jetcityimage

Occidental Petroleum (NYSE: OXY) is without doubt one of the largest oil firms on the planet with a market capitalization of practically $60 billion. The corporate can be one of many largest holdings of our favourite buyers (Berkshire Hathaway) after the corporate broke in throughout The COVID-19-related battle after incurring an enormous quantity of debt to accumulate Anadarko Petroleum. As the corporate progresses, we’ll see on this article the way it’s an fascinating funding so as to add throughout downturns.

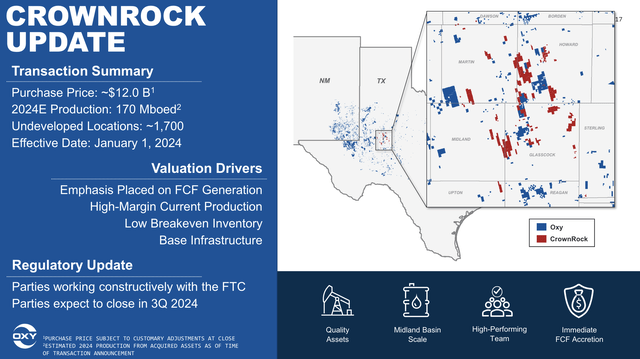

Occidental Petroleum CrownRock

Occidental Petroleum lately made one in all its largest acquisitions for the reason that acquisition of Anadarko Petroleum, the $12 billion acquisition of CrownRock.

Occidental Petroleum Investor Presentation

The acquisition is predicted so as to add 170,000 barrels per day of contemporary manufacturing and shall be terminated within the subsequent few months. The asset is predicted so as to add 1,700 undeveloped and powerful areas effectively built-in into Occidental Petroleum’s present sown space. The corporate expects to obtain robust working margins and FCF development from the acquisition, and expects this to be accretive on a per-share foundation. Nevertheless, he has vital money owed to repay.

The acquisition comes at a time of serious consolidation within the trade, and with the corporate’s robust shale property, it is actually costly, however we like that it was performed with debt slightly than a further share difficulty. Total, we anticipate the acquisition to be accretive to long-term shareholder returns.

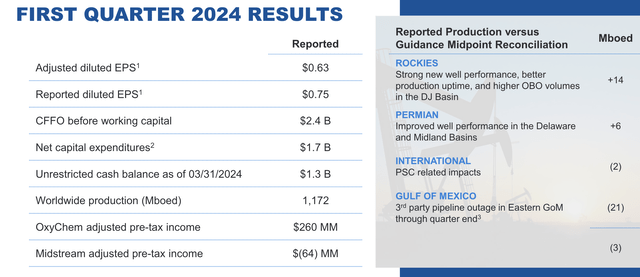

Occidental Petroleum Q1 2024 efficiency

Occidental Petroleum had fairly robust ends in the primary quarter of 2024 regardless of persevering with to put money into its enterprise.

Occidental Petroleum Investor Presentation

The corporate continues to provide practically 1.2 million barrels per day, excluding the CrownRock acquisition, which is able to push that 1.3 million barrels per day. The corporate’s CFFO was $2.4 billion, however capital expenditures remained excessive, with an annualized FCF of about $700 million ($3 billion annualized). Capex is predicted to stay flat, however we anticipate the corporate’s FCF to enhance shifting into the again half.

The corporate continues to carry out strongly in its enterprise segments with a formidable portfolio of property. The corporate expects the acquisition of CrownRock to assist it additional, with FCF steerage of greater than $5 per share at a post-acquisition WTI worth of $75. This helps present the energy of the corporate’s asset portfolio.

Low Carbon Occidental Petroleum

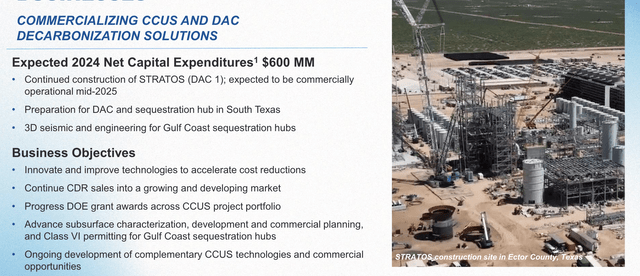

Oil firms now calmly admit that local weather change is an issue and the necessity to cut back world CO2 emissions. There are alternate options for a lot of types of emissions, comparable to fixing leaks in pure gasoline pipelines or constructing high-speed rail as a substitute of short-haul air journey. Nonetheless, for sustainable emissions there’s carbon seize, a posh enterprise that Occidental Petroleum hopes to make use of its experience to construct.

Occidental Petroleum Investor Presentation

The enterprise is sort of costly, with the corporate planning to spend $600 million in web capital expenditures in 2024, practically 10% of complete capital expenditures. The corporate expects its first DAC plant to be in industrial operation in mid-2025, and it plans to construct a middle in Texas, the place it already has a formidable enterprise. The corporate hopes to construct extra sequestration facilities and expects to take care of capital expenditures at <$600 million by means of 2026.

The Firm expects future DAC plans to fulfill the return thresholds for FID. There may be a variety of uncertainty, significantly round long-term dependable demand for giant initiatives and the affect of regulation. Nevertheless, the corporate sees itself effectively to have a robust enterprise right here.

Occidental Petroleum FCF Enhancement

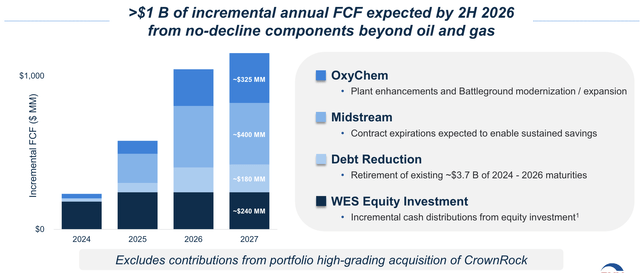

Occidental Petroleum additionally sees a chance to develop FCF by greater than $1 billion by 2H2026.

Occidental Petroleum Investor Presentation

The corporate expects this development to return from quite a lot of sources, together with incremental FCF of over $1 billion incrementally by means of 2H2026. These positive aspects additionally come from continued investments in midstream and OxyChem plant enhancements, in addition to the corporate’s focused debt discount. This FCF achieve is large for a corporation valued at practically $60 billion and, mixed with decrease debt, will assist a robust give attention to earnings.

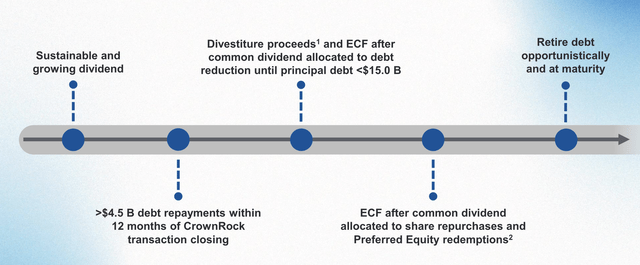

Returning Occidental Petroleum Shareholders

The corporate has various priorities because it focuses on persevering with to generate robust returns for shareholders.

Occidental Petroleum Investor Presentation

The principle focus of the corporate is a steady and rising dividend, nevertheless the corporate’s dividend could be very low – just one.4%. There’s nothing significantly thrilling about regular dividend development given how a lot the corporate’s earlier dividend cuts have been. The corporate’s instant objective after buying CrownRock is to pay down $4.5 billion in debt, lowering the whole debt raised by the acquisition.

The corporate continues to make use of gross sales and debt repayments to scale back underlying debt under $15 billion. After that, the corporate plans to work on paying off Berkshire Hathaway’s anticipated most popular inventory, which carries a ten% premium, however at an 8% yield, continues to be value paying off in comparison with its debt load. This, mixed with opportunistic debt buybacks, will proceed to enhance the corporate’s general shareholder return profile.

This helps make the corporate stand out as a worthwhile funding.

Threat thesis

The most important threat to our thesis is crude oil costs. The carbon seize firm enterprise continues to be extremely younger, and it isn’t sufficient to construct an organization. Because of this, the corporate must generate adequate money circulate from its core enterprise, which implies oil costs should stay excessive. The corporate wants WTI costs at $80+ per barrel to ship double-digit shareholder returns. There’s a lot that may cease this, as the corporate has vital dangers which are value noting.

Conclusion

Occidental Petroleum was as soon as an organization whose administration was hated, as the corporate’s commerce struggle for Anadarko Petroleum left it with an enormous quantity of debt on the flawed time. Nevertheless, the corporate has since acknowledged its errors together with the affect of the Black Swan occasion of Covid-19 and has labored to enhance its general portfolio and improve shareholder returns.

The corporate faces comparatively low oil costs, with WTI simply above $80 WTI. The corporate is presently fairly worthwhile, however it would not present unreasonably excessive returns for shareholders, making it an funding it doesn’t matter what. Regardless of the corporate’s falling share worth, in addition to its robust and enhancing asset portfolio, including throughout the downturn makes the corporate a helpful funding alternative.

Please tell us your ideas within the feedback under.