Shahid Jamil

Holding “Soar” (NASDAQ: JAMF) is an organization that develops options for managing Apple units corresponding to Mac, iPad, iPhone and Apple TV in work or workplace settings.

Efficiency of shares has been disappointing all alongside. JAMF went public in 2020 at $39.7, however after after reaching an all-time excessive of $47 and buying and selling sideways within the following years, the inventory value continued to say no. Many of the underperformance has occurred over the previous 5 years, with JAMF down greater than -59%. As we speak, the inventory is at the moment buying and selling at $16.3, down -6% year-to-date.

I fee the inventory a purchase. My annual value goal of $18 per share suggests upside of about 11%. At this degree, JAMF represents an honest shopping for alternative. In my view, the latest launch of a security-enhancing characteristic for Apple Imaginative and prescient Professional may very well be a possible catalyst. Furthermore, JAMF must also profit from the rising demand for enchancment safety of related Apple units within the office.

Monetary opinions

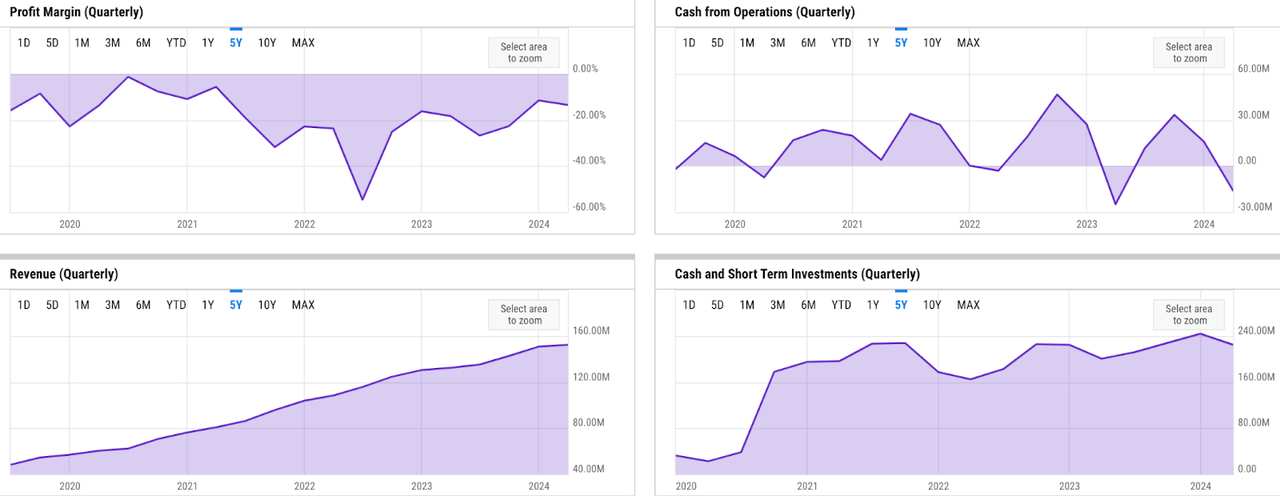

ycharts

The basics had been combined. Income progress has just lately fallen from over 30% to fifteen% y/y. JAMF posted income of $152 million within the first quarter, up 15% year-over-year. Equally, working money move (OCF) era has additionally declined from 2022 onwards. Particularly, this was attributable to the numerous burning of OCF within the 1st quarter of this 12 months, in addition to the identical time final 12 months. Within the first quarter, the principle issue behind the OCF burn was excessive prices for system transformation and restructuring. This had a slight unfavorable affect on liquidity. JAMF ended the primary quarter with $224.5 million in money and short-term investments, down barely from the earlier quarter. Nonetheless, comparatively excessive SBCs (stock-based compensations) additionally resulted in a GAAP loss for JAMF. Within the first quarter, this doesn’t appear to have improved but. In truth, the online loss margin really widened to -13.5%, indicating that JAMF remains to be a bit away from GAAP break-even.

Catalyst

I consider there are a number of catalysts for JAMF in FY24 and past. Some characteristic launches for Apple Imaginative and prescient Professional are noteworthy, in addition to continued growth alternatives as a result of rising demand from enterprises to safe related work units.

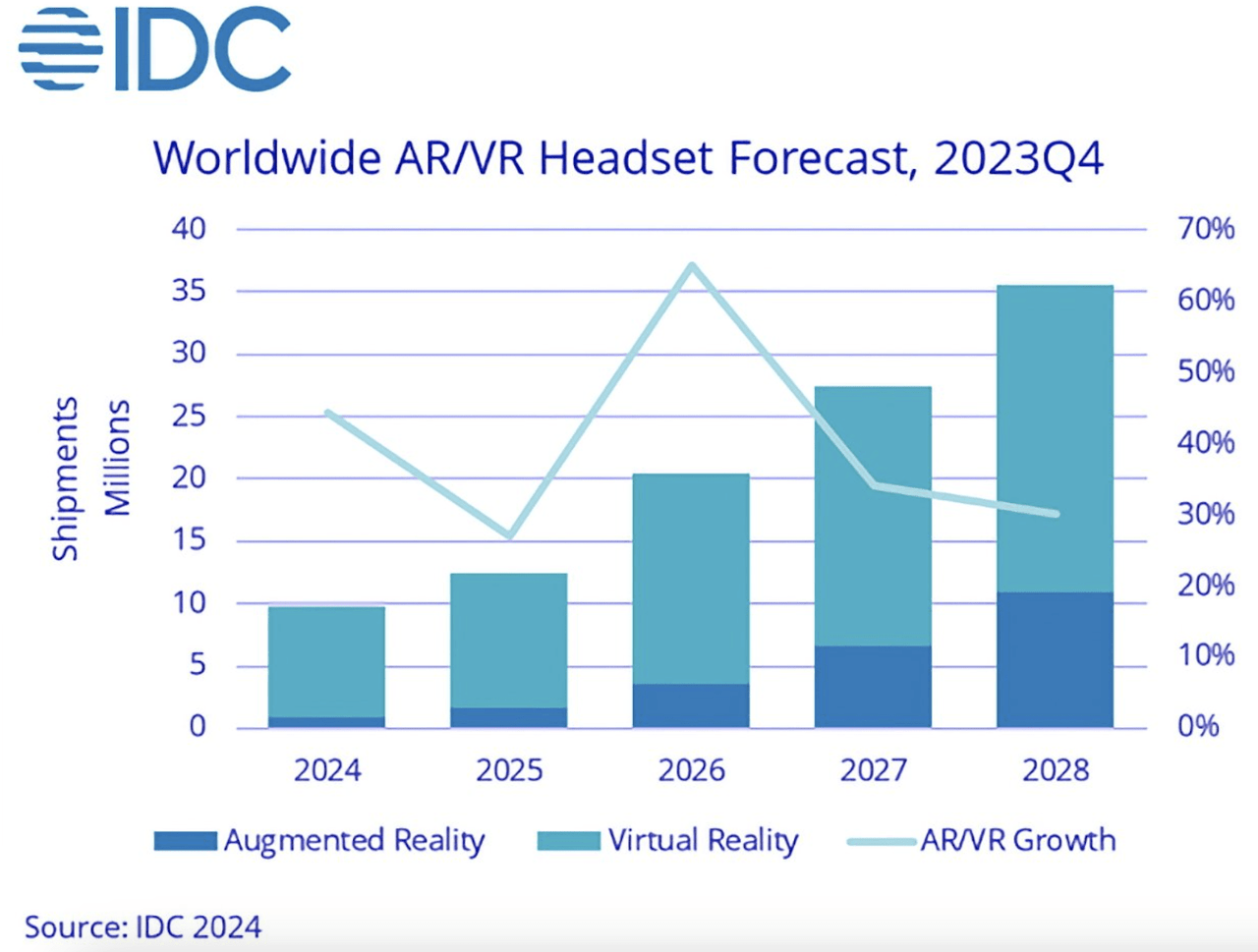

IDC

As an organization that develops Apple-centric choices, JAMF ought to proceed to profit from the elevated penetration of AR/VR headsets such because the Apple Imaginative and prescient Professional. Provided that the market is at an early stage at the moment and remains to be rising at 30% YoY in 2028, there’s a important alternative to seize the house. Furthermore, given the comparatively excessive value of the Imaginative and prescient Professional, I count on the extent of utility for work use to be larger than for private use within the close to time period.

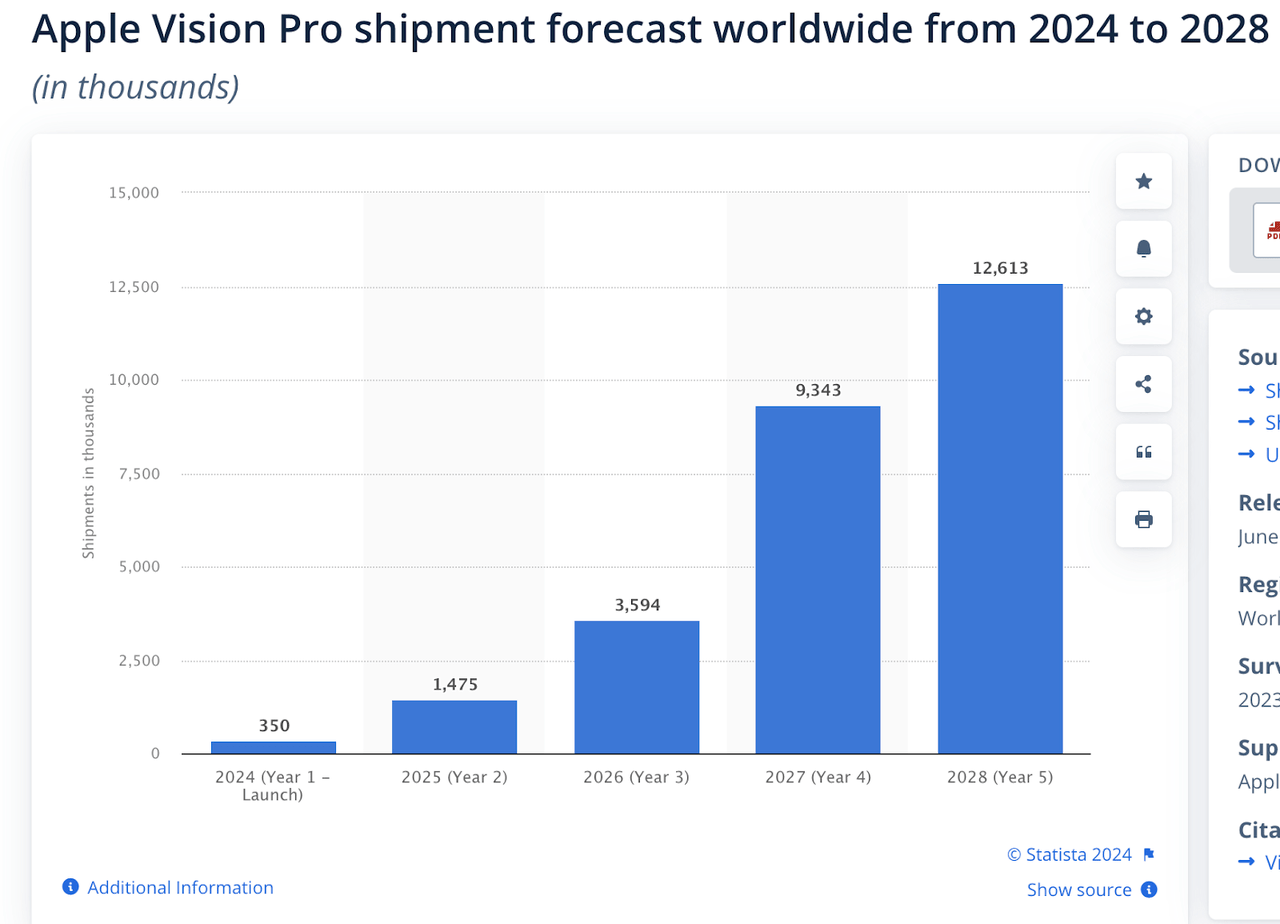

statesman

Extra importantly, with greater than 1.4 million items anticipated to ship in 2025, Apple’s Imaginative and prescient Professional will doubtless stay the second-largest participant behind the Meta within the AR/VR house at the moment. In my view, the elevated use of Imaginative and prescient Professional within the office ought to proceed to extend cyber safety and threats of unauthorized entry, additional driving the demand for JAMF’s choices. In Q1, JAMF appears to have anticipated this by launching related options for Imaginative and prescient Professional, which I consider ought to place it properly to fulfill rising enterprise demand:

With Jamf Professional, organizations can register and optimize the deployment of enterprise purposes and settings for Apple Imaginative and prescient Professional. Jamf Join allows Apple Imaginative and prescient Professional to securely entry company sources for any internet and proprietary purposes that require safe identity-based entry management. Jamf Shield extends the identical use circumstances of cell menace safety, community safety and content material filtering to the Apple Imaginative and prescient Professional.

Supply: Q1 earnings report.

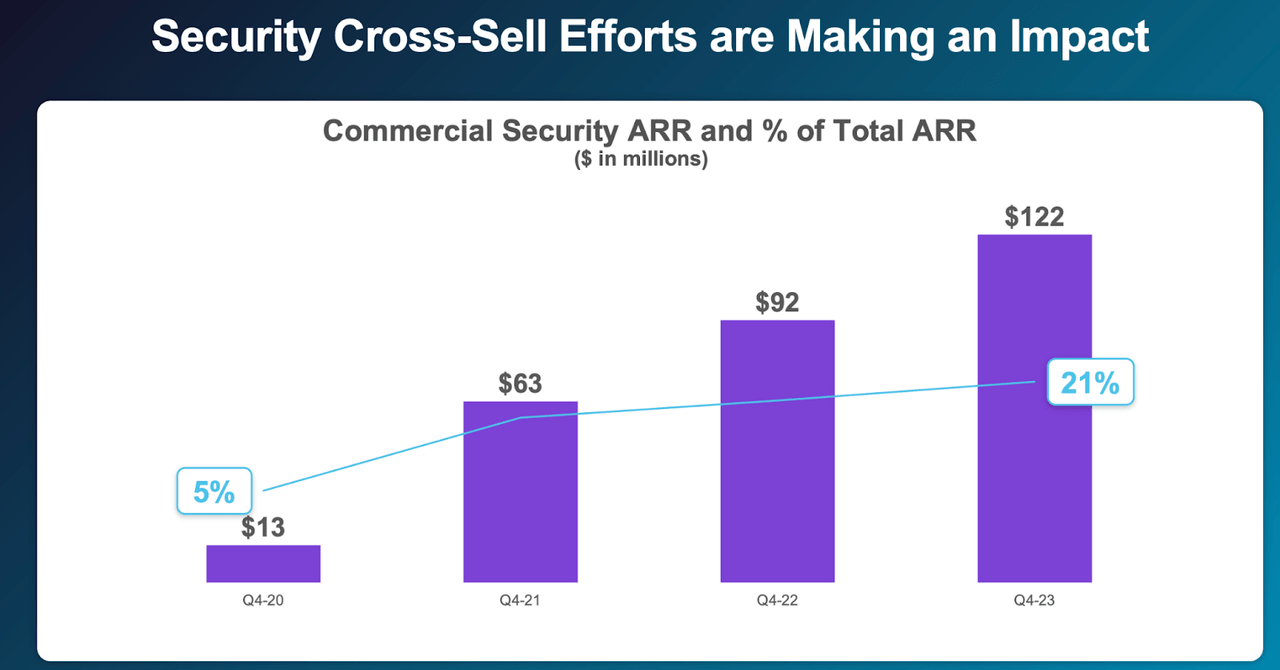

firm presentation

The concentrate on safety has paid off handsomely for JAMF to date, with industrial safety product ARR accounting for 21% of whole enterprise ARR. For my part, this could proceed to create important alternatives for additional progress in subscription income by increasing the set up base, which might additionally result in elevated margins via decrease value per buyer acquisition.

danger

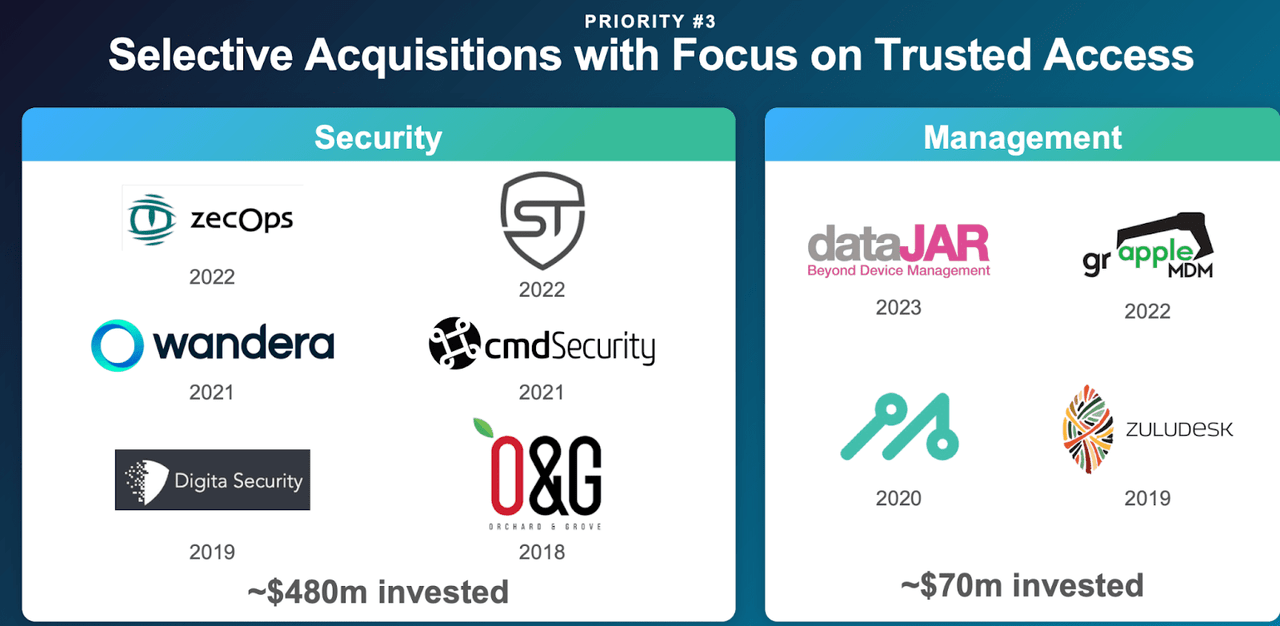

Whereas the short-term structural danger stays minimal, I’d be aware that JAMF’s continued concentrate on aggressively pursuing inorganic progress alternatives from M&A may current a small danger.

firm presentation

To date since 2018, JAMF has accomplished $550 million value of mergers and acquisitions, with the variety of acquired firms persevering with to develop over time as JAMF is ready to generate extra OCF. Extra just lately, mergers and acquisitions have targeted on strengthening safety capabilities, which seems to be a step in the suitable path. Alternatively, there are a number of danger elements to contemplate.

First, cyber safety is a scorching sector the place firms can commerce at the next premium. Second, there may be all the time integration danger the place, for instance, JAMF might spend extra sources than it expects to efficiently combine its choices with goal options after which carry them to market.

10Q

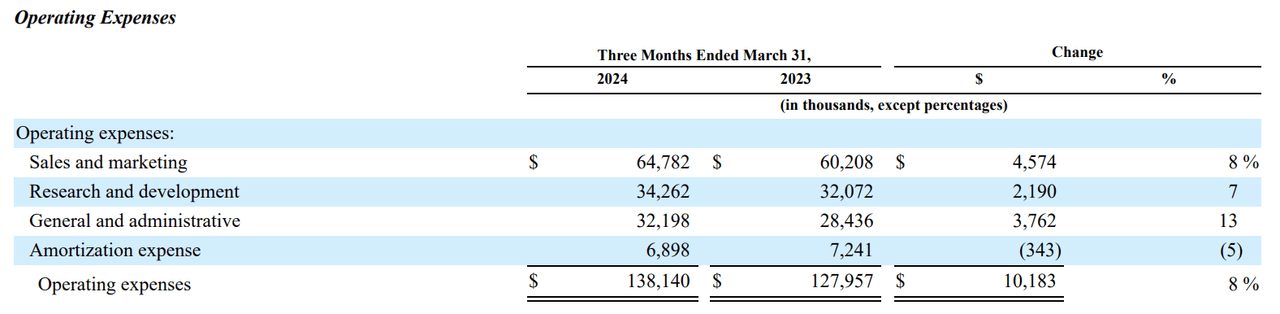

Ultimately, they’ll all come all the way down to a decrease stress. JAMF was not worthwhile on a GAAP foundation, as I discussed earlier, and in Q1, SBC remained fairly robust regardless of a slight decline. However the greatest driver of working bills was a 13% improve in G&A, which was negatively impacted by what seems to be M&A associated, in accordance with Q10:

For the three months ended March 31, 2024, normal and administrative bills elevated primarily on account of a $1.5 million improve in stock-based compensation expense and associated payroll taxes, a $1.4 million improve in , an acquisition-related improve of $1.3 million, system-related transformation prices and restructuring prices of $0.8 million,

Supply: 10Q.

Analysis / pricing

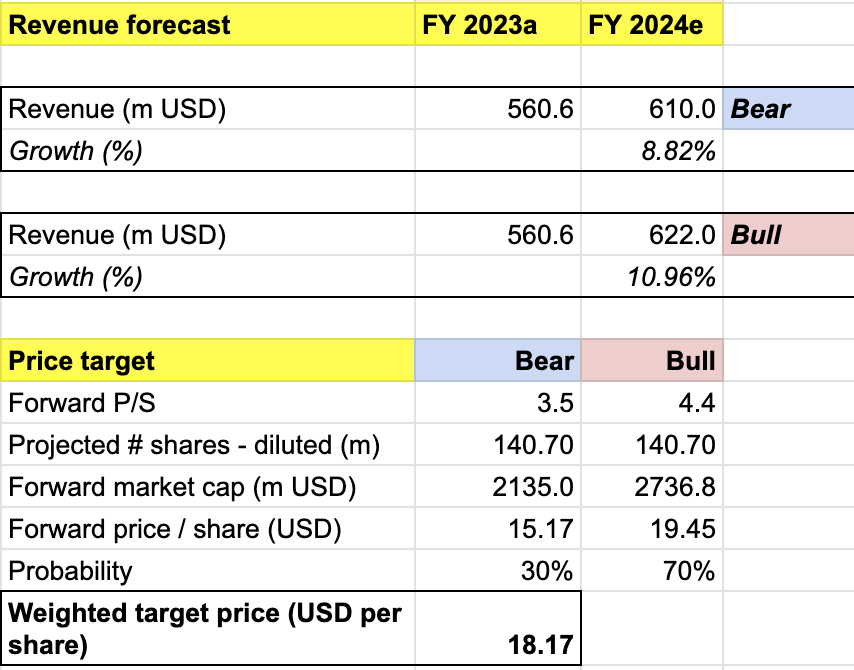

My goal value for JAMF relies on the next assumptions for bull vs. bear eventualities in FY2024 forecast:

Development Situation Assumptions (70% likelihood) – I count on income to develop 10.96% YoY to $622M according to the corporate’s steerage. I predict the ahead P/S will improve to 4.4x, which implies the inventory value will rise to the $20 degree. My guess is that JAMF’s P/S will attain its YTD excessive as soon as it will probably meet its FY2024 goal as promised.

Bearish situation (30% likelihood): JAMF’s FY2024 income can be $610 million, up 8.8% 12 months over 12 months, $8 million under the corporate’s low-end steerage. This could appropriate to $15.2 per share.

personal evaluation

By combining the entire info above into my mannequin, I’ve a weighted FY2024 value goal of $18.2 per share, with a projected 1-year upside potential of roughly 11%. I’d fee the inventory as a purchase.

My 70-30 bear likelihood task relies on my perception that the expansion catalyst ought to stay robust in fiscal 2024, offering JAMF with enough fiscal 12 months earnings visibility. That is additionally partly demonstrated by the slim vary of the corporate’s focus. Alternatively, I additionally lowered my income forecast by $8 million, which was a conservative estimate.

Conclusion

JAMF is an organization that gives options for the administration and safety of Apple units. It ought to proceed to profit from the rising adoption of Apple’s choices in office settings, such because the Apple Imaginative and prescient Professional. As such, the most recent product enhancement to assist allow using Imaginative and prescient Professional at work might probably be a powerful catalyst for JAMF. In the meantime, JAMF’s M&A spotlight may proceed to place stress on GAAP earnings if not executed correctly. As we speak, JAMF continues to be a stable enterprise that generates constant OCF regardless of its GAAP loss. My value goal of $18 per share implies upside of 11%. I fee the inventory as a purchase.