by no means

Pa Lin’s track

Weak confidence continued to carry again progress

China has had combined outcomes by way of knowledge releases over the previous month, with most indicators coming in weaker than market expectations.

It grew to become the important thing subject of the month each the personal sector and households stay cautious. Credit score knowledge confirmed combination funding contracted for the primary time since 2005, whereas M2 progress additionally fell to file lows. After a powerful 2023, credit score declined sharply in 2024. We consider that actual rates of interest stay too excessive for the present state of the financial system, and we consider that the chance of financial easing will enhance over the subsequent few months.

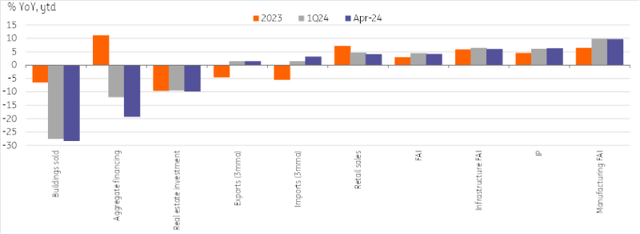

Retail gross sales confirmed that customers additionally remained cautious, falling to a brand new post-pandemic low of two.3% year-on-year. Shoppers are shying away from massive purchases in favor of the “eat, drink and play” classes.

Mounted funding additionally disillusioned for the month, falling to 4.2% y-o-y primarily on account of headwinds from personal sector funding, which rose 0.3% y-o-y. As property costs fell sharply in April and homebuilder sentiment hit new lows, it was no shock to see property funding stay the primary drag -9.8% y/y YTD.

China’s high-tech transition affords good advantages

An excellent substrate will be the transition to high-tech improvement, which continues to stimulate hotbeds of sturdy progress.

One side of this transition will be seen within the resumption of business exercise. Industrial manufacturing rose to six.7% y/y in April, pushed by high-tech (11.3%), computer systems, communications and different digital tools (15.6%) and vehicles (16.3%). Manufacturing PMI knowledge for Could confirmed combined indicators of additional momentum, with the official PMI notably falling to 49.5, whereas the Caixin PMI hit a seven-month excessive of 51.7 – though each surveys confirmed a slowdown in new orders.

Imports additionally beat expectations for the month, reaching 8.4% y/y, as demand for computerized knowledge processing tools, built-in circuits and high-tech imports elevated on account of synthetic intelligence. As China’s financial transformation continues, these areas ought to proceed to see comparatively sturdy progress.

China’s progress has been unbalanced this 12 months

CEIC, ING

Coverage rollout has accelerated amid a stimulus to stabilize progress

The coverage bulletins stole the thunder from China’s Knowledge Dump Day. Policymakers stepped up assist measures to attempt to stabilize the property market, and the central authorities started issuing 1 trillion yuan of ultra-long-term bonds.

New measures previously month have included lifting minimal mortgage charges, lowering down fee ratios, lifting restrictions on purchases and asserting outright dwelling purchases to assist soak up extra stock. Banks proceed to supply assist to sick builders.

Growing aggressiveness in coverage assist has supported markets over the previous month and has proven a continued dedication to stabilizing progress. There may be rising optimism within the markets that we are going to see home costs in tier 1 and a couple of cities backside out within the coming months. Though that is maybe an important improvement in stabilizing home belief, it is usually step one and extra must be achieved. The third plenum in July is probably going to supply extra particulars on the long-term coverage course to additional deepen reforms and promote China’s modernization. President Xi’s feedback indicated that the assembly may embrace measures to assist property, employment and childcare.

Content material disclaimer

This publication has been ready by ING for informational functions solely, whatever the wealth, monetary state of affairs or funding aims of the actual consumer. The data doesn’t represent an funding advice, nor does it represent funding, authorized or tax recommendation or a proposal or solicitation to purchase or promote any monetary instrument. Learn extra

Unique put up