by no means

Gladstone Funding (NASDAQ:NASDAQ: ACQUISITION) has been one in all my favourite BDCs since late final December, after I took a better have a look at its fundamentals, figuring out that the chance/return profile was enticing sufficient to go lengthy.

The motivation behind the purchase advice with revenue got here from the next features:

- One of many lowest ranges of leverage within the BDC sector.

- Vital publicity to most popular shares, which not solely generate secure money flows, but additionally supply elevated upside potential if rates of interest fall.

- The main target is on corporations with money circulation which have already organized their actions in comparatively defensive industries.

- Stringent underwriting requirements end in diminished portfolio threat publicity and thus a diminished probability of great non-accruals being acknowledged.

The counterargument was the tiny GAIN portfolio, which inherently limits the overall possibility area the place you’ll be able to interact in LBOs, M&As and different transactions that usually require vital quantities of exterior financing. Equally, the truth that GAIN has not used its leverage potential may theoretically imply diminished upside potential in a bull market situation.

Nevertheless, given my funding technique, which favors protection over offense and primarily focuses on the sustainability of underlying dividends, the above advantages have been greater than sufficient to offset any potential downsides.

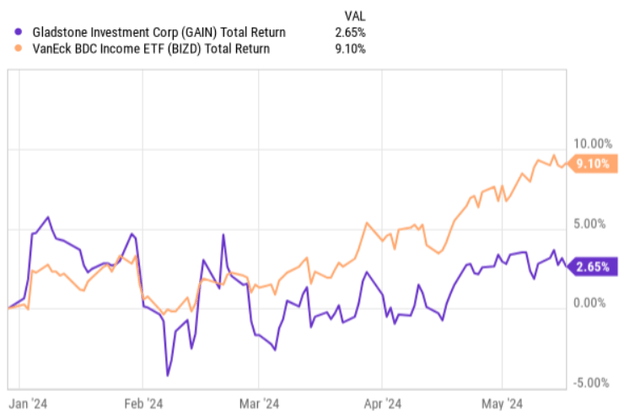

For the reason that publication of my bullish thesis, GAIN has delivered strong outcomes, however underperformed the BDC market, which has typically skilled headwinds, principally from a strengthening higher-for-longer rate of interest situation. That is in line with my assumption earlier than recommending a purchase on GAIN, which is that in a powerful BDC market, it’s more likely to underperform the index resulting from decrease leverage, which lowers the general beta part.

Ycharts

GAIN simply launched its This autumn 2024 earnings report, which reveals a brand new set of information price contextualizing in opposition to my present thesis. Let’s check out the revenue deck and decide if the scenario stays hopeless.

Evaluation of thesis

The fourth quarter introduced a blended bag of messages that, when checked out extra deeply, boil all the way down to the continued favorable dynamics of the core enterprise.

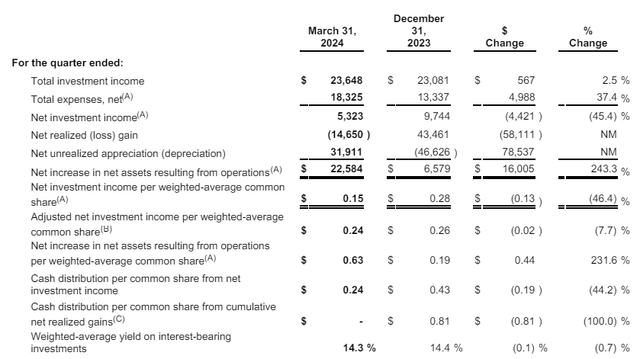

At first look, essentially the most disappointing facet of the 4Q outcomes was the marked drop in internet funding revenue, which got here in at $5.3 million from $9.7 million within the prior quarter. Wanting on the prime line, we see that it truly improved by about $0.5 million, but it surely was the broadening of the fee base that drove the underside line (ie internet funding revenue) down. Internet bills for the fourth quarter have been $18.3 million, a rise of roughly $5 million from the prior quarter. So, if we have been to cease at this and correlate it with the underlying dividend, we’d simply conclude that the distribution is unsustainable and that GAIN will revise the dividend down ultimately.

Nevertheless, the primary motive why the web value part grew a lot was because of the profitable realization of fairness investments, which opened up vital capital positive aspects from the built-in e book values, which have been registered comparatively way back, when GAIN invested its capital within the capital of corporations.

Due to this fact, the rise in value base was primarily pushed by incentive charges primarily based on capital positive aspects, which might be thought of non-recurring and in addition considerably optimistic as they outcome from the profitable exit of the corporate.

Because the desk under reveals, adjusted internet funding, which excludes these fluctuations and focuses solely on curiosity elements, was $0.24 per share. That is barely decrease than the earlier quarter, when GAIN achieved a results of $0.26 per share.

GAIN This autumn 2024 Earnings Report

This drop of $0.02 per share is because of general margin compression within the BDC phase and largely resulting from GAIN having the ability to exit fairness positions, thus placing a headwind on the upside. Once more, that is one thing non permanent, and even when GAIN did not return an adjusted internet funding revenue outcome, it could nonetheless be sufficient to cowl the dividend.

Now, on account of the exit, GAIN was capable of enhance its NAV by $0.42 per share after the distribution. Due to this fact, this drawdown alone generated sufficient capital to cowl the hole between adjusted internet funding revenue and dividends, and left a big quantity of liquidity untapped that might have been used to cut back debt or fund further investments.

Nevertheless, on a forward-looking foundation, I’d counsel that GAIN will have the ability to enhance its internet funding revenue backside line because it does simply that: both additional reduces debt or begins to underwrite extra vital new funding by leveraging its robust stability sheet (which has one of many lowest leverage profiles within the BDC area).

Primarily based on President Dave Dallum’s feedback in the course of the current earnings name, it additionally seems that GAIN will proceed to slowly however certainly interact its fairness portfolio to unlock the embedded worth that ought to ultimately present a headwind to earnings or its stability sheet.

As our portfolio has matured, we have been engaged on this since 2005, and the price of fairness has been, we’ll clearly have the ability to proceed to constructively accumulate these returns for the advantage of shareholders. As you all know, we are able to, due to our mannequin, be in a few of these corporations for a protracted time period, and it is actually to the advantage of the shareholders that we do not have to go away the businesses too rapidly with out having the ability to help them. We are going to proceed to stability the timing of exits whereas sustaining the extent of our revenue producing belongings essential to help the month-to-month dividend ranges we’re at the moment capable of obtain and hopefully proceed to extend over time.

Backside line

On the face of it, the newest quarterly outcomes might seem to point a deterioration in efficiency, resulting in an unsustainable stage of present dividend protection.

Nevertheless, after peeling again the onion a bit, it’s clear that solely the profitable realization of beforehand made fairness investments launched incentive charges primarily based on capital positive aspects, which in flip diminished the ensuing internet return on funding.

Nevertheless, the truth that GAIN was capable of eliminate one in all its fairness pursuits elevated the NAV base and strengthened the liquidity profile, which not solely coated the non permanent hole in dividend protection, but additionally gave administration extra flexibility to cut back its borrowing additional or channel that capital into new interest-bearing investments. Both one ought to assure a better internet funding revenue outcome.

Given the aforementioned dynamics and the plain worth potential in Gladstone Funding’s inventory portfolio, the inventory is price shopping for.