Hiroshi Watanabe

The Nuveen Churchill Direct Lending Company (NYSE: NCDL) is without doubt one of the BDCs that took benefit of the prevailing tailwind and went public this yr (late January). Whereas NCDL’s internet asset base is kind of giant in comparison with Morgan Stanley Direct BDC Mortgage (MSDL), which is one other BDC that has had an IPO this yr, is about 2 occasions smaller in complete.

In April, I wrote an article about MSDL, evaluating the basics to see in the event that they had been engaging sufficient to go lengthy and make up for the dearth of a public firm status. The conclusion was optimistic, and since then MSDL has clearly outperformed the BDC index.

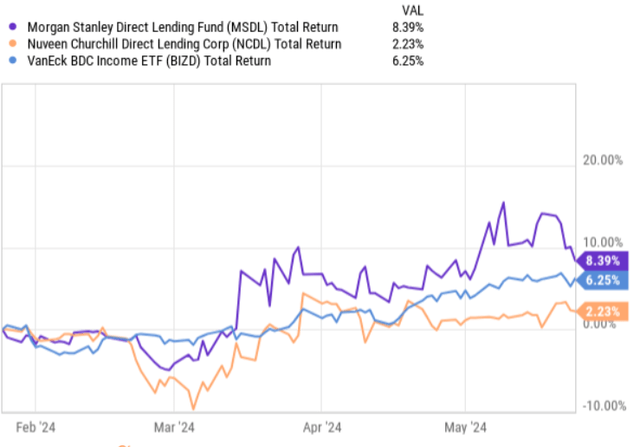

Nevertheless, if we have a look at the chart beneath and examine the entire return efficiency of NCDL to MSDL and the BDC index, we are able to see that there’s fairly a major hole or adverse alpha, which is related to NCDL.

YCharts

With this context in thoughts, let’s dig into NCDL’s fundamentals to see if the mix of current underperformance and financials warrants an extended maintain.

Graduate work

NCDL’s focus is totally on senior secured debt investments for US center market non-public fairness corporations. That is in step with the funding technique of most BDCs.

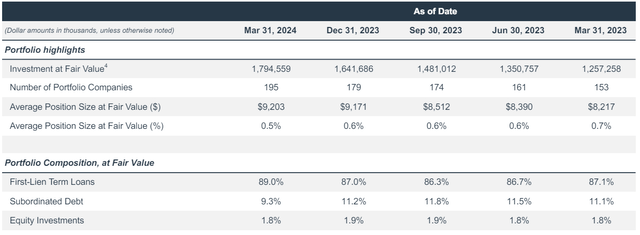

As we are able to see within the desk beneath, the entire worth of NCDL’s portfolio is round $1.8 billion, with investments unfold throughout 195 totally different corporations, offering an honest aspect of diversification. For instance, the typical place measurement as of Q1 2024 was 0.5% of portfolio worth, which is usually related to pretty giant BDCs.

It must also be emphasised that NCDL focuses on first lien constructions, which at present account for 89% of the entire, with the rest primarily positioned in second lien or subordinated investments (and a minor allocation additionally directed in the direction of fairness investments).

NCDL Q1 2024 Earnings Presentation Presentation

The combo of senior lien, subordinated debt and fairness investments is inside the norm of what we would usually see within the BDC house, dominated by first lien and extra tactical allocations made in riskier (increased yield) segments.

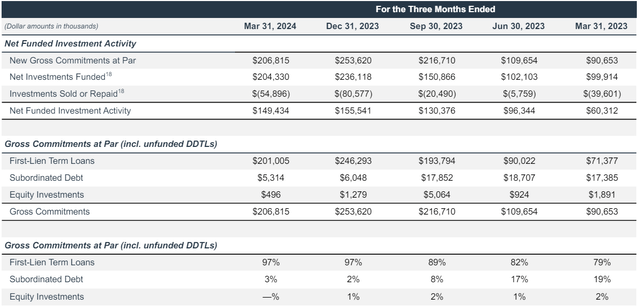

Nevertheless, because the desk beneath exhibits, administration has clearly centered on growing the primary collateral part to de-risk its portfolio. For instance, over the previous two quarters, a lot of the investments had been made within the first stage of collateral – about 97% of the entire internet financing exercise.

An extra takeaway we may notice right here is that NCDL has managed to take care of its current internet funding funding ranges at a optimistic stage regardless of difficult situations within the capital markets and LBO house. Over the previous few quarters, increasingly more BDCs have been experiencing adverse internet funding funding ranges resulting from an incapability to lift ample volumes to offset natural funding repayments. Such dynamics, by definition, create obstacles to sustaining a secure internet funding earnings.

NCDL Q1 2024 Earnings Presentation Presentation

Nevertheless, trying just a little deeper, we are able to discover some indicators that aren’t very encouraging by way of NCDL’s development prospects and general income predictability.

There are two particular points.

First, NCDL is at present experiencing important unfold compression, the place the portfolio’s annualized return has declined for 4 consecutive quarters. A few of this is because of a normal drop within the returns BDCs can cost from funding corporations (resulting from elevated competitors), and a few is because of NCDL’s growing concentrate on first lien merchandise. For instance, the ahead unfold that NCDL captured on 1Q2024 funding was 4.9%, ~150 foundation factors decrease than what it was capable of seize in early 2023.

with

NCDL Q1 2024 Earnings Presentation Presentation

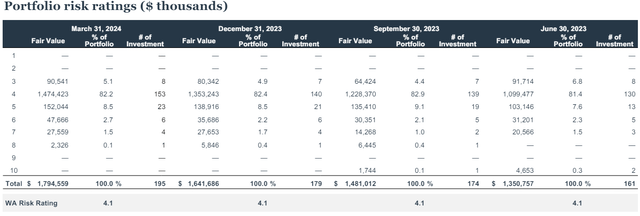

Second, the present high quality of the portfolio isn’t that prime. At present, NCDL’s portfolio-level risk-weighted common is 4.1x, which defines the funding as performing in step with expectations. Nevertheless, there’s a comparatively giant portion of investments which can be beneath the “ranking 4” class, which already signifies that these specific investments or loans are usually not performing properly and have an elevated stage of danger.

NCDL Q1 2024 Earnings Presentation Presentation

Now about $140 million is concentrated within the “ranking 5” class, the place the administration has already despatched a notification to the board about taking particular measures to stabilize monetary indicators.

General, the image isn’t as rosy and strong because the underlying fundamentals would possibly counsel. The mix of fabric unfold compression and poor portfolio high quality creates far an excessive amount of danger and hypothesis round NCDL’s future development prospects than the general means to accommodate present dividends.

Backside line

In my view, there’s not sufficient robust proof to justify opening an extended place in Nuveen Churchill Direct Lending Company.

On the face of it, the basics look strong as there’s first rate diversification and an acceptable emphasis on protected first lien constructions by way of companies which can be already producing money.

Nevertheless, the issue is that NCDL seems to be experiencing structural momentum in unfold compression, making it tough for it to take care of its present stage of internet funding earnings. Along with this, there are heightened dangers to the standard of the NCDL portfolio, which may flip adverse (and intensify) in a state of affairs the place we see some financial weak spot.

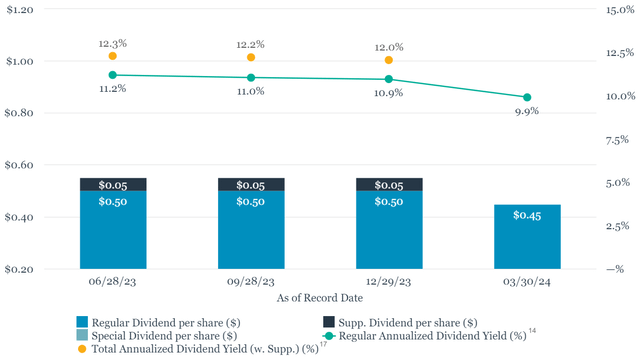

Provided that NCDL gives a dividend yield of ~11.2% (which is barely beneath the sector common), given the above context, I simply do not see the rationale for going lengthy NCDL.