Eugene Orlov/iStock by way of Getty Pictures

MMM Inventory: Nonetheless buyable close to 52-week excessive

I final wrote on Firm 3M (NYSE: MMM) shares initially of this 12 months in February. As proven within the chart under, I argued for a bullish thesis on the premise of artwork following issues:

3M lately settled its class-action lawsuits associated to its use of PFAS (aka, Perpetual Chemical compounds) and fight earplugs. These settlements can enhance public notion and result in elevated funding and investor confidence. MMM’s present valuation is engaging, with a excessive dividend yield and favorable earnings metrics.

After that, certainly, the inventory rose strongly. It has gained 30.6% since then and has a complete return of over 31.5%, effectively forward of the broader market’s 7% return over the identical interval. MMM’s revenue is even larger when the distribution of shares from Solventum Company (SOLV) spinoff is taken into account (extra on that in a minute).

Seeking Alpha

Normally, such a big value enhance in a brief time period weakens (and even invalidates) the bullish thesis. As costs rise, so do valuations and dangers. Nonetheless, within the case of MMM within the present setting, I’ll argue that the bullish thesis stays legitimate.

In the remainder of this text, I am going to clarify the underlying earnings drivers that would help even larger inventory costs. And a significant component is the completion of extra Solventum manufacturing, which is mentioned under.

MMM shares and Solventum spinoff

For readers unfamiliar with the background, MMM introduced plans to spin off its healthcare section a while in the past. The spinoff lastly occurred as lately as April. The brand new firm was named Solventum and now trades below the ticker SOLV on the New York Inventory Alternate. 3M shareholders acquired one share by way of the SOLV tax-free distribution for each 4 MMM shares, additional rising their whole revenue.

I see this spinoff as very optimistic for each firms. I anticipate MMM to obtain about $8 billion in income from the deal. MMM might use these funds to additional strengthen its monetary place and/or to develop different working divisions.

MMM’s healthcare section accounted for roughly 1 / 4 of whole revenues previous to the spin-off. So, shortly after the spin-off, MMM’s earnings per share may take successful within the close to time period, as seen within the chart under. Extra particularly, the chart reveals consensus earnings per share estimates for MMM over the following few years. As you may see, the market is anticipating a major decline in earnings per share in FY2024. Earnings per share for fiscal 2024 are estimated at $7.14, a decline of greater than 22% in comparison with the earlier 12 months.

Apart from the affect of the spinoff, I would not be stunned if different bills may additionally have an effect on the underside line. The principle points on my record embrace restructuring prices and authorized prices. As talked about in my earlier article, the corporate lately settled class motion lawsuits, agreeing to pay $10.3 billion to public water programs over the following 13 years to deal with PFAS points. It should additionally pay $6 billion over the following six years to the members within the Fight Ear Plugs lawsuit.

Seeking Alpha

Regardless of these headwinds (which I imagine are short-term or resolved), analysts are predicting a robust rebound in earnings per share after fiscal 2024. For fiscal 2025 and 2026, EPS is forecast to be $7.76 and $8.35, representing development of 8.61% and seven.67%, respectively. Total, its earnings per share are anticipated to rise to round $10 in 5 years.

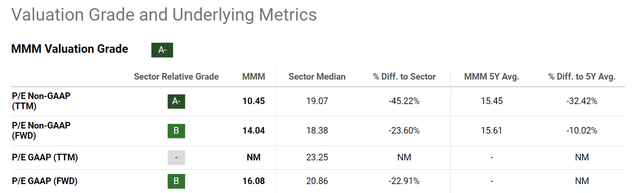

At 14x FWD P/E, the inventory is already buying and selling at a really engaging valuation, as seen within the subsequent chart under. In line with MMM’s inventory valuation ranking, its P/E ratio is effectively under each the sector median and 5-year common. On a ahead P/E ratio (primarily based on FY2024 estimates proven above), MMM trades at 14x. At a sector median of greater than 18x, this represents a reduction of 23.6%. The typical 5-year P/E ratio for MMM is about 15 occasions, about 10% larger than the present P/E. With projected development, valuation ratios will shrink even additional – at a reasonably speedy tempo – by an element of about 10 in simply 5 years.

Seeking Alpha

Different dangers and ultimate ideas

When it comes to draw back dangers, MMM and its industrial friends face many frequent challenges, reminiscent of financial downturns, which might considerably scale back demand for industrial merchandise. As well as, fluctuations in commodity costs and ongoing inflation (by way of labor prices, gas prices, and so on.) can scale back the speed of return.

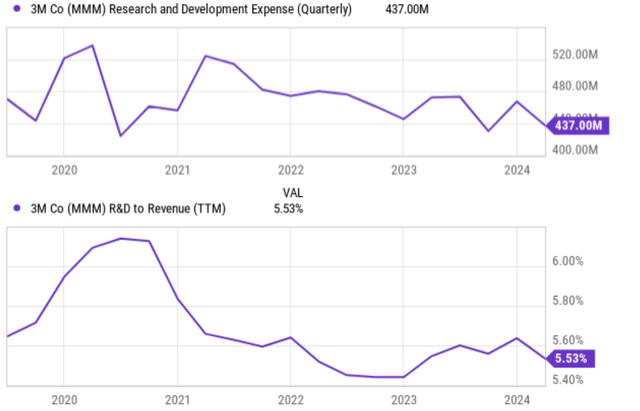

A extra distinctive danger for MMMs includes the potential for innovation stagnation. MMM has traditionally been a pacesetter in new product growth, however lately some traders are involved that this lead could also be slipping away. There are good causes for such apprehension. For instance, the chart under reveals MMM’s R&D spending in comparison with its historic common (high panel) and its R&D as a share of income in comparison with its historic common (backside panel). Each are exhibiting alarming indicators.

Wanting on the high panel, 3M’s present analysis and growth spending hovers round $437 million in the latest quarter, a major decline from the $520 million peak reached just a few years in the past. The underside panel reveals that 3M’s R&D spending as a share of income can be decrease than its historic common. As of the latest quarter, 3M’s R&D-to-revenue ratio was 5.53%, once more down considerably from its peak of round 6.2% just a few years in the past.

Seeking Alpha

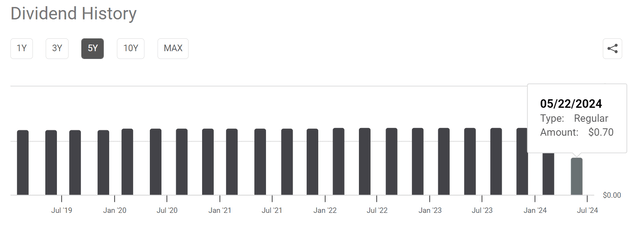

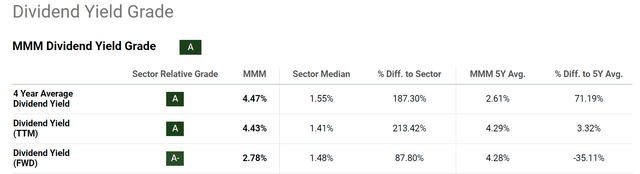

This brings me to the following danger: the current dividend lower. As you may see within the subsequent chart under, the Dividend King (MMM has constantly elevated its dividend for 65 years) lately determined to chop its payout. This growth may trigger some short-term ache and negatively affect sentiment amongst traders — particularly dividend traders. Nonetheless, total, I believe this choice is the precise one in the long term to assist the corporate spend money on itself and activate its innovation edge. Moreover, the dividend yield after the lower remains to be fairly engaging in comparison with the broader sector, as seen within the second chart under.

Total, my verdict is that the positives far outweigh the negatives. So my bullish thesis on MMM stays and I proceed to see it as a compelling purchase candidate. Admittedly, there might be EPS headwinds within the close to time period. Nonetheless, I anticipate a robust restoration in earnings per share within the subsequent 1-2 years.

In my opinion, the 2 important catalysts are the SOLV allocation and the settlement of probate litigation. For my part, the SOLV enterprise is a slower rising section. The completion of the spinoff ought to simplify operations and unlock the hidden worth of the inventory. Lastly, MMM’s P/E ratio sits at a major low cost to the sector median and its personal historic averages, including extra upside potential.

Seeking Alpha Seeking an alpha