Guido Mith

What a distinction a number of months could make! Again on the finish of September final 12 months, I did the evaluation Dime Neighborhood Bancshares (NASDAQ: DCOM), a financial institution of modest measurement with a market capitalization up to now solely $775.1 million. On the time, I felt the inventory was low cost sufficient to supply buyers good upside potential. In spite of everything, the inventory has actually rallied, leading to a achieve of about 42% from the time I rated the corporate a “purchase” to the tip of December. Since then, nevertheless, the weak point of its monetary place has helped push the inventory decrease. Quick ahead to right this moment, and the inventory is up simply 4.2% whereas the S&P 500 is up 22.3%.

On condition that sort of work, you’d assume I would be right here to reiterate my optimism in regards to the firm. However it’s not so. After Wanting on the newest out there knowledge, I actually assume now’s the time to go decrease. Whereas I’d like to see the inventory go up prefer it has been, the financials have deteriorated and the inventory would not look that engaging in comparison with what it’s. The one exception to that is when shares are low cost. However I’d argue that the standard of the institution makes this cheapness justified. Subsequently, due to this, I’m formally downgrading the corporate from Purchase to Maintain to mirror my view that the inventory is unlikely to outperform the broader market within the foreseeable future.

A have a look at latest weak point

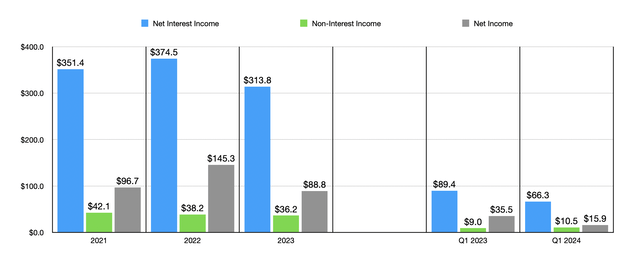

After I beforehand wrote about Dime Neighborhood Bancshares, we solely had knowledge for the second quarter of fiscal 12 months 2023. This knowledge now covers the primary quarter of 2024. Earlier than we get to the newest outcomes, it is perhaps useful to see how 2023 ended. The establishment’s internet curiosity earnings for the 12 months was $313.8 million. That is down from the $374.5 million reported a 12 months earlier. And this although the corporate’s stability sheet has elevated considerably. The massive ache for the establishment will be attributed to the truth that its internet curiosity margin has fallen from 3.25% to 2.46%. However this was not the one weak point of the establishment. Non-interest earnings fell from $38.2 million to $36.2 million. Mixed, this precipitated internet earnings to fall from $145.3 million to $88.8 million.

Posted by SEC EDGAR Information

In the case of fiscal 2024, the weak point has largely persevered. The decline in the price of money, securities and borrowings, in addition to a discount within the firm’s internet curiosity margin, decreased internet curiosity earnings to $66.3 million within the first quarter of this 12 months, in comparison with $89.4 million recorded a 12 months earlier. True, non-interest earnings elevated from 9 to 10.5 million {dollars}. However that wasn’t sufficient to stem a pointy drop in internet earnings from $35.5 million to $15.9 million. Notably, a few of that ache was additionally attributable to larger prices, particularly a rise in salaries and worker advantages from $26.6 million to $32 million, and a rise in Federal Deposit Insurance coverage premiums from $1.9 million to $2. 2 million {dollars}.

Posted by SEC EDGAR Information Posted by SEC EDGAR Information

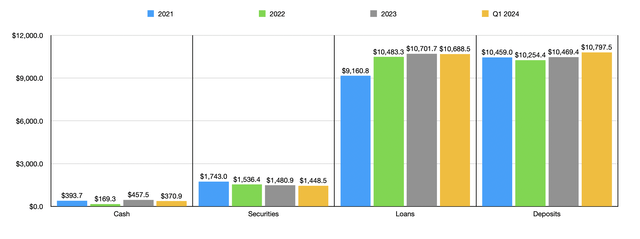

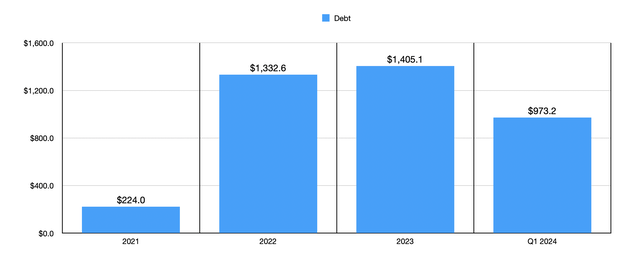

Turning to the stability sheet, the corporate has seen each optimistic and adverse adjustments. For instance, the price of deposits continued to develop. Within the first quarter of 2024, they have been just below $10.80 billion. That was up from the $10.47 billion reported on the finish of 2023. However, the worth of securities fell from $1.48 billion to $1.45 billion, whereas the worth of loans on the corporate’s books decreased from $10.70 billion to $10.69 billion. Even the worth of money and money equivalents decreased from $457.5 million to $370.9 million. That is to not say that each one these falls have been in useless. On the identical time this occurred, the worth of the debt on the corporate’s books fell. On the finish of final 12 months, the debt was 1.41 billion {dollars}. That quantity dropped to $973.2 million on the finish of the primary quarter of this 12 months. Given how excessive rates of interest are, it is a internet optimistic and will have decreased the prices of money, securities and loans.

Posted by SEC EDGAR Information

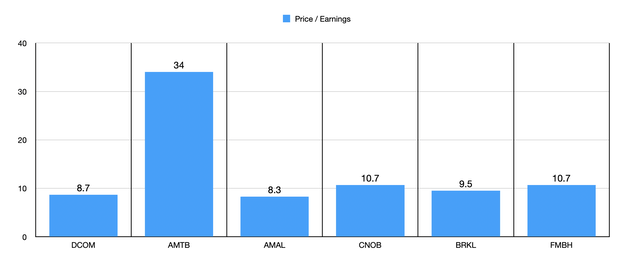

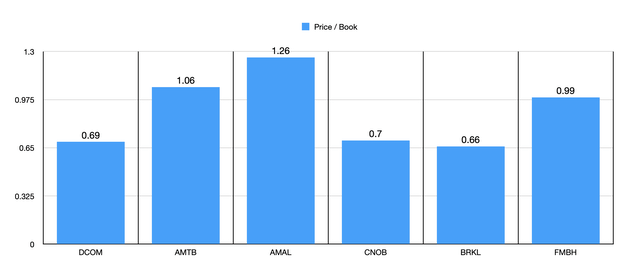

Though I’m usually adverse in regards to the decline in earnings and income, I consider that the autumn in debt and improve in deposits outweighs the autumn in money, securities and loans. However to guage this enterprise, you should have a look at extra than simply this knowledge. We additionally have to see how low cost the inventory is. Within the chart above, for instance, you may see how a inventory’s value will depend on earnings. You can too see the identical for the 5 related firms I selected to match Dime Neighborhood Bancshares. Based mostly on this, just one out of 5 firms turned out to be cheaper than her. I then did the identical utilizing the price-to-booking method as proven within the desk under. With a value to e-book of simply 0.69 Dime Neighborhood Bancshares is just not solely objectively low cost, however cheaper than all however one of many 5 firms I evaluate it to.

Posted by SEC EDGAR Information

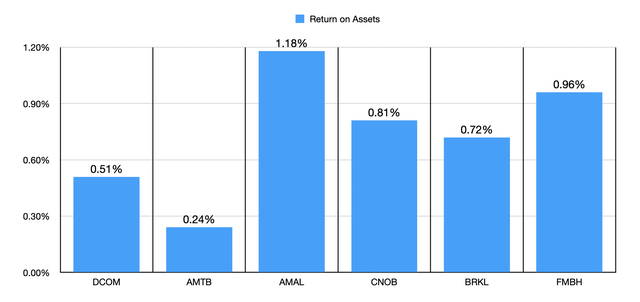

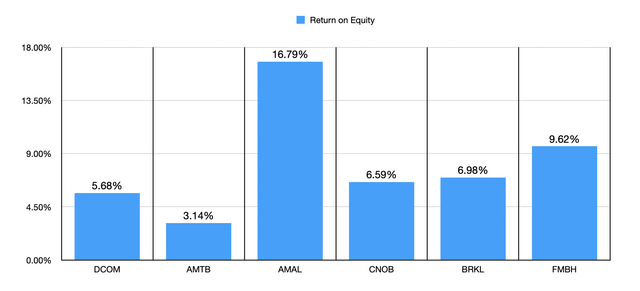

You’ll assume that the mix of rising deposits, declining debt and low buying and selling ratios would make me bullish on the enterprise. Nevertheless, we should additionally take note of the standard of the property in query. We are able to do that in a number of methods. Within the first chart under, you may see the return on property not just for Dime Neighborhood Bancshares, but additionally for a similar 5 firms I’ve already in contrast. On the identical time, 4 out of 5 firms are of upper high quality than it. Within the following chart, I did the identical factor utilizing return on fairness. And once more, I consider 4 out of 5 corporations are larger than that. So, whereas the inventory is affordable, it deserves to be low cost due to the poor asset high quality we’re speaking about.

Posted by SEC EDGAR Information Posted by SEC EDGAR Information

Take it away

For individuals who worth valuation above every part else, I can see why an optimistic view of Dime Neighborhood Bancshares is perhaps the conclusion. Nevertheless, I feel the image is extra difficult. Latest income and revenue points mixed with poor asset high quality are problematic in my e-book. To some extent, this justifies a budget buying and selling of shares. Given these elements, I’d argue that whereas there could also be upside for buyers transferring ahead, there are most likely higher alternatives available in the market. Consequently, I made a decision to downgrade the agency to “maintain”. However within the occasion that we start to see improved income and earnings, will probably be straightforward for me to justify a “purchase” transfer as soon as once more.