SI pictures

Introduction

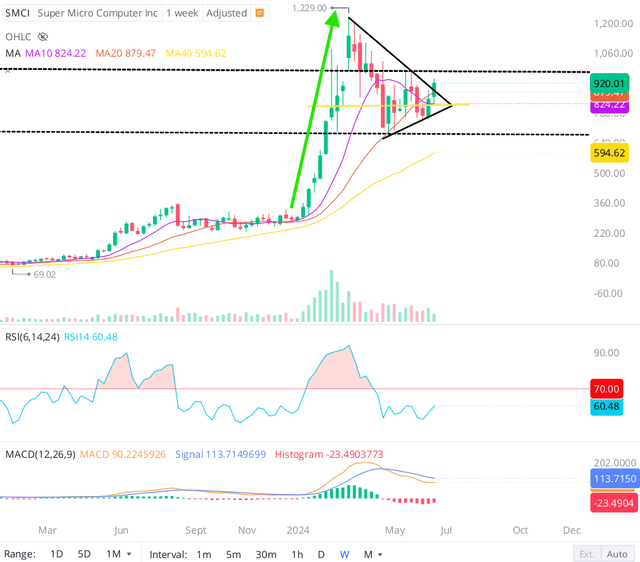

After hovering from ~$300 to ~$1,200 earlier within the yr, Tremendous Micro Pc, Inc. (NASDAQ: SMCI) inventory fell ~45% on its $2 billion fairness providing in March and has been consolidating in direction of a variety since then.

Webull workbench

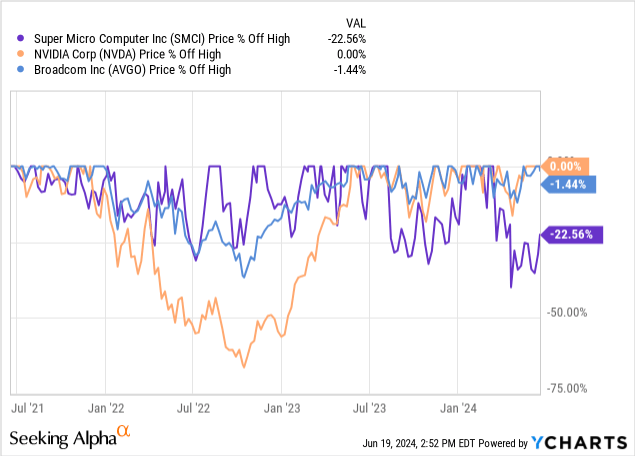

With AI shares like Nvidia ( NVDA ) and Broadcom ( AVGO ) hitting new all-time highs in current buying and selling periods, the red-hot pursuit of AI infrastructure exhibits no indicators of slowing down.

So why is Tremendous Micro Inventory completely different from its friends?

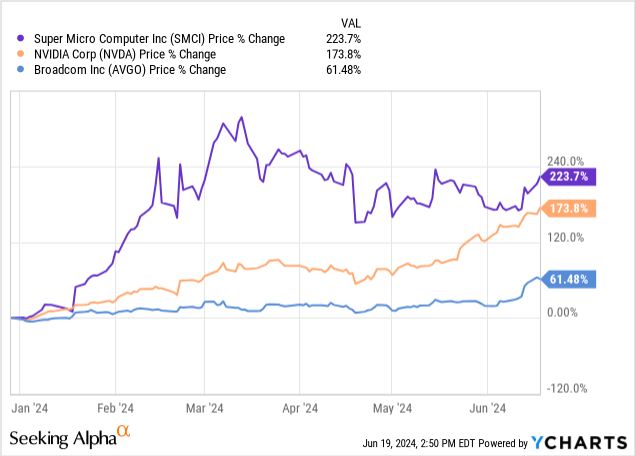

Earlier than discussing the potential elements behind Tremendous Micro’s current relative underperformance, I would like to focus on the truth that SMCI is the best-performing inventory within the S&P 500 ( SPY ) based mostly on year-to-date returns. Sure, Nvidia has closed the hole in current weeks, however for now, Tremendous Micro shares are nonetheless on sale dominance So the divergence between SMCI and its AI infrastructure friends could be a standard correction.

Nevertheless, Tremendous Micro peaked in mid-March of this yr, simply earlier than the corporate introduced a $2 billion fairness providing to boost capital. Given the extra provide of SMCI shares getting into the market, a value correction is barely pure.

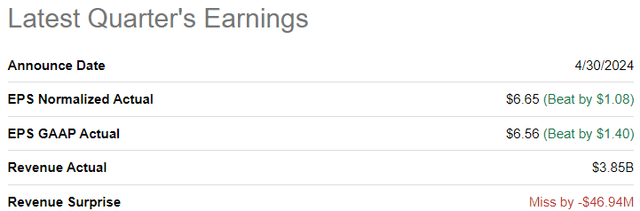

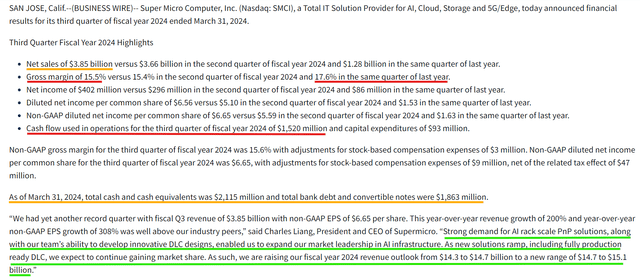

Furthermore, Tremendous Micro’s fiscal 3Q24 report missed buyers’ excessive expectations with income of $3.85 billion, consistent with administration’s steerage of $3.7 billion to $4.1 billion and lacking consensus estimates. Whereas Tremendous Micro simply beat EPS estimates on the again of higher scale, gross margins fell 210bps YoY to fifteen.5% in 3QFY24.

In quest of Alpha Tremendous Micro Report for Q3 FY2024

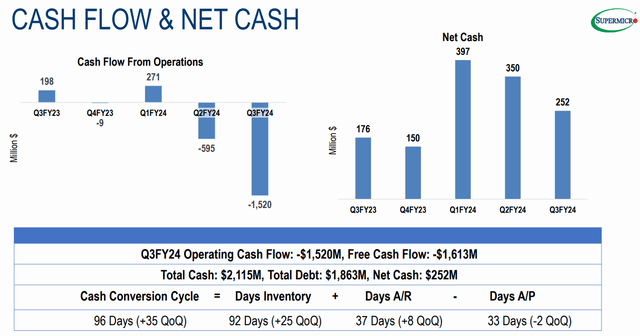

Along with the decline in gross margin, elevated stock resulted in unfavourable free money circulate of -$1.6 billion in Q3 FY24. Whereas Tremendous Micro’s administration expressed confidence that these stock and money tendencies could possibly be reversed within the coming quarters, SMCI’s comparatively small internet money stability of $250 million (2.1 billion {dollars} in money and money equivalents, $1.86 billion in convertible debt) leaves the likelihood for Tremendous Micro to dip into the capital markets to boost more money.

Tremendous Micro Report for Q3 FY2024

Is SMCI a purchase, promote or maintain at present ranges?

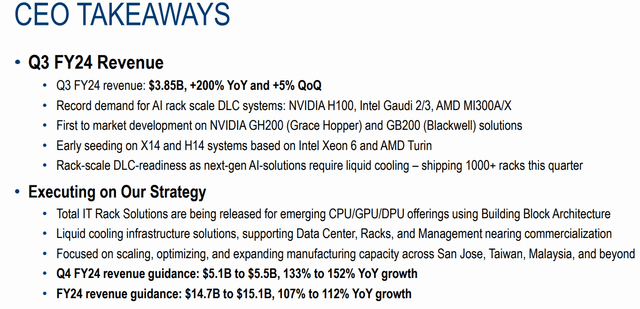

Whereas the 5% QoQ sequential gross sales progress raises some legitimate issues in regards to the sustainability of demand, Tremendous Micro’s administration hinted at robust demand for its synthetic intelligence DLC (direct liquid cooling) rack programs as they elevated fiscal 2024 income steerage to $14.7-$15.1. B (+107-112% y/y), with FY24Q4 income now forecast at $5.1-5.5 billion (+133-152% y/y, +32-43% sq/sq m).

Tremendous Micro Report for Q3 FY2024

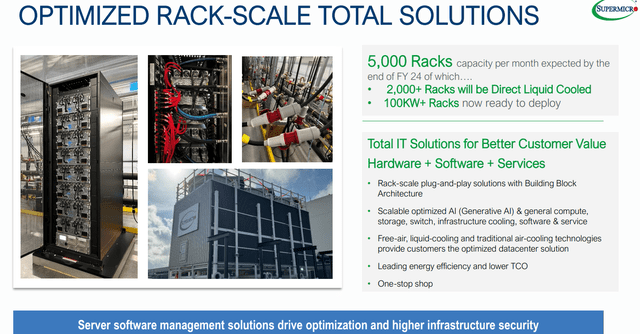

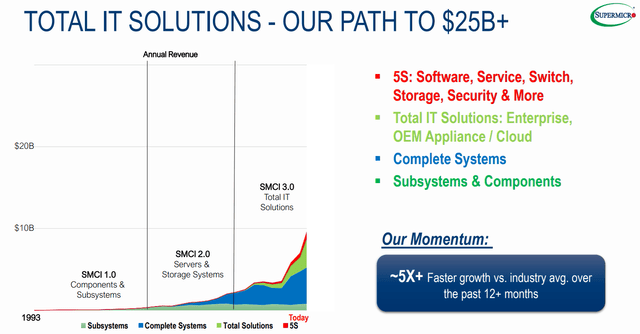

In my view, Tremendous Micro’s ~15% gross margin displays its restricted value-add and/or pricing energy as a supplier of plug-and-play servers. Nevertheless, SMCI goes past its core server system choices to ship end-to-end IT options ({hardware} + software program + companies) that assist Tremendous Micro’s path to $25 billion or extra in annual income and higher margins.

Tremendous Micro Report for Q3 FY2024 Tremendous Micro Report for Q3 FY2024

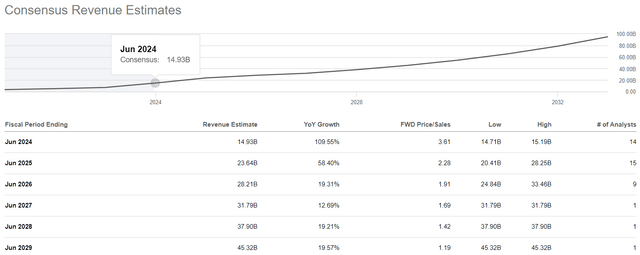

In keeping with consensus road estimates, Tremendous Micro’s income is forecast to develop from ~$15 billion in FY2024 to ~$45 billion by FY2029 at a CAGR of ~25%, or roughly 3x over 5 years!

In quest of Alpha

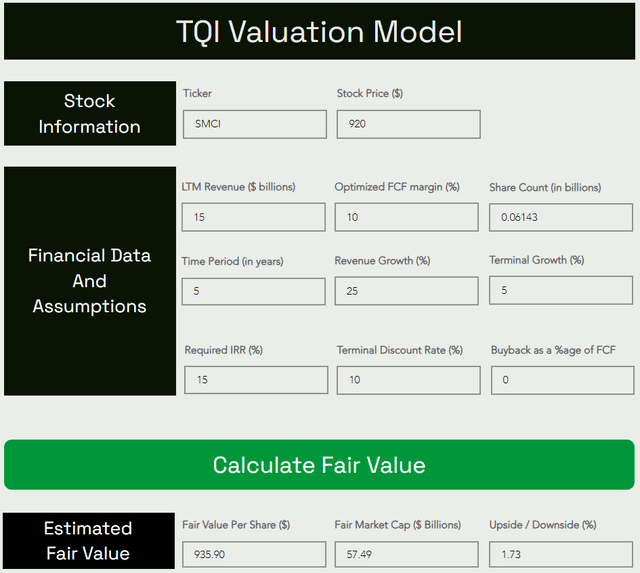

Whereas Tremendous Micro’s administration is optimistic about long-term profitability enchancment, working margins have been pretty secure round ~11%, and so I recommend an optimized steady-state FCF margin of 10%.

All different mannequin assumptions are fairly simple, however please share any questions you will have within the feedback part under.

Right here is my evaluation mannequin for SMCI:

TQI Evaluation Mannequin (free to make use of at TQIG.org)

Primarily based on affordable assumptions about future income progress and profitability, Tremendous Micro’s honest worth is ~$936 per share, roughly consistent with SMCI’s present buying and selling inventory.

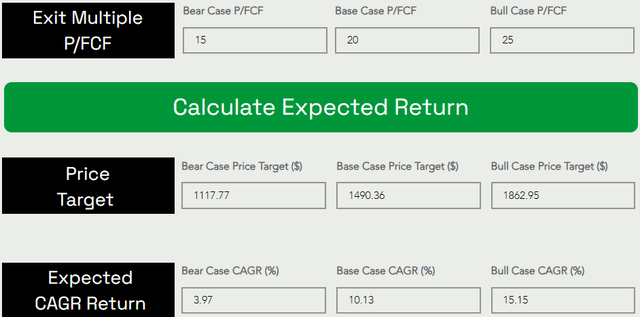

Assuming an exit a number of of 20x P/FCF, I see SMCI inventory rising to ~$1,500 per share over the following 5 years at a median annual progress price of ~10%.

TQI Evaluation Mannequin (free to make use of at TQIG.org)

Since SMCI’s anticipated 5-year CAGR returns fall wanting our funding stage of ~15%, I am not enthusiastic about shopping for Tremendous Micro inventory right here. Wanting forward, buyers can fairly count on to generate S&P-500 (8-10%) annual returns from SMCI over the following 5 years. Given Tremendous Micro’s inherent volatility, I would fairly simply personal the S&P-500!

Remaining ideas

Like picks and shovels, Tremendous Micro ought to proceed to profit from ongoing AI CAPEX spending. So I believe Tremendous Micro’s financials will proceed to be robust, at the very least within the close to time period. From a elementary standpoint, I do not see any main downsides to Tremendous Micro for the foreseeable future, given administration’s stable enterprise outlook and optimistic suggestions from tech giants like Nvidia and Dell ( DELL ).

In mild of the -25% decline from all-time highs, the long-term danger/reward for SMCI inventory has improved considerably, with the inventory slightly below my $936 honest worth estimate and the 5-year anticipated return rising to just about 10%. Primarily based on the rankings, the Tremendous Micro appears fairly priced; nonetheless, the chance/reward isn’t enticing sufficient for long-term buyers to warrant allocating new capital to SMCI inventory.

Now, can SMCI inventory proceed to maneuver larger within the mid-to-mid vary? Is that this a viable swing commerce?

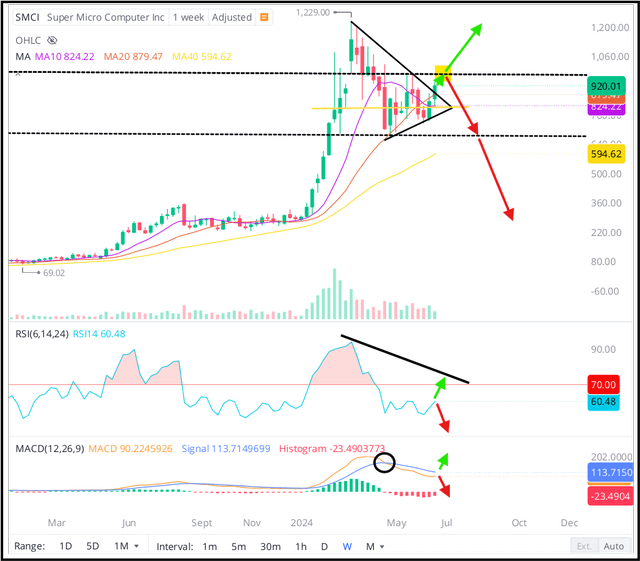

Final week, shares of Tremendous Micro jumped +16% from its 10-week shifting common and retook the 20-week shifting common. With the short-term development turning bullish (and the SMCI apparently breaking out of the triangle sample), I count on to see a retest of the higher boundary of the consolidation channel at ~$980 within the close to future.

Webull work desk

From there, SMCI inventory might actually go both approach. If we break above ~$980, the inventory might attain all-time highs (maybe across the 4Q earnings report subsequent month). Then again, if this newest bounce seems to be a bull lure, SMCI might collapse to $700 (the decrease boundary of the consolidation channel) – with divergences on the weekly charts confirming the bearish view.

Technically, Tremendous Micro shares are buying and selling at a make-or-break stage.

Whereas I do not personal SMCI, it is positively a inventory I am conserving a detailed eye on. If SMCI drops to the low to mid $700s (or we’ve got a big momentary correction), I might be a purchaser. For now I keep away.

Takeaway key: I price the Tremendous Micro as Impartial/Maintain at ~$900.

Thanks for studying and joyful investing! When you’ve got any questions, ideas, and/or issues, be at liberty to share them within the feedback part under.