SlavkoSereda/iStock by way of Getty Photos

Funding thesis

StoneX Group (NASDAQ:NASDAQ: SNEX) continues to construct capital, constantly rising income and earnings over the previous few years. With a powerful return on fairness and a well-diversified enterprise, StoneX continues will shock me with its regular development and enticing long-term development alternatives. Even at a good valuation, I believe the inventory continues to be enticing given its monitor report of fairness and excessive ROE. To me, StoneX appears like an excellent enterprise at a good value, which makes me fee the inventory as a purchase.

Firm overview

StoneX goals to attach its shoppers with no matter markets they should handle threat, commerce strategically with alternatives and meet their operational enterprise wants. Their technique, in response to the annual report, is to “be the only trusted associate for our clients by offering our community, merchandise and providers that permit them to benefit from buying and selling alternatives, handle their market dangers, make investments and enhance their enterprise outcomes.”

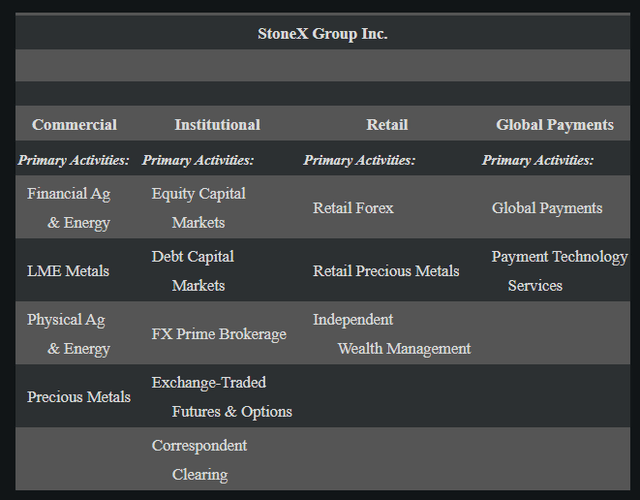

The corporate divides itself into 4 segments: industrial, institutional, retail and international funds, in response to the annual report. With “greater than 54,000 industrial, institutional and international fee shoppers and greater than 400,000 retail accounts situated in additional than 180 international locations,” StoneX has a monitor report of delivering worth to various shoppers by serving to them commerce extra effectively and strategically.

The industrial section refers to “actions associated to the identification, administration, hedging and monitoring of the varied commodity and monetary dangers confronted by industrial entities of their enterprise cycles.” As a one-stop store for its industrial shoppers, StoneX presents threat administration advisory options, execution and clearing providers, in addition to market evaluation and analysis.

Institutional section refers to “a full suite of fairness buying and selling providers to assist them discover best-executed liquidity, constant liquidity throughout a sturdy array of mounted revenue merchandise, aggressive and environment friendly clearing and execution on all main futures and securities exchanges worldwide , and as a chief dealer in equities and main forex pairs and swaps.”

The retail section goals to “present our retail shoppers all over the world with entry to greater than 18,000 international monetary markets, together with spot forex and CFDs, that are funding merchandise whose returns depend upon the efficiency of the underlying belongings, in addition to monetary buying and selling and bodily funding in treasured metals”.

World Funds “present custom-made fee, know-how and treasury providers to banks and industrial enterprises, in addition to charities, NGOs and authorities organisations”. It focuses on serving to clients with overseas alternate and forex alternate, facilitating cross-country funds safely and effectively.

10-Okay

As a diversified monetary providers firm, StoneX is on the middle of serving to shoppers commerce neatly and handle dangers fastidiously. I see it as an enormous matchmaker that comes with many built-in options to determine itself as a family identify within the monetary area, changing into a real one-stop store for all its clients’ buying and selling wants. I just like the enterprise and consider the worth they supply is critical based mostly on the corporate’s constant elementary development.

Robust Q2 earnings reinforce development story

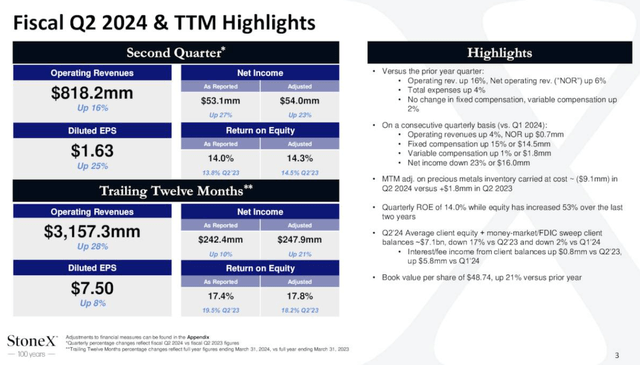

On Could 8, 2024, the corporate introduced what I assumed had been implausible Q2 earnings numbers, confirming my perception that the corporate’s regular development ought to proceed. In keeping with this press launch,

Quarterly working revenue $818.2 millionup 16%

Quarterly internet revenue 53.1 million {dollars}ROE of 14.0%

Quarterly diluted earnings per share 1.63 US {dollars} per share, up 25%

Most of this development occurred in retail and establishments, the place working revenue elevated by 30% y/y and 28%, respectively, in comparison with the second quarter of final yr. Administration attributes this to their “diversification of each our merchandise and buyer base,” which leads me to consider they got here up with new merchandise to draw new clients to additional develop their enterprise.

Return on fairness stays robust, and in response to the transcript, it was “14.8% return on fairness on tangible belongings and 14% return on fairness on reported e book worth, which as a reminder has elevated 53% over the previous two years , with each figures near our long-term goal of 15%.” I consider that ROE can stay at round 15% in the long run on account of their monitor report of retaining clients and creating revolutionary merchandise to diversify their providing. Therefore, the funding in StoneX just like investing in a fund that’s 15% yearly, which to me could be very enticing, even at a good valuation, the return earned by the investor will probably be roughly equal to the precise return on capital that the enterprise earns over an extended time frame.

For my part, the retail section was the spotlight this quarter, with administration detailing their earnings development,

We noticed year-over-year income development throughout all of our segments over the previous 12 months, led by retail, which grew by 127%, adopted by funds, which grew by 24%.

I consider the retail section is gaining momentum and can turn into extra essential within the development story as I see the industrial section as comparatively mature and mature at this level. Mockingly, StoneX’s web site calls retail buyers “self-directed shoppers” out of respect and presents them bodily investments in treasured metals. I discover StoneX Bullion (their bodily treasured metals enterprise) notably enticing in immediately’s markets as many buyers can use it as a hedge towards inflation. Finally, I believe the administration has been very revolutionary in arising with new concepts to develop their product providing and entice new clients, particularly the retail crowd.

A one-stop store strengthens the bond with the shopper

I consider that the mission to be a one-stop store for buyer wants has elevated silos, making switching to a different service supplier much more troublesome. The primary aggressive benefit I see right here is switching prices, as clients are extremely depending on StoneX’s again workplace and buying and selling providers, so they can’t go away StoneX simply.

To again up that declare, I am seeing large year-over-year development with no hiccups in step with their presentation.

Presentation for the investor

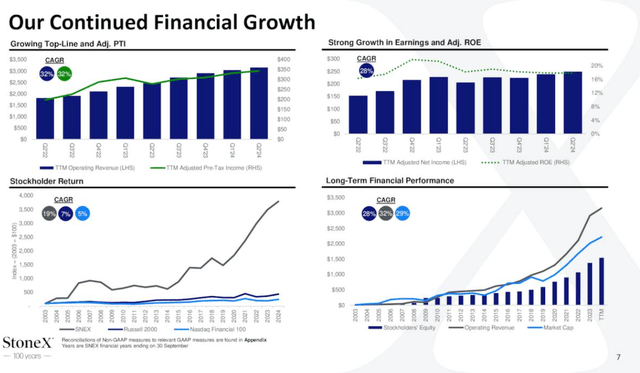

An organization that continues to generate constant earnings and ROE ought to have some aggressive edge, and I consider the mix of excessive leverage with enticing unit economics makes this a extremely worthwhile and fast-growing enterprise. As a service firm, they’ll earn very enticing spreads and commissions based mostly on market exercise and have a versatile price construction that’s largely depending on buying and selling quantity. Subsequently, even in the course of the pandemic disaster, their working income grows in a straight line in response to the presentation, demonstrating their resilience to financial shocks.

I consider the underside proper graph on web page 7 says all of it. Over the long run, for my part, shares are all the time in step with fundamentals, and market capitalization intently follows working revenue and fairness. Assuming the corporate can retain its robust buyer base, introduce new merchandise and diversify its buyer base, the inventory ought to proceed to observe an orderly path to working revenue. StoneX appears to be very immune to financial modifications, so oil costs, pandemics, rates of interest and inflation do not appear to have the ability to cease StoneX from going increased and better. As a monetary providers supplier, they need to profit from this volatility as they supply their shoppers with threat administration and hedging instruments to guard them from market volatility.

Analysis is a long-term compounding machine

Valuing a long-term compound will be difficult as a result of I consider that although the multiples are in step with the sector median, shopping for an excellent long-term compound at a good value is definitely a misleading commerce. My level is that it could not look low cost, however as soon as buyers issue within the development and excessive return on capital, shopping for this inventory at a good value is an effective deal. So, I will not use “goal value” right here as a result of I believe buyers can purchase and maintain this identify so long as the basics are rising.

Assuming earnings can proceed to develop at a 15% CAGR over the subsequent few years, I count on the inventory to observe go well with. At 10x diluted EPS of $7.50, the inventory trades at a good value, however I count on diluted EPS to develop at round 10-15% CAGR over the subsequent few years on account of robust retail and institutional development and constantly excessive return on capital. Finally, the inventory ought to present buyers with round 10-15% returns with comparatively low threat as the corporate seems to be extremely resilient to financial shocks.

Presentation for the investor

As belongings underneath administration develop over time and extra buyers enter the scene, long-term financial development ought to propel StoneX ahead. There’s all the time some threat that must be insured, and buying and selling exercise ought to improve yearly, which can improve charges and commissions for StoneX. I view this long-term compound machine as a purchase on account of its development and excessive return on capital, with every part buying and selling at a good value immediately.

Dangers

Repute is essential and StoneX should be cautious in managing its enterprise to keep up its model. Regulatory compliance, fixed innovation in service enchancment and a diversified buyer base appear to be essential for the protected development of this enterprise. StoneX should be certain that all stakeholders they cope with conduct enterprise ethically and responsibly in order to not injury their popularity.

StoneX relies on continued volatility within the markets to promote the derivatives essential to hedge this threat. Until there’s a drastic change in commodity costs, the demand for StoneX’s hedging providers could lower as individuals needn’t hedge their dangers, so in a means volatility is a significant benefit for StoneX. Traders ought to count on markets to stay risky, however any authorities intervention by way of commodity value flooring and ceilings might damage StoneX’s fundamentals.

The trade stays extremely aggressive with many choices to select from by way of market makers and hedging answer suppliers. StoneX should proceed to stay aggressive on value and quantity to draw new clients to develop its enterprise. As well as, StoneX should be conscious of counterparty credit score threat as a result of some shoppers could use margin for his or her buying and selling actions and will default on their margin obligations.

Purchase StoneX

I consider I’ve discovered an excellent long run folding machine commerce at a good value. I believe the long-term shareholder return will probably be roughly equal to the precise return on the enterprise’s fairness (15%) over the long run, so I count on buyers to obtain 15% yearly so long as they maintain the inventory. With its resilience to financial shocks and poised to learn from value volatility, I view StoneX as a protected haven from market crashes and fee the inventory as a purchase.