Arnold Media/DigitalVision through Getty Photographs

Introduction

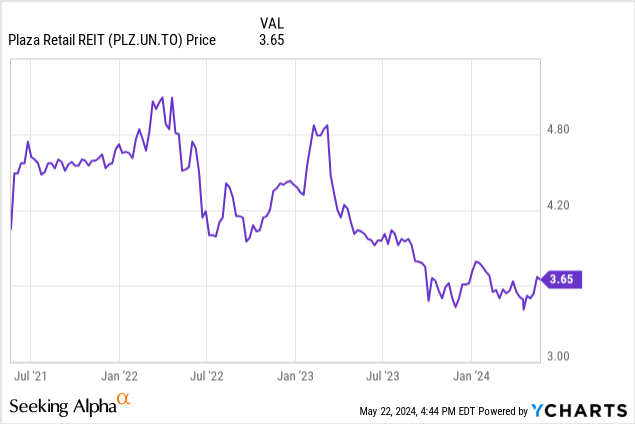

I believe there’s lots of good worth to be discovered within the Canadian REIT sector, so I am conserving an in depth eye on a number of Canadian retail, residential and industrial REITs. I used to personal Plaza Convertible Bonds Retail REIT (TSX:PLZ.UN:CA) (OTC: PAZRF), however luckily/sadly, the REIT repaid the debt obligations on the maturity date. Clearly, I am glad the REIT survived the COVID pandemic, however I additionally do not thoughts getting an honest coupon from a well-run REIT. However as rates of interest within the monetary markets rise, Plaza Retail additionally faces and should take care of a rising value of debt. Which means I have to preserve an in depth eye on Plaza’s quarterly efficiency to ensure the beneficiant dividend is not in jeopardy.

This text is meant as an replace to earlier articles which you could find right here.

Efficiency for 1 quarter

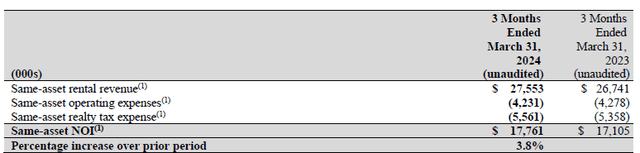

Wanting on the first quarter outcomes, the property are performing as anticipated. Plaza Retail was capable of document a web enhance in web working earnings from the identical property of roughly 3.8% year-over-year to C$17.8 million.

Plaza Investor Relations

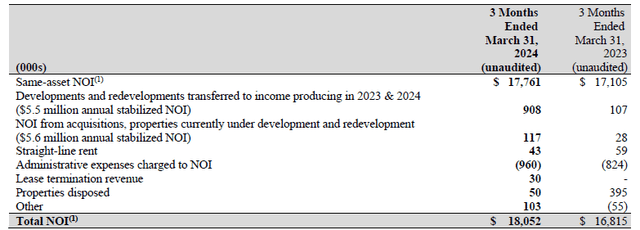

That being mentioned, Plaza has additionally invested in extra ground area, whereas there are some particular G&A gadgets which are charged to NOI efficiency. As you may see under, this added virtually one million Canadian {dollars} to the NOI end result. Whole NOI was roughly C$18.05 million.

Plaza Investor Relations

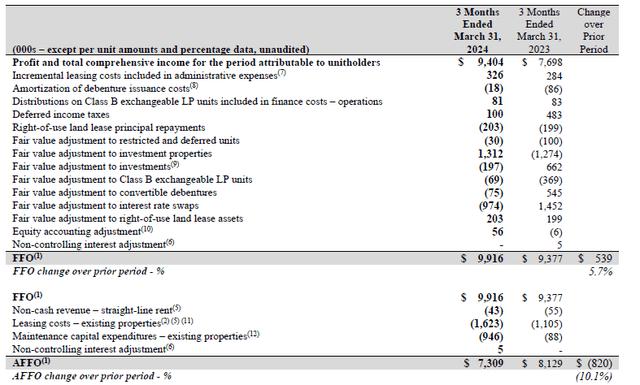

When REITs, FFO and AFFO outcomes are clearly extra essential than web earnings. As you may see under, Plaza Retail was certainly capable of submit a considerable enhance in its FFO numbers, which jumped almost 6% to C$9.9 million from simply C$9.4 million within the first quarter of final yr.

Plaza Investor Relations

This resulted in FFO per share of roughly C$0.089 per share, broadly according to final yr’s end result as the upper common variety of shares reduces the influence on efficiency per share.

In Canada, the AFFO calculation additionally contains capital upkeep prices. As you may see within the picture above, capital upkeep prices have been round C$0.95 million, whereas rental-related prices have been round C$1.6 million. This positively impacted the AFFO backside line, which was down about 10% to C$7.3 million, representing AFFO of C$0.066 per share. That is disappointing, however take into account that these prices have been extraordinarily excessive within the first quarter as capital upkeep and leasing prices greater than doubled in comparison with the primary quarter of final yr. I stay up for seeing how these prices develop over the subsequent few quarters. I count on them to say no, which can instantly enhance AFFO, as 1Q AFFO was not sufficient to cowl the month-to-month dividend of C$0.0233/share.

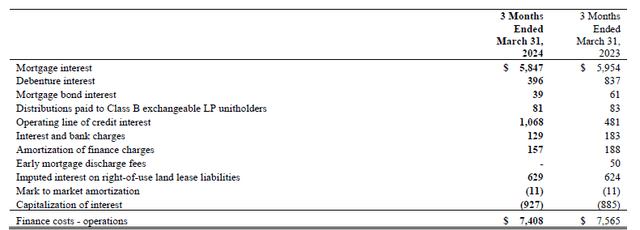

One of many massive questions within the present funding local weather is how rates of interest will have an effect on FFO and AFFO going ahead. As you may see under, the REIT paid about C$5.85 million in mortgage curiosity and C$1.07 million in curiosity on the road of credit score. I’ll enhance these two gadgets since they make up the vast majority of the whole curiosity expense.

Plaza Investor Relations

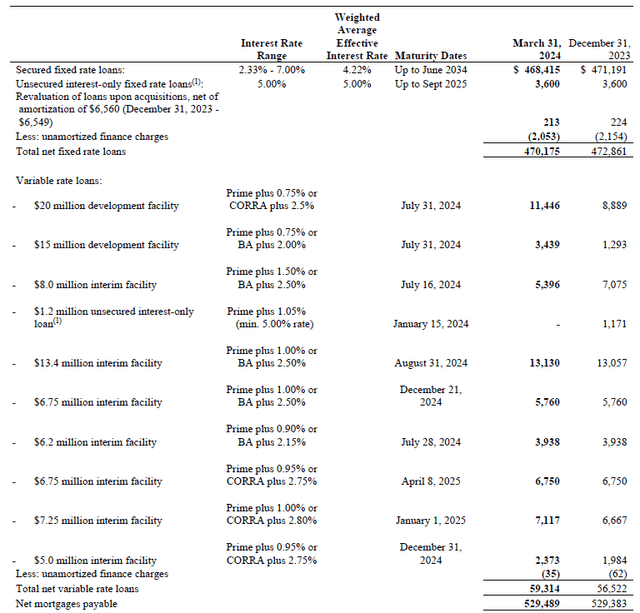

On the finish of the primary quarter, the REIT had slightly below C$530 million in mortgage loans excellent, which means a weighted common loan-to-value ratio of roughly 4.4%. As you may see under, the overwhelming majority of mortgages have a hard and fast rate of interest, averaging 4.22%, however with rates of interest starting from 2.3% to 7%, with repayments unfold over the subsequent decade. Plaza acquired a brand new 10-year mortgage throughout the first quarter of the yr and was capable of lock in an rate of interest of 5.69%.

Plaza Investor Relations

The mortgage is a dearer type of debt, because the rate of interest on the mortgage is +0.75% or bankers’ acceptance plus 2%. This line of credit score matures within the third quarter of this yr, and will probably be attention-grabbing to see what phrases the road of credit score shall be renewed on. I count on Plaza will once more have a floating fee credit score facility to make the most of the chance for decrease rates of interest within the monetary markets.

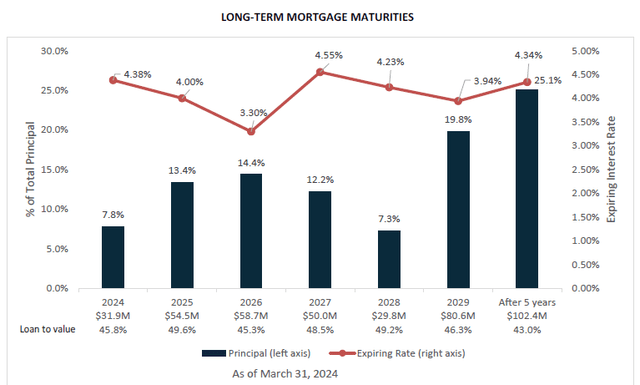

Between now and the top of 2026, the REIT should refinance solely about C$145 million in mortgages. They’ve a weighted common rate of interest of three.8%, so I believe it is truthful to imagine that the typical value of debt will enhance by 100-150ba. charges than in 2024 and 2025, given the expectation of decrease rates of interest in monetary markets). This is able to quantity to roughly C$2 million per yr in extra curiosity expense by the top of 2026.

Plaza Investor Relations

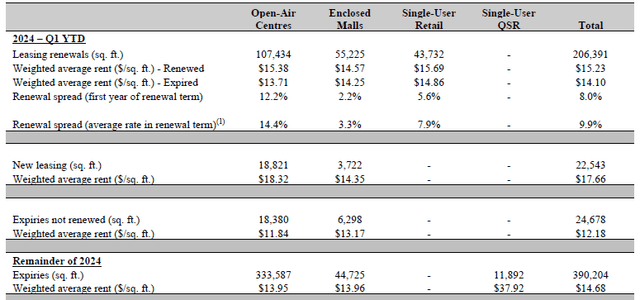

I count on the REIT to have the ability to offset the upper curiosity expense with increased rental earnings. Leasing spreads have been fairly spectacular within the first quarter of the yr as Plaza reported a median renewal unfold of 9.9%, because of outside facilities the place renewal spreads exceeded 14%.

Plaza Investor Relations

As you may see within the picture above, there are over 330,000 sq. toes which are up for renewal within the remaining three quarters of the yr. It will likely be attention-grabbing to see the extension spreads on these extensions as some have contractual phrases and others shall be renegotiated available in the market. As you may see under, an extra 1.47 million sq. toes shall be renewed in 2025 and 2026, and additional lease will increase ought to enable the Plaza to cowl the aforementioned anticipated enhance in curiosity expense.

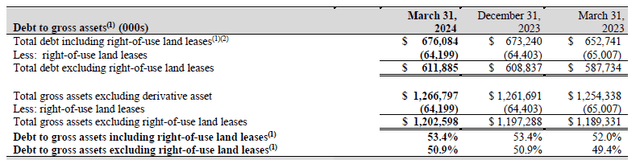

On the finish of the primary quarter, the REIT had roughly C$9 million in money and C$676 million in liabilities, with roughly C$667 million in web monetary liabilities (together with lease liabilities). With compensation of roughly C$1.23 billion in property and investments, the LTV ratio is roughly 54.5%. The REIT publishes a gross debt-to-asset ratio (which isn’t fairly the identical as conserving money as an asset relatively than calculating a web debt place), leading to a debt ratio of 53.4% together with lease and 50.9% with out lease accounting.

Plaza Investor Relations

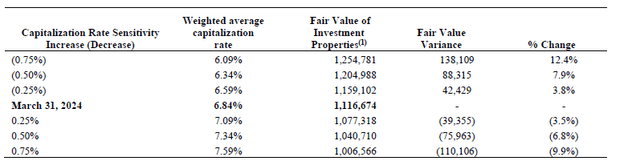

Though this can be a comparatively excessive LTV ratio, take into account that the property is valued at a really cheap capitalization fee. As you may see under, the typical cap fee was 6.84%. And even if you happen to enhance the cap fee to 7.59%, the steadiness will lose about C$110 million in worth. That is lower than 10%, which implies that the LTV ratio will stay under 60%.

Plaza Investor Relations

Then again, if curiosity and capitalization charges decline sooner or later and the REIT is ready to use a decrease cap fee, reminiscent of 6.50%, it could probably add about C$58 million in worth.

Funding thesis

As of the top of the primary quarter of 2024, the e-book worth per share was roughly C$4.95 (adjusting the impact of C$4.2 million of LP Class B trade items on the variety of shares). This implies the inventory is at the moment buying and selling at a reduction of round 25% to its e-book worth. On the present share value, the dividend yield is roughly 7.6%, and whereas the distribution was not absolutely coated by the 2024 Q1 AFFO outcomes, I believe the full-year end result will cowl the distribution within the type of upkeep capex and leasing prices within the first quarter of the present yr have been comparatively excessive.

I at the moment shouldn’t have a place in Plaza Retail REIT as a result of I most popular different Canadian REITs. Plaza is affordable when it comes to NAV and enticing when it comes to earnings. However based mostly on its AFFO efficiency with AFFO per share of C$0.291 in fiscal 2023 and my expectation to see AFFO of C$0.30 this yr, the earnings ratio shouldn’t be very low. However as talked about earlier, the extension spreads are fairly sturdy, and hopefully this could enhance earnings considerably.

Editor’s Notice: This text discusses a number of securities that aren’t traded on a serious US trade. Pay attention to the dangers related to these shares.