Monty Rakuzen

In January of this 12 months, I printed an optimistic article Power switch (NYSE:ET) arguing that its dividend, which on the time yielded ~9%, was in a a lot safer place than a number of years in the past when ET was compelled to chop it. U Within the article, I additionally highlighted a number of dynamics that I consider have created a reasonably favorable setting for ET to ship sturdy total returns. In different phrases, the funding case didn’t simply revolve round dividends, but additionally round natural and M&A development potential.

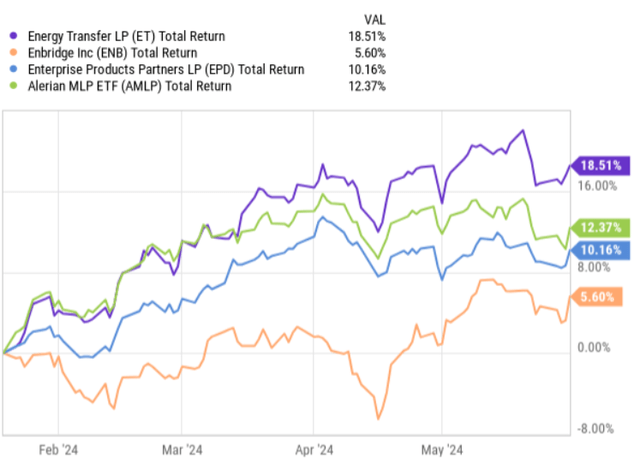

Since publishing this optimum case, ET has outperformed the index and different fashionable midstream names that I’ve additionally assigned purchase scores to.

Ycharts

This example, like after I rerated the case after the This fall 2023 earnings report, may elevate the query of potential overvaluation and whether or not there may be nonetheless respectable upside stays for ET.

Particularly, in April of this 12 months, I analyzed the This fall report back to see if the basics justified the above-average a number of and the share worth development. The mixture of ET’s strengthened steadiness sheet, steadily rising enterprise segments and early indicators of a extra formidable M&A program motivates me to stay bullish on ET. Since then (April 14, 2024), ET has continued to supply alpha as a substitute of the MLP index.

Let’s now contextualize the newest knowledge from the Q1 2024 earnings report with the present bullish thesis to find out the present attractiveness of ET.

Nevertheless, earlier than I analyze the dynamics of the primary quarter, I want to emphasize that my funding technique will not be based mostly on hypothesis or short-term earnings. As an alternative, I am targeted totally on incomes engaging dividends which are backed by stable fundamentals, after which solely the capital appreciation element comes into play.

Assessment of thesis

All in all, trying on the key efficiency indicators for the primary quarter of 2024, it shouldn’t be stunning that ET’s share worth has risen on this approach. All ET enterprise segments skilled development relative to the primary quarter of 2023 and even the earlier quarter. In comparison with the primary quarter of 2023, internet earnings and adjusted EBITDA for the primary quarter of 2024 elevated by 11% and 13%, respectively, pushed by larger volumes and higher pricing.

Apparently, this ET additionally registered report volumes within the crude oil pipeline phase, which is certainly one of ET’s most worthwhile segments (ie the place the money conversion ratio is highest). In consequence, DCF within the first quarter of 2024, which displays the precise stage of money receipts, was $2.4 billion, in comparison with $2 billion within the first quarter of final 12 months. That, in flip, has allowed ET to maintain about $1.3 billion in money on its books after its quarterly dividend, yielding an annualized charge of 8.1%.

As we take into consideration the long run, it is vital to begin with the truth that at the moment round 90% of ET’s Adjusted EBITDA is made up of fee-based segments, which signifies that solely ~10% is uncovered to commodity market volatility (ie internet market danger). Provided that the fee-based segments are linked to periodic (annual) escalators and are inherently much less risky, this supplies the mandatory stability for ET to maintain the dividend protected and higher handle the leverage profile.

Extra lately, ET introduced that it might enterprise to accumulate WTG Midstream, paying about $3.2 billion in money. The brand new acquisition needs to be accretive to underlying DCF, including $0.04 per share as early as 2025, with a forecast (submit synergies) of $0.07 per share in DCF by 2027.

The transfer comes hand-in-hand with what Chief Govt Officer Tom Lengthy stated in a latest earnings name:

Yeah, hear, that is clearly a really, very, superb query. We spend a number of time at Power Switch creating technique right here. I believe I will begin by saying that we nonetheless really feel that consolidation is smart within the midstream area. So, simply to reply your query at 50,000 toes, we nonetheless intend to judge totally different prospects as we glance. So we’re not going to decelerate on that entrance. Now, so far as what we have a look at, it is all the time going to attempt to have a look at the issues that feed all the way in which downstream. We all the time like to speak about how we go from the wellhead to the water, and we try this in all merchandise. So you may see our technique as we have a look at these items and what property we have a look at, how they help the complete worth chain as we make these acquisitions.

In different phrases, it is clear that ET has stepped up its M&A recreation to reap the benefits of a slightly fragmented market. There’s additionally the good thing about inorganic development within the type of incremental diversification and particularly DCF era, as we will for instance see when trying on the particulars of the WTG Midstream acquisition.

Given all this, one can query ET’s capacity to take care of steadiness sheet safety. This might certainly grow to be an issue if ET continues to announce such vital money transactions. Nevertheless, given the present knowledge, I simply do not see any danger on the steadiness sheet finish.

First, as famous above, ET can maintain about $1.3 billion in money every quarter — and that is after debt service and dividend distributions.

Second, capital upkeep prices are fairly low relative to quarterly money holdings. For instance, in Q1 2024, ET spent roughly $460 million on natural capital for development, which nonetheless leaves sufficient liquidity to focus on M&A

Third, ET took some notable steps to scale back its most popular inventory place by shopping for again all of its Collection E most popular models. Through the quarter, ET additionally purchased again $1.7 billion of senior notes utilizing a partly money and partly credit score revolver.

Fourth, together with the primary quarter outcomes, administration raised its steering for adjusted EBITDA to $15 billion to $15.3 billion, in comparison with the earlier forecast of $14.5 billion to $14.8 billion. This may enable ET to entry much more liquidity every quarter to finance acquisitions or additional optimize the steadiness sheet.

Now, whereas I said earlier within the article that my ET bias will not be based mostly on short-term outcomes or ET’s capacity to fulfill consensus expectations (and the main focus is on a pretty and steadily rising dividend), I consider that ET will be capable of ship on revised EBITDA era. The principle driver of the rise in EBITDA is the mixing (or consolidation) of NuStar’s property, which closed in Might of this 12 months. This impact alone contributes $500 million to EBITDA development, and the remainder may simply be lined by additional acquisitions and continued excessive demand for oil and pure gasoline.

Lastly, one may theoretically argue that the ET multiplicity has elevated an excessive amount of and has now reached fairly a excessive stage. Whereas an EV/EBITDA of seven.8x could be thought-about larger than the typical over the previous 24 months when in comparison with a few of its most direct friends corresponding to Enbridge (NYSE:ENB)(TSX:ENB:CA), Enterprise Merchandise Companions (NYSE: EPD ) or Plains All American Pipeline (NASDAQ: PAA ), we acknowledge that in actuality ET continues to be undervalued. For instance, EV/EBITDA for ENB, EPD and PAA are 11.3x, 9.3x and 9.2x. Given ET’s development momentum, backed by an investment-grade steadiness sheet, the inventory is reasonable for my part.

Backside line

In my opinion, the latest enhance in ET share doesn’t imply that the expansion has been exhausted. The rise in share worth was pushed by good enterprise fundamentals and an bettering development outlook, the place early indicators of this have been already seen in my earlier (April this 12 months) ET article.

Since updating my thesis, ET has begun to take tangible steps to implement its M&A method to reap the benefits of the fragmented midstream market, the place gradual consolidation ought to enable ET to be extra diversified and keep DCF development momentum.

Given the mixture of stronger EBITDA development, ramping up acquisitions, low upkeep capex and enough quarterly money retention (~8% after dividend service), ET’s monetary danger stays nicely managed.

On account of the aforementioned dynamics, an bettering development profile and a pretty dividend that’s nicely lined, Power Switch stays a superb purchase for me.