MarsBars

Written by Nick Ackerman, co-produced by Stanford Chemist.

Octagon XAI Floating Price and Various Earnings Fund (NYSE: XFLT) continues to ship excessive returns for income-oriented buyers because of robust web revenue from greater price investments atmosphere. The newest half-yearly report reaffirms that this fund’s attain stays robust. In actual fact, the most recent report means that the fund is on monitor to attain a good greater NII in comparison with final yr. As price cuts proceed to be delayed, this additionally stays excellent news for this fund as money movement ought to proceed to movement.

XFLT Fundamentals

- 1-year Z-score: -0.99

- Premium: 2.02%

- Distribution Yield: 14.31%

- Expense ratio: 3.88%

- Leverage: 38.89%

- Property beneath administration: $678.7 million

- Construction: indefinite

XFLT’s goal is to “search enticing complete returns with an emphasis on producing revenue at a number of phases of the credit score cycle.”

They may do that by way of a “dynamically managed portfolio of floating price credit score devices and different structured credit score investments within the personal markets. Below regular market circumstances, the Belief will make investments a minimum of 80% of property beneath administration in senior secured loans, CLO debt and fairness.”

The fund’s expense ratio is comparatively excessive for a closed-end fund, however as we touched on earlier, it is truly low in comparison with different CDFs out there.

That is helped by the truth that they don’t seem to be a pure play CLO fund, however it is usually price noting that they don’t have incentive charges like different pure play CLO funds. These incentive charges are sometimes earned no matter whether or not the fund earns a optimistic return or not, as they’re primarily based solely on web funding revenue.

When the fund’s leverage prices are included, the whole expense ratio is 8.64%. The fund has seen a rise in the usage of borrowings, the newest half-yearly report now stands at $169.05 million. That is greater than the $150.35 million that they had on the finish of fiscal 2023 and greater than $113.15 million borrowed on the finish of fiscal 2022. As the dimensions of the fund grew by way of market choices and fairness placements, they continued to extend the borrowings that the fund makes use of to frequently keep an efficient leverage ratio of round ~40%.

A few of its leverage comes within the type of exchange-traded most well-liked shares, XAI Octagon Floating Price Various Earnings 6.5% Most well-liked Time period (XFLT.PR.A). This comes with a present yield of 6.6%, making it a reasonably first rate selection for extra conservative buyers. I mix this with my heavier place in XFLT to assist steadiness it out. We’ve already crossed the maturity date of this preferential cost, because it occurred in March 2023. Nevertheless, the maturity date is March 31, 2026, so it won’t be legitimate perpetually.

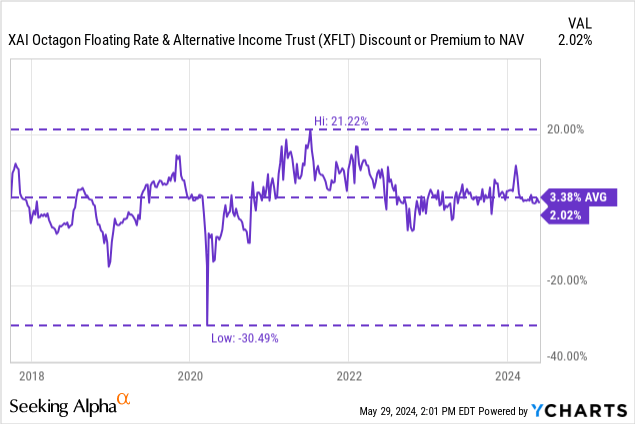

Efficiency – Premium holds up

As we famous earlier, this fund has been authorized to abolish the time period construction and change to a perpetual fund. I’ve famous a number of examples of what has occurred previously the place funds have been lowered following such adjustments. It has been a comparatively quick time frame, however that hasn’t been the case for this fund in the mean time. A minimum of nothing too main in the mean time. The fund’s premium was greater in our final replace, nevertheless it stays at premium.

The newest premium is in keeping with its long-term historic common value and has not resulted in any extraordinary low cost as we’ve got seen on a number of different events.

YCharts

It is actually nonetheless a positive atmosphere for this fund, with greater charges nonetheless in place and the truth that price minimize expectations proceed to be squeezed additional. Larger charges promise this fund. As well as, the fund will profit from an total pretty secure economic system. This fund invests closely in firms with a decrease funding grade and is leveraged.

Subsequently, any financial downturn is more likely to lead to steeper drawdowns for this fund, making it a comparatively riskier fund. Of their commentary, they really famous that the default price fell beneath the Morningstar Lending Index. That is excellent news.

However there may be additionally dangerous information. They famous that “problematic exchanges” had elevated. That is typically dangerous information, however it could be higher than the choice of complete default.

Morningstar LLI’s trailing 12-month default price decreased to 1.14% as of March 31, 2024, from 1.34% as of September 30, 2023. 3 Whereas typical defaults (akin to missed funds and chapter filings) decreased throughout the yr. Interval, the variety of downside exchanges has elevated. 3 Troubled swaps happen when a debtor swaps property which might be usually price lower than the unique mortgage to be able to restructure the debt. Distressed swaps and different legal responsibility administration transactions, or “LMTs” (during which an organization’s money owed are restructured outdoors of the traditional chapter course of), have change into extra widespread between troubled firms and their collectors as a way of lowering debt and avoiding expensive chapter proceedings. 3 We count on LMT exercise to stay excessive within the close to time period.

Normally, should you’re taking a look at a 14% yield, you recognize you are not going to get an funding in triple-A issuers. As we have seen traditionally, a very sharp drop in Covid may be fairly unstable. For my part, I consider buyers are pretty compensated when it comes to threat/reward with XFLT.

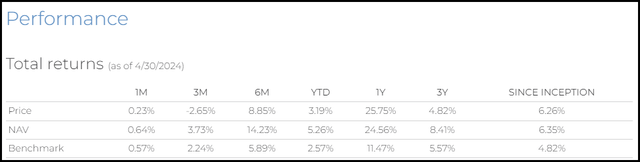

By way of fund efficiency, since its inception, the fund has crushed its benchmark. Over the previous 1 yr, the fund has greater than doubled its benchmark complete return.

XFLT annual efficiency (XA Investments)

Distribution – A strong coating stays

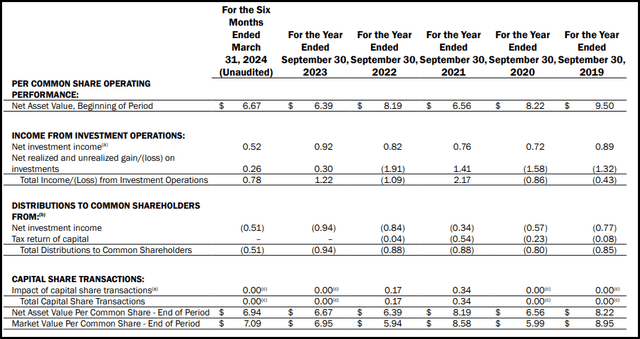

On this newest semi-annual report, we take a look at the final six months of the interval ending March 31, 2024 for this fund. The web return on funding primarily based on this final determine would carry NII protection to almost 102% for the present month-to-month distribution.

Monetary efficiency of XFLT (XA Investments)

In our earlier replace, we reviewed the three-month quarterly monetary report and famous an NII determine of $0.27 per share. This meant that we’d see a slight lower in NII in 1Q24 as it might have yielded $0.25 NII per share. Normally, that is insignificant and might simply be attributed solely to the timing of funds.

Which means the fund’s robust allocation degree of 14.31% continues to be achieved, a minimum of by way of NII. After a serious drop in 2022, the fund has additionally began to recoup a few of these losses. This has helped contribute to the robust efficiency we’ve got seen over the previous 1 yr because the fund has elevated its NAV whereas supporting such a excessive distribution.

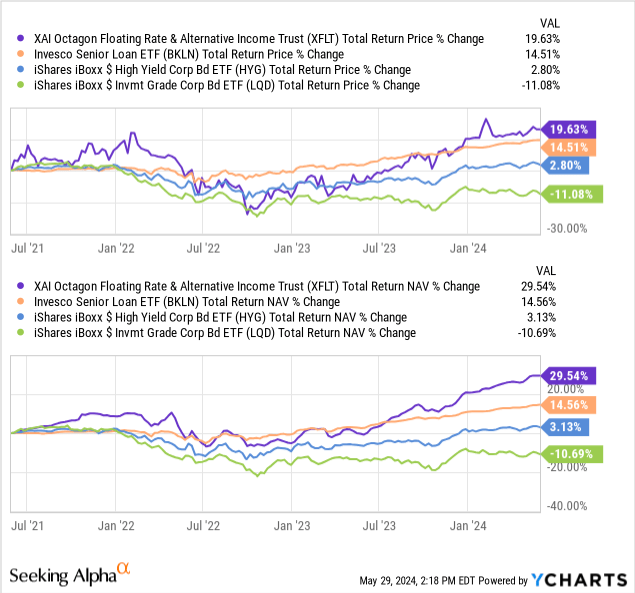

Nevertheless, it is vital to do not forget that once we look again over the previous three years, together with for the reason that Fed aggressively raised its price goal to stabilization, XFLT has carried out fairly strongly on a relative foundation. Larger rates of interest have put important stress on the mounted revenue market. This is an outline of ETFs that assist symbolize different areas of mounted revenue. The closest counterpart to XFLT is the Invesco Senior Mortgage ETF (BKLN), as BKLN additionally holds primarily floating price securities.

Then we’ve got mounted price debt ETFs representing excessive yield after which funding grade company bonds represented by the iShares iBoxx $ Excessive Yield Company Bond ETF (HYG) and the iShares iBoxx $ Funding Grade Company Bond ETF (LQD). Traders in HYG have managed to barely break even over the previous three years, whereas buyers in LQD are nonetheless taking a look at complete complete return losses over that interval.

YCharts

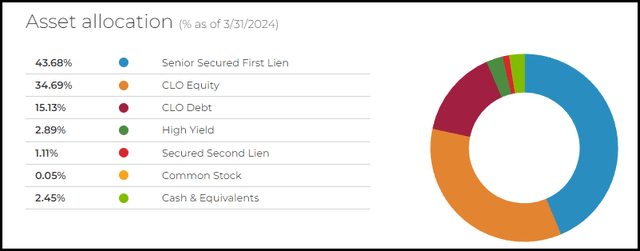

XFLT portfolio

There hasn’t been an excessive amount of to report on that entrance since our final replace. They final reported a turnover of 19%, which compares to 29% for the total 2023 fiscal yr. That might put it on tempo for the next complete turnover than reported in every of the earlier three years.

Whereas managers are actually altering positions, as mirrored in fund turnover studies, the fund’s total asset allocation has remained largely the identical as firstly of the yr. That’s, senior loans make up the biggest quantity of funds of the fund. This remained pretty much like the earlier allocation of 45.04%. This was adopted by CLO debt, which grew to become the second largest, adopted by CLO debt, every beforehand accounting for 32.09% and 16.51%, respectively.

XFLT Asset Distribution (XA Investments)

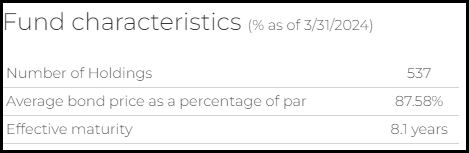

We additionally noticed the common bond value of the fund’s underlying portfolio rise barely. That is fairly attention-grabbing to notice as a result of basically because the fund’s premium has declined, it has been barely offset by a decrease common low cost in its underlying holdings.

Traits of the XFLT fund (XA Investments)

Lastly, the variety of 537 properties ought to be famous. One technique to shield funds targeted on excessive profitability is critical diversification. As a result of the dangers are unfold throughout a whole bunch of firms, this limits the fund’s publicity and that just one or two particular person failures will trigger the fund to drop considerably.

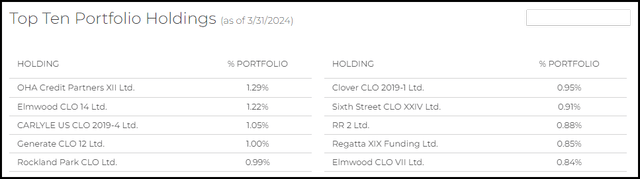

That is additionally mirrored within the fund’s ten largest holdings, none of which symbolize a very massive allocation. Additionally, CLO investments themselves include a whole bunch and even hundreds of loans bundled collectively. Of the biggest positions listed right here, most are additionally CLO positions. To remove XFLT, we have to see the economic system deteriorate throughout the board.

XFLT’s High Ten Positions (XA Investments)

Conclusion

I consider XFLT stays an attention-grabbing selection for risk-averse buyers. For my part, the fund’s threat/reward is kind of enticing. They cowl the 14.4% yield they pay buyers with the money movement generated within the underlying portfolio. So long as the charges do not come down, it ought to keep that approach too.

Nevertheless, being extremely leveraged and investing primarily in sub-investment grade securities means there may be all the time the potential for a black swan occasion to drop the fund by 50% shortly. In spite of everything, you do not get that yield since you get entry to pristine triple-A debt devices.

The premium has gone down a bit since our earlier replace. Our goal low cost/premium “Purchase” is definitely parity, or in different phrases, any low cost on this fund will likely be what we need to add to this place. Whereas the premium stays virtually on track, I am completely snug including at these ranges and would not be too choosy.