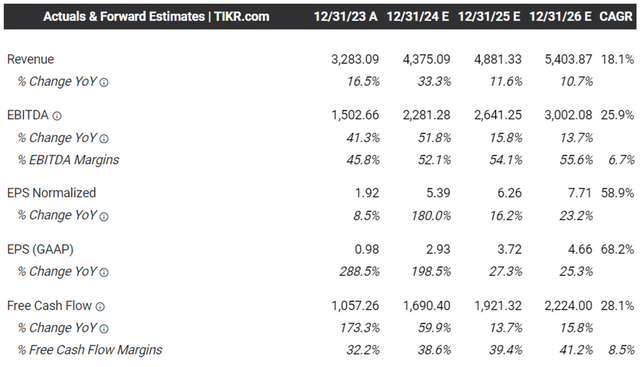

Consensus forecast forecasts

Terminal Tikr

Maybe that is why the consensus raised its forecast estimates, and APP is anticipated to ship accelerated income/earnings progress at a CAGR of +18.1%/+58.9% by FY2026.

This compares to earlier estimates of +10.8%/+31.1% and historic progress of +34.8%/+28.4% between fiscal 2016 and 2023, respectively.

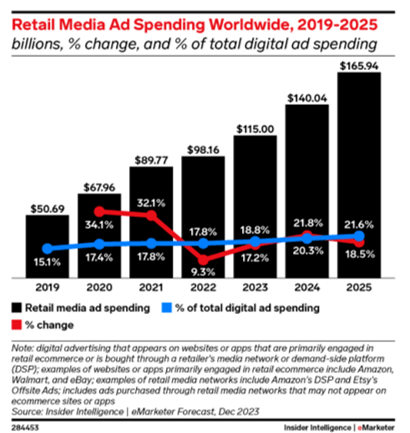

Retail promoting spend

e-marketer

We imagine a lot of the optimism will also be attributed to new progress alternatives for APP within the web-based e-commerce phase, based mostly on projected progress in retail media advert spending from $115 billion in 2023 to $165.94 billion in 2025. which is growing at an accelerated CAGR of +20.1%.

With administration already guiding for the primary launch of “internet adverts on our platform” in Q2 2024, we imagine we will see incremental progress in its prime and backside strains, probably resulting in its subsequent greatest quarter within the 2nd quarter of 2024.

On the identical time, APP’s sturdy free money move of $1.16 billion in comparison with LTM and projected money move enlargement by fiscal 2026 imply it has the flexibility to opportunistically spend money on progress alternatives with out having to pressure its steadiness sheet.

It should additionally allow administration to keep up robust shareholder returns thus far, based mostly on retirements of 24.57m or equal to six.5% of float over the trailing twelve months and 39.71m/10.2% from FY2021, with of this $500 million remains to be accessible by the prevailing share repurchase program.

Coupled with a comparatively wholesome steadiness sheet with a good internet debt of -$3.09B (+17.9% QoQ/ +26.7% YoY) and a well-placed debt maturity of 2028/2030, we imagine that APP stays nicely positioned to achieve the upcoming advert tech growth over the following few years.

So APP inventory is a purchasepromote or maintain?

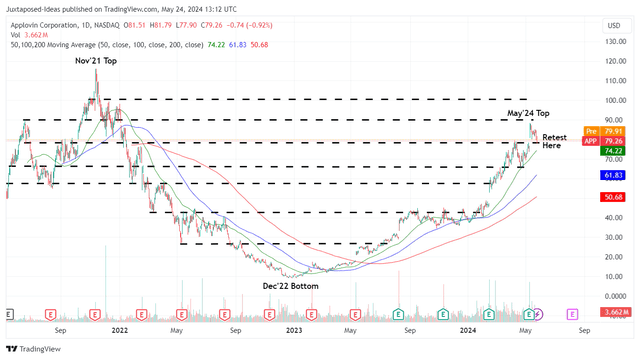

APP 2Y share worth

Commerce view

For now, APP has misplaced a few of its latest features following its wonderful FQ1’24 earnings report, though it’s nonetheless buying and selling nicely above its 50/100/200 day shifting averages.

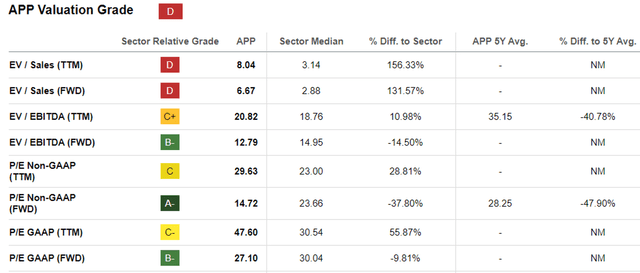

App scores

In quest of Alpha

Regardless of this, we expect APP remains to be moderately valued at a FWD EV/EBITDA of 12.79x and a FWD P/E GAAP of 27.10x.

This compares to advert tech friends resembling extremely worthwhile Commerce Desk ( TTD ) at 44.25x/ 130.31x , Perion Community ( PERI ) at 4.84x/ 12.59x earlier than the latest correction attributable to Bing modifications, and the nonetheless worthwhile Digital Turbine, Inc. (APPS) at 5.96x/NA respectively.

That is particularly so when evaluating the projected APP prime and backside line progress to 2026 with TTD at +21.6%/ +22.9%, PERI at +16.2%/ -30.1% and APPS at -2.8 %/ -22.8% respectively, allowing for that the previous’s accelerated worthwhile progress is absolutely cheaply valued.

Readers also needs to be aware that generative synthetic intelligence has entered the advert tech image, and the ecosystem is anticipated to profit from “quicker content material creation charges, more practical advert campaigns, and higher advert ROI,” naturally driving the accelerated progress of market leaders like PROGRAM .

That is particularly in order the worldwide advert tech market measurement is anticipated to develop exponentially from USD 987.52 billion in 2023 to USD 2.81 trillion in 2030 at a powerful CAGR of +16.1%.

For now, based mostly on FQ1’24 GAAP EPS of $2.68 (+36.7% QoQ/ +6800% YoY) and a FWD P/E GAAP estimate of 27.10x, it’s clear that APP is buying and selling above our truthful worth estimates of $72.60.

Nonetheless, based mostly on consensus estimates for FY2026 GAAP EPS of $4.66, it’s clear that the inventory continues to supply wonderful upside potential of +59.2% to our long-term goal worth of 126, 20 {dollars}.

Coupled with strong returns for shareholders and a sexy threat/reward ratio, we provoke a Purchase score on APP, however with out a particular entry level because it depends upon the investor’s common greenback worth and threat urge for food.

Because the inventory is at present retesting its earlier resistance ranges at $80, readers could need to watch it transfer a bit longer earlier than including after a average pullback to the earlier buying and selling vary of $66-$74 to enhance margin of power.