anyaivanova/iStock by way of Getty Photos

REGENXBIO Inc. (NASDAQ: RGNX) is a biotechnology firm growing AAV therapies for frequent and uncommon ailments. Its proprietary NAV platform creates single-dose AAV therapies that ship long-lasting therapeutic results concentrating on the underlying explanation for illness. AAV vectors ship gene remedy to particular cells, growing efficacy and avoiding hostile immune responses. The RGNX pipeline contains promising candidates corresponding to ABBV-RGX-314 for age-related AMD and DR, RGX-202 for DMD, and RGX-121 for Hunter syndrome. RGXN’s strategic collaboration with AbbVie (ABVV) is growing the ABBV-RGX-314. Regardless of the built-in biotech dangers, I feel RGNX’s potential in IP, TAM and promising scientific trial knowledge help a “Sturdy Purchase” score for risk-aware buyers.

Worth in Biotechnology: A Enterprise Evaluation

REGENXBIO is a clinical-stage biotechnology firm within the improvement of adeno-associated virus [AAV] gene remedy of frequent and uncommon ailments. RGNX was based in 2008 and is headquartered in Rockville, Maryland. This created a proprietary nucleic acid vector [NAV] Applied sciences Platform to create a single-dose AAV remedy that treats illness with a long-lasting healing impact. AAVs are viral vectors that ship gene remedy to focus on cells, growing efficacy and minimizing undesirable uncomfortable side effects corresponding to hostile immune responses. Curiously, AAVs can not reproduce, so they don’t trigger illness. The RGNX NAV platform generates product candidates, and chosen NAV vectors are licensed to different biotech companies.

Supply: Company presentation. April 2024

The RGNX pipeline contains packages for retina, neuromuscular and neurodegenerative ailments. Retina Analysis Has ABBV-RGX-314 for Moist Age-related Macular Degeneration [AMD] and diabetic retinopathy [DR]. It’s a single-dose therapy for moist AMD and DR utilizing the NAV AAV8 vector to ship a gene encoding monoclonal antivascular endothelial progress issue [anti-VEGF] antibody fragment to retinal cells.

VEGF is a protein that in these ailments stimulates the irregular progress of blood vessels beneath the retina, resulting in imaginative and prescient loss. Thus, ABBV-RGX-314 encodes an antibody fragment that inhibits VEGF, stopping the proliferation of those irregular vessels. This remedy is being studied in phases 2 and three for moist AMD, with regulatory filings scheduled for late 2025 and early 2026. This drug candidate is in part 2 analysis for DR.

Supply: Company presentation. April 2024

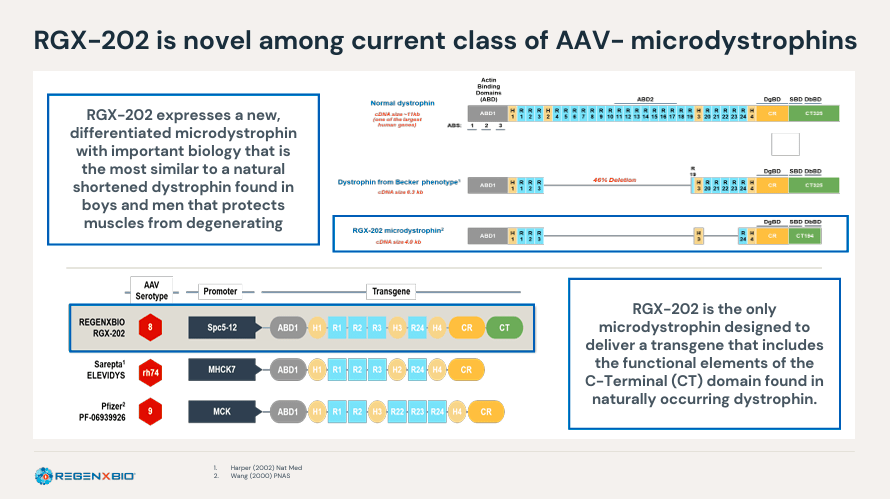

As well as, RGNX’s neuromuscular program has RGX-202, a part 2 gene remedy for Duchenne muscular dystrophy [DMD]. RGX-202 makes use of an AAV8 vector that delivers a transgene to restore the genetic modifications related to DMD. Mutations on this gene lead to incorrect coding for dystrophin, a protein required for muscle fibers. So RGX-202 is a therapeutic transgene that encodes a truncated however lively dystrophin protein known as microdystrophin that may restore muscle cell performance. The remedy offers a single-dose therapy that addresses the underlying explanation for the illness and may doubtlessly halt the development of DMD.

Supply: Company presentation. April 2024

As well as, the corporate’s neurodegenerative illness program has RGX-121, which is in a pivotal examine involving sufferers within the Part 1/2/3 CAMPSIITE trial. It makes use of an AAV9 vector to ship a practical copy of the gene chargeable for the manufacturing of the lysosomal enzyme iduronate-2-sulfatase [IDS]. Deficiency of this enzyme causes kind II mucopolysaccharidosis [MPS II], often known as Hunter syndrome. IDS is an enzyme that breaks down glycosaminoglycans (GAGs) in lysosomes. In IDS deficiency, GAGs accumulate in cells and injury the central nervous system with cognitive regression.

Thus, the IDS gene restores enzyme manufacturing and reduces GAG accumulation, stopping cognitive decline and different neurological signs of MPS II. This remedy has the next FDA designations: Orphan Drug, Uncommon Pediatric Illness, Quick Observe, and Regenerative Drugs Superior Remedy. The corporate plans to use for a biologics license [BLA] for RGX-121 in 2024.

Racing forward: market potential

In March 2024, RGNX and AbbVie revealed two-year knowledge for ABBV-RGX-314 indicated for moist AMD. The outcomes confirmed the security and efficacy of the gene remedy as a subretinal injection. Information collected from 1,200 sufferers worldwide will contribute to the event of a one-time therapy for moist AMD. If profitable, ABBV-RGX-314 might turn out to be the brand new normal of care [SoC]. It must be famous that AbbVie paid $370 million in 2021 for the rights to this drug. The settlement offers for as much as $1.38 billion in extra improvement and milestones, in addition to an equal share of U.S. distribution earnings. AbbVie will handle the commercialization outdoors the US and pays RGNX a share of the income as royalties.

As well as, RGX-202 has demonstrated efficacy in DMD in pediatric and aged sufferers with an affordable security profile. Security issues are key as a result of Pfizer not too long ago had a tragic end result for a boy who suffered cardiac arrest after a 12 months of receiving the microdystrophin gene to deal with DMD. It was additionally a scientific trial of DMD gene remedy. Nonetheless, RGNX is assured that the security profile of RGX-202 will facilitate the trial’s progress. Thus far, administration famous that RGX-202 is exhibiting optimistic security alerts with out AEs, which is vital to differentiating DMD gene remedy. Security profile testing of the RGX-202 started in early 2023 and is anticipated to be accomplished by the top of 2025.

Supply: Company presentation. April 2024

Furthermore, RGNX’s earnings report highlighted its progress towards key challenges. For instance, the worldwide market potential of ABBV-RGX-314 within the subsequent 5 years might be about $17.0 billion. The US anti-VEGF market is estimated at $4.5 billion yearly, with 800,000 moist AMD sufferers receiving therapy each 4-16 weeks. The retina illness market is projected to achieve $11.5 billion within the US, $4.5 billion within the EU, and $1 billion in Japan. Equally, 20 million sufferers within the US, EU and Japan endure from DR. Likewise, the worldwide DMD market is valued at $7.0 and MPSII at round $1.0. Subsequently, RGNX will obtain an enormous TAM if its drug candidates are efficiently developed and commercialized.

Promising and Underrated: An Analysis Evaluation

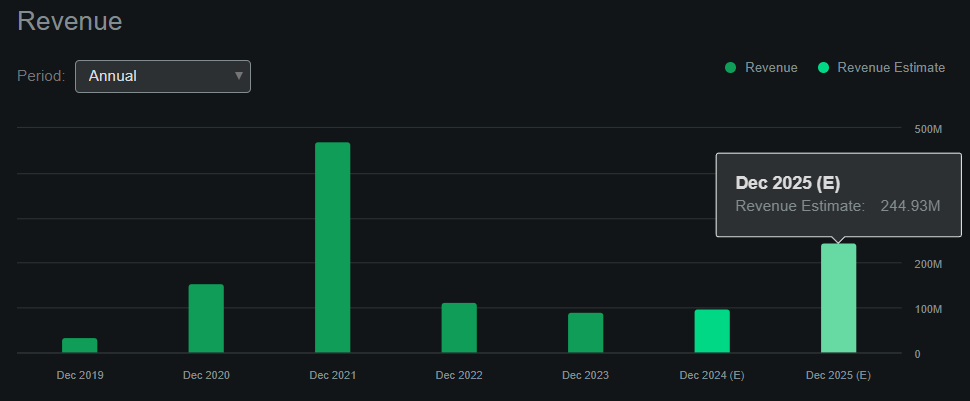

By way of valuation, RGNX has a market cap of $693.5 million, making it a mid-sized biotech product firm. Nonetheless, regardless of the shortage of product income for the foreseeable future, RGNX’s royalty income from Zolgensma ought to proceed. As well as, there’s a potential cost of $200.0 million from AbbVie upon dosing of the primary affected person in a pivotal suprachoroidal supply examine. I think the Looking for Alpha RGNX dashboard initiatives to generate round $244.9 million in income by 2025 this fashion. That may worth RGNX at a ahead P/S ratio of two.8, which is affordable in comparison with its business common ahead P/S a number of of three.7.

Supply: Looking for Alpha.

Furthermore, RGNX maintains $113.0 million in money and money equivalents plus $225.7 million in marketable securities on its steadiness sheet. This provides as much as $338.7 million in available liquidity for the corporate following a $140.0 million capital improve. Moreover, I estimate that RGNX’s most up-to-date quarterly bills have been $56.1 million when CFOs and web capital expenditures are added. This assumes an annual money burn fee of $224.4 million, suggesting a money reserve of about 1.5 years. That must be sufficient to fund operations via the top of 2025, which is consistent with the corporate’s 2026 money estimate.

A cap cost of $200.0 million is expounded to RGNX for DR. (Supply: RGNX’s newest 10-Q.)

Total, then, the corporate appears to be in stable monetary form, particularly after the latest dilutive enhance. Its analysis packages are effectively superior alongside their regulatory pathways. Certainly, ABBV-RGX-314, RGX-202, and RGX-121 are probably the most promising RGNX candidates. The previous has notable help from ABBV. This, mixed with steady royalty funds from Zolgensma and a possible future milestone of $200.0 million from ABBV, affirm the long-term viability of RGNX. Lastly, its low P/S ratio relative to friends suggests it’s undervalued, even when it has loads of catalysts in 2024 and 2025. So I feel a Sturdy Purchase score is smart for RGNX.

Funding Precautions: Threat Evaluation

Nonetheless, you will need to do not forget that a good portion of the projected income in 2025 is extremely depending on the profitable progress of RGX-314 analysis. It seems secure, however knowledge on its security stay considerably speculative till part 2 and three trials are accomplished. If there are any vital setbacks, this might push again or cancel such a $200.0 million milestone cost, which is a key assumption in my “sturdy purchase” score.

The latest pullback may very well be a compelling entry worth for brand new buyers. (Supply: TradingView.)

I additionally anticipate Zolgensma’s earnings to stay comparatively steady going ahead, supporting its present money line. Nonetheless, this isn’t assured, and if these revenues decline considerably, it might power RGNX to make one other inventory providing in 2025. In spite of everything, RGNX’s money burn of $244.9 million is critical, which implies the corporate is betting large on its analysis going with out a hitch. Nonetheless, I’m conscious of those dangers, however contemplate them acceptable in mild of RGNX’s IP potential and obvious progress alongside the regulatory path.

Sturdy Purchase: Conclusion

Total, RGNX is a wonderful biotech firm with numerous merchandise. It has a gentle stream of royalty revenue and a doubtlessly giant payout in 2025. Furthermore, after a latest capital improve, RGNX’s steadiness sheet helps excessive ranges of funding in late-stage analysis and improvement. Whereas I settle for the danger concerned within the equation, I feel RGNX’s vital potential in IP, TAM, and promising scientific trial knowledge help a “Sturdy Purchase” score for buyers conscious of the biotech’s inherent dangers.