Enhancing by Sean Williams/iStock by way of Getty Pictures

Funding thesis

At present, Allstate (NYSE: ALL) is on the edge of intensive development. As COVID slows down the worldwide financial system, its elevated influence on the reinsurance market and the ensuing short-term influence on the insurance coverage market have been largely overestimated, leaving an underrated {industry}. On this article, we’ll reveal extra explanation why the insurance coverage {industry} is undervalued, with Allstate being the very best funding on this market due to their promising working base, loyal buyer base, and revolutionary marketing strategy for the subsequent decade.

Firm background/description

Allstate is a United States-based property and casualty insurance coverage firm comprised of a rising community of small firms that present auto, house, life and retirement services and products to clients in the US and Canada. Their popularity is that of a versatile enterprise that is able to adapt to a altering market, incomes them a wide range of improvements and customer support awards. For instance, after Hurricane Katrina in 2005, they applied numerous measures to higher handle and cut back the danger of losses from more and more excessive climate circumstances. This contains including extra danger metrics to the underwriting and pricing of house owners insurance coverage. As well as, Allstate constructed on its robust stability sheet by benefiting from report low rates of interest to situation perpetual most well-liked inventory and subordinated debt to refinance costlier senior debt. On account of these methods, they preserve regular development in property and casualty market share.

Qualitative evaluation

The property and casualty insurance coverage {industry} as a complete is presently rising from the COVID period and the headwinds of that interval are dissipating. Business powerhouses noticed margins shrink and needed to de-risk their insurance coverage portfolios. Now, in 2024, we’re watching income and stability sheets return to regular. After a 12 months of industry-wide premium will increase, the {industry} can now carry out properly. Consensus development estimates are in keeping with our estimate of sustained {industry} development of a minimum of 8% for a minimum of the subsequent decade.

Bargaining energy of patrons:

Over the previous few many years, the digitization of the insurance coverage {industry} has led to an growing reliance on web-based aggregators and social media advertising and marketing, leading to particular person policyholders at this time having increasingly more affect in comparison with large company shoppers who spend hundreds of thousands of {dollars} on premiums. We imagine that at this time’s customers anticipate extra customized consideration and look after the premiums they pay as a result of they’ve on the spot entry to details about protection, pricing and companies. Allstate has prioritized its on-line presence, efficiently and constantly reducing its working prices whereas attracting an more and more loyal buyer base.

Bargaining energy of suppliers:

Within the insurance coverage market, the 2 essential suppliers are distributors and reinsurance companies. Because the {industry} has moved in the direction of on-line platforms, the necessity for insurance coverage brokers and brokers is steadily disappearing, leading to decreased bargaining energy for distributors.

However, the present “tight” reinsurance market attributable to the pandemic continues to place stress on insurers as reinsurers turn out to be much less prepared to tackle danger. Because the underwriting course of takes longer for insurance coverage firms, they expertise greater prices and thus really feel the necessity to cost greater premiums. Though the reinsurance {industry} is anticipated to melt within the close to future, obtainable capital out there is presently nonetheless shrinking. This stress on insurance coverage firms to regulate their insurance policies and enhance costs is best for corporations with loyal buyer bases and decrease working prices, which is completely in keeping with Allstate.

Risk of recent entrants and improvement:

The insurance coverage {industry} is responding to the specter of new entrants by specializing in branding, distribution and technique. The insurance coverage {industry} is altering, from usage-based insurance coverage (UBI) know-how to the Web of Issues (IoT) and drones, from technology-driven underwriting merchandise to new property information sources, and from API-based insurance coverage useful modules to white-label insurance coverage merchandise for quick integration and launch. Corporations should observe the curve to take care of relevance.

Risk of substitute merchandise:

Traditionally, insurers haven’t needed to take care of substitute merchandise. Whereas the Insurtech motion may change that, consultants predict it will not encroach on their marketplace for a minimum of the subsequent 20 years.

Rivalry between current rivals:

The fashionable insurance coverage market as a complete operates as an oligopoly. A number of dominant firms within the property and casualty insurance coverage sector are Allstate, State Farm ( STFGX ), Progressive ( PGR ) and Berkshire Hathaway ( BRK.B ). Every of those corporations controls a minimum of 5% of the market and affords related insurance policies on a big scale. State Farm’s extensively profitable advertising and marketing campaigns and buyer service-oriented enterprise mannequin have helped them seize their largest market share in many years.

Allstate, together with State Farm, preserve regular development in market share. As State Farm’s advertising and marketing campaigns wind down and the success of Allstate’s digitization course of grows, we anticipate Allstate’s market share to outpace State Farm’s within the subsequent few years.

Details of thesis help

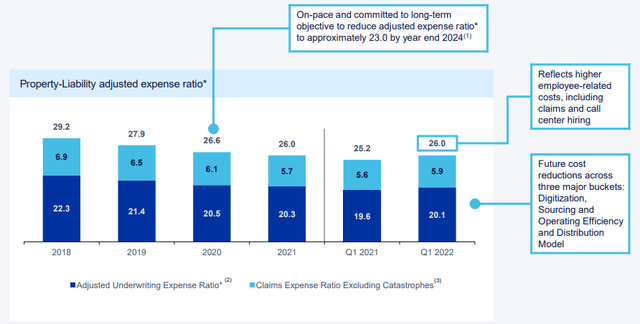

A defining attribute of Allstate is their deal with customer support and constructing loyalty, realized by means of prioritizing the optimization of the insurance coverage coverage course of. Prior to now, they’ve achieved this by working by means of native small companies to construct connections between brokers and shoppers. In response to COVID, they’re implementing their “multi-year transformational development plan.” From 2020, cut back the worth and prices of automobile insurance coverage and put extra emphasis on insurance coverage. This funding in digital infrastructure allowed them to put off 3,800 workers, additional decreasing long-term working prices. Additionally they indicated their intention to proceed to cut back prices by means of: digitization, provisioning and operational effectivity and distribution mannequin, which can result in a steady enhance in EBIT with the purpose of decreasing their debt-to-expense ratio to 0.23.

Allstate Investor Presentation

Whereas they’re selling their product on-line, Allstate nonetheless prioritizes customer support. Throughout this course of, they’ve invested important assets in constructing a complete on-line presence. From their fastidiously designed web site and simply accessible on-line brokers to their intensive social media community, their purpose is to proceed to make the insurance coverage course of as streamlined as doable.

Even ignoring their doubtless future development, many market indicators level to them being presently undervalued, corresponding to their EV/Gross sales, P/E and P/S ratios being properly beneath {industry} averages. As well as, their dividend yield of two.2% dwarfs the {industry} common of 0.3%. Because of the above causes and cautious fee hikes, their revenues for the primary quarter of this 12 months reached $15.3 billion, a rise of 10.7% in comparison with final 12 months. This excellent first quarter end result demonstrates the worth of our thesis and reinforces our conviction.

Evaluative evaluation

Our projected free money stream for the subsequent 5 years is predicated on regular development within the property and casualty insurance coverage market, Allstate’s continued development in market share and decrease prices.

Projected free money stream

QOE Capital

From there, we discovered our WACC utilizing values from their annual monetary stories together with market estimates for his or her beta, which was constantly beneath 0.8.

QOE Capital

Our goal worth is set utilizing a perpetual development technique utilizing a extra sensible a number of of estimated trailing EBITDA. We additionally used the multiples technique, utilizing a conservative estimate for the EBITDA a number of, and created a corresponding sensitivity desk.

QOE Capital

Whereas {industry} multiples over the past two years have been within the vary of 13-15x, when factoring within the anticipated development, we anticipate the multiples to rise to round 16-18x.

QOE Capital

Threat dialogue

As all the time, traders ought to concentrate on a given firm’s underlying idiosyncratic dangers along with their macro volatility. To start with, Allstate’s capacity to pay insurance coverage claims over the long run is conditioned by investments in dangerous property, which enhance the chance of volatility of capital and earnings. This isn’t a secret for anybody, and the corporate can be conscious of this downside. Allstate has a deep deal with using derivatives to get rid of funding danger and cut back volatility. Sadly, this comes at the price of decreasing their total profitability. For the reason that finish of 2022, the company has actively decreased danger in its funding portfolio, primarily by decreasing publicity to equities and speculative fastened earnings devices. Throughout that point, their fairness holdings fell from 7% to three%, and their restricted legal responsibility holdings fell from 13% to 12%.

One other good portion of their danger is said to disaster losses brought on primarily by extreme climate corresponding to hurricanes, wildfires and extreme storms. They noticed a $2.5 billion soar in disaster losses from 2022 to 2023, largely as a result of a rise within the frequency of extreme storms. Whereas it is a legitimate concern going through the insurance coverage {industry} as a complete, Allstate is a bit more insulated from the issue as a result of earlier renewal of reinsurance safety. Over the previous decade, the corporate has confirmed fairly adept at utilizing its reinsurance insurance policies to constantly outperform the {industry} as a complete. Whereas we imagine within the firm’s capacity to proceed to excel in danger administration, we imagine traders ought to concentrate on the inherent volatility of the insurance coverage {industry}.

On a bigger scale, with the 2024 election approaching, there may be the potential for large financial shifts for healthcare suppliers. The Reasonably priced Care Act, a coverage that President Trump has repeatedly talked about repealing, has confirmed to be a boon for insurance coverage firms. If the previous president is elected for a second time period, there’s a risk that the insurance coverage {industry} as a complete may anticipate a decline in income.

Conclusion and conclusions

With the mix of a steadily rising property and casualty insurance coverage market, an revolutionary price discount plan and a loyal buyer base, we suggest that traders take a “purchase” place on Allstate. Bearing in mind the potential dangers, Allstate’s profitable price discount program and plans to lift costs in crucial areas that haven’t traditionally seen important declines within the shopper base counsel income development and free money stream for a minimum of the subsequent 5 years.

As well as, the insurance coverage {industry} as a complete is presently undervalued as a result of strengthening of the reinsurance market in response to the elevated dangers which have arisen on account of the pandemic. Because the market softens within the coming years, income throughout the {industry} will rise as there may be much less stress on the backend for corporations. General, we encourage patrons to look previous this short-term undervaluation, add Allstate to their watch checklist, and even contemplate investing.