Aleksei Baharov

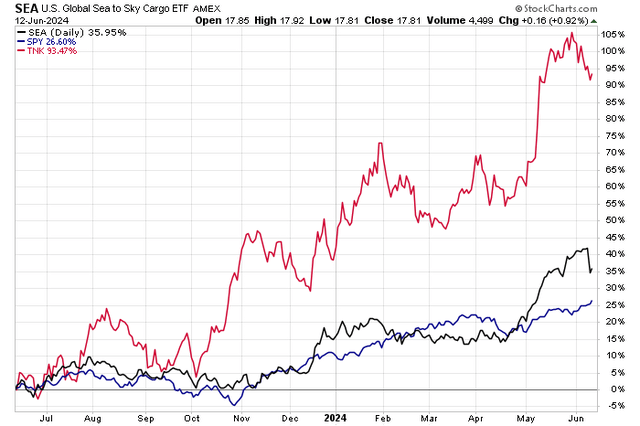

It’s troublesome to search out niches within the world inventory market which have outperformed the S&P 500 in 1 yr. Whereas U.S. large-cap shares, in line with the S&P 500 Belief ETF ( SPY ), are rising 27% from final yr, one transportation-focused fund is up 36% on a dividend foundation.

The US-based World Sea to Sky Cargo ETF (SEA) posted a powerful efficiency regardless of the media focus persevering with to be on AI and expertise. One of many fund’s largest holdings, Teekay Tankers (NYSE: TNK), main the way in which with development of virtually 100% in comparison with June 2023.

i repeat purchase ranking on the inventory, even after a big rally. After optimistic stability sheet tendencies and continued sturdy EPS development, I see a better honest worth for TNK in comparison with my earlier evaluation.

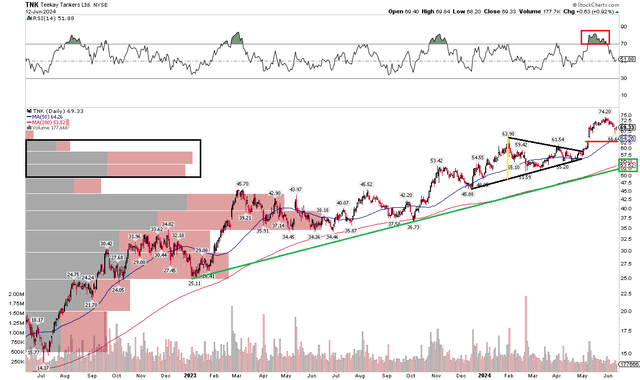

World transportation shares and shippers outperformed the S&P 500 YoY

Stockcharts.com

In response to Financial institution of America World Analysis, Teekay Tankers is without doubt one of the world’s largest tanker house owners and operators. It owns 53 midsize tankers and co-owns 50% of 1 VLCC chartered 9 for an working fleet of 54 tankers. The corporate owns a mix of Suezmax, Aframax, Product Tankers, help vessels and a 50% three way partnership curiosity in a single VLCC tanker.

Again in Might, Tikay knowledgeable strong set of quarterly numbers. Q1 non-GAAP EPS of $3.86 beat the Wall Road consensus estimate of $3.70, whereas income of $338 million, down 14% year-over-year, was a lot bigger than $118 million. The corporate famous that as of March 31, 2024, its liquidity place was wholesome at $692 million.

The agency continued to learn from a good tanker market, which led to larger spot charges and robust demand for tonne miles. Geopolitical conflicts have additionally contributed to business pricing, and the administration crew expects demand for Aframax vessels to extend with the commissioning of the Trans Mountain pipelines.

Whereas there was a modest drop in TCE charges, internet vessel income was sturdy at $222 million. Notably, the agency had no debt as of the tip of the primary quarter, after shopping for again the lease-back vessels, in line with BofA. Because of this, a particular dividend of $2 was issued.

The principle dangers for the corporate embody volatility within the cyclical tanker market and world delivery, in addition to diminished oil manufacturing, which reduces demand for the motion of oil all over the world.

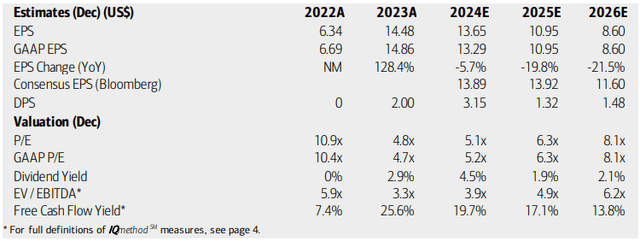

On the prospect of revenueBofA analysts see earnings per share falling from final yr’s peak ranges and finally falling under $9 by 2026. Nonetheless, the consensus numbers, in line with In search of Alpha, are extra optimistic, with working earnings per share starting from $13 to $14 as of as we speak. 2026. TNK’s income is round 800 million {dollars} yearly.

Dividends, in the meantime, is forecast to be $1.32 in 2025, excluding any particular dividends, however I believe that if money stream is strong, the administration crew might problem one other particular payout, however that is extra seemingly in spite of everything, will not be for a number of extra quarters. Nonetheless, free money stream is extraordinarily sturdy at $16.90 million during the last 12 months, leading to a 24% trailing FCF yield.

Teekay Tanker: Earnings, Dividends, Valuation, Free Money Circulate Projections

BofA World Analysis

If we assume non-GAAP normalized earnings per share of $13 and apply a five-year common earnings a number of, the inventory ought to be buying and selling round $95. However there is a draw back to taking a look at earnings, and with lackluster EPS development forward, it is good to decrease the a number of. A a number of of six would lead to a good worth of round $78, which I feel is extra applicable. Robust money stream technology and historical past of rewarding shareholders are optimistic elements.

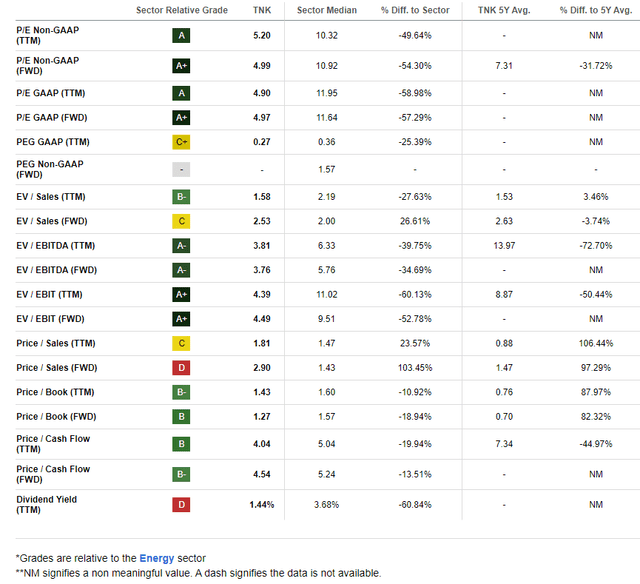

TNK: Nonetheless strong valuation ratios

Searching for Alpha

In comparison with their friendsTNK performs solidly evaluation grade whereas its development trajectory is much less spectacular and is the primary perpetrator behind the low P/E. However the sports activities firm is dependable yield tendencies and EPS over the previous 90 days have been respectable, with three income enhancements in comparison with solely a few downgrades.

lastly inventory worth momentum has been stellar over the previous few years, and I am going to spotlight key worth ranges to watch on the chart later within the article.

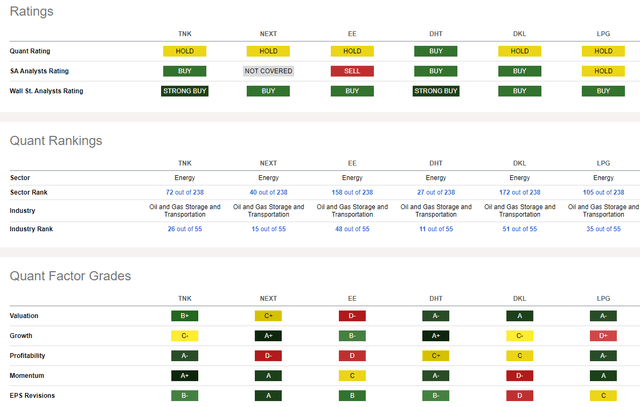

Evaluation of opponents

Searching for an alpha

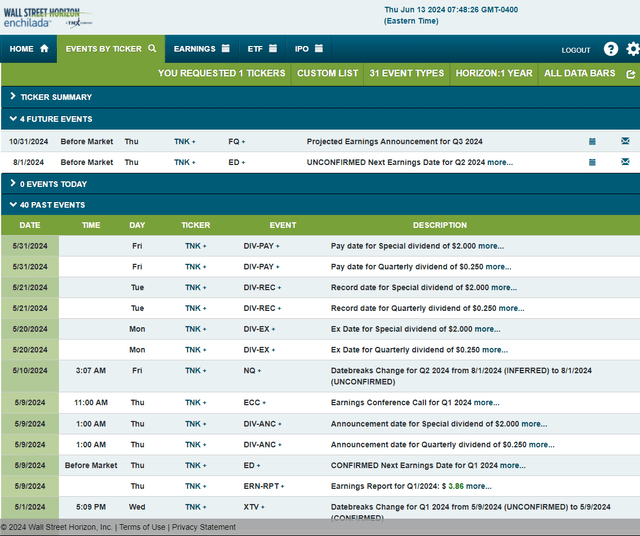

Wanting forward, company occasion information offered by Wall Road Horizon exhibits an unconfirmed earnings date for the second quarter of 2024 on Thursday, August 1st BMO. No different volatility catalysts are seen within the calendar.

Danger calendar of company occasions

Wall Road Horizon

Technical reception

TNK’s schedule could be very sturdy. Discover within the chart under that the log chart exhibits a strong uptrend beginning in 2022. The longer-term 200-day shifting common stays positively sloped and is presently close to the uptrend help line. Whereas TNC is under its 2Q peak, I see the decline as merely a play off of overbought situations. There’s a chance of additional weak spot if the worth fills the profit-related worth hole slightly below the $65 mark.

I see help on the high of the earlier symmetric triangle within the higher $50s, and this might be a good shopping for alternative from each a technical and elementary perspective. Furthermore, there’s a whole lot of quantity on the worth exhibiting within the low-to-mid $50 vary, which ought to present extra help if an extended pullback happens.

General, the TNC pattern has been sturdy, with little signal that the inventory’s rally has ended.

TNK: Bullish pattern continues, shares are engaged on overbought situations

Stockcharts.com

Backside line

I reiterate my purchase ranking on Teekay Tankers. Because of a powerful spot tanker market, the agency’s strong stability sheet and free money stream technology, in addition to strong technicals, the inventory continues to be price holding after gaining greater than 60% since This autumn final yr.